DXY is down, down.

AUD is up, but it’s still a grind.

Lead boots to the moon!

Commods too.

Big bear intact.

EM launch!

Junk vertical!

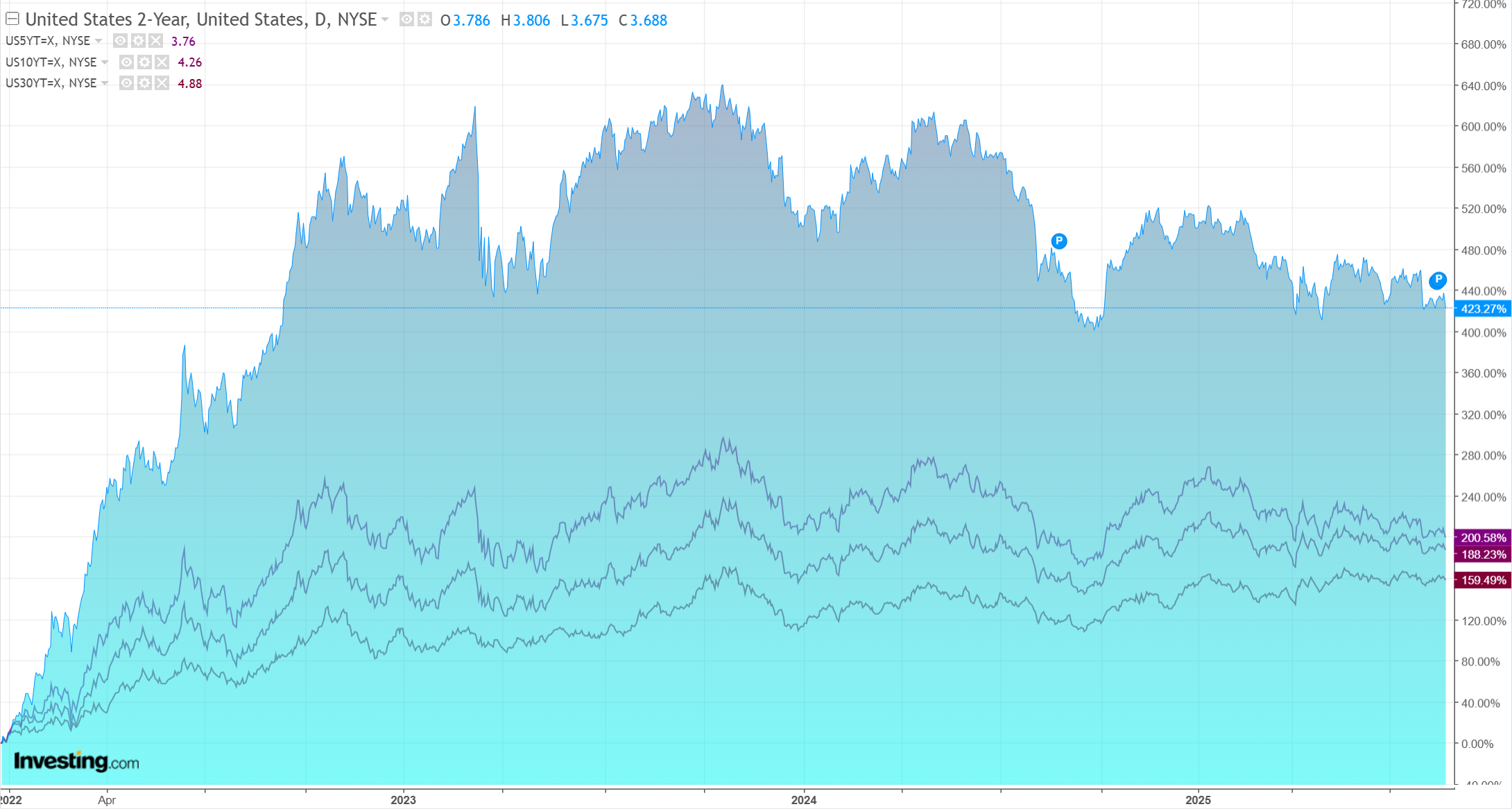

Yields pounded!

Stocks roar!

So many exclamation marks in one post means it can only be dovish Fed.

Jay Powell at the bottom of the Jackson Hole.

Putting the pieces together, what are the implications for monetary policy? In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate. Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance. Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.

How did I get this wrong?

First, the Fed should not be cutting. It has been bullied into it.

Second, don’t believe everything you read (including here). The MSM told me that the Powell speech was titled “Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy” but that was actually the session title. The speech was called “Monetary Policy and the Fed’s Framework Review,” much less benign.

So, the Fed is going to cut. I can’t see PCE or BLS stopping it, given that it should not be cutting already.

Which makes me think it is blowoff time.

AUD up but seemingly at the same plodding pace as the Chinese depression deepens.