Statistics New Zealand on Tuesday released Q2 labour force data, which reported a decline in employment and a rise in both unemployment and underemployment.

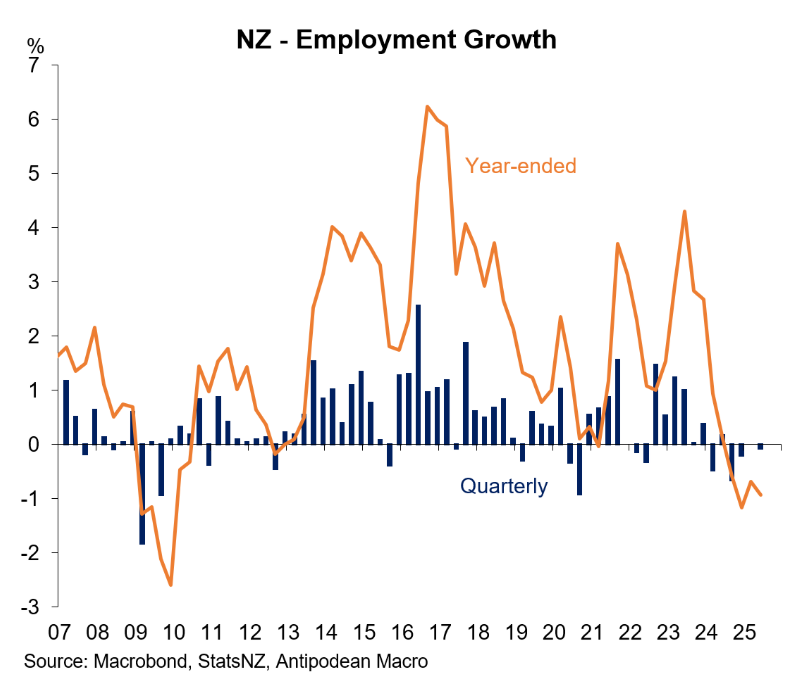

As illustrated below by Justin Fabo from Antipodean Macro, overall employment in New Zealand declined by 0.1% in Q2 and was 0.9% lower over the year.

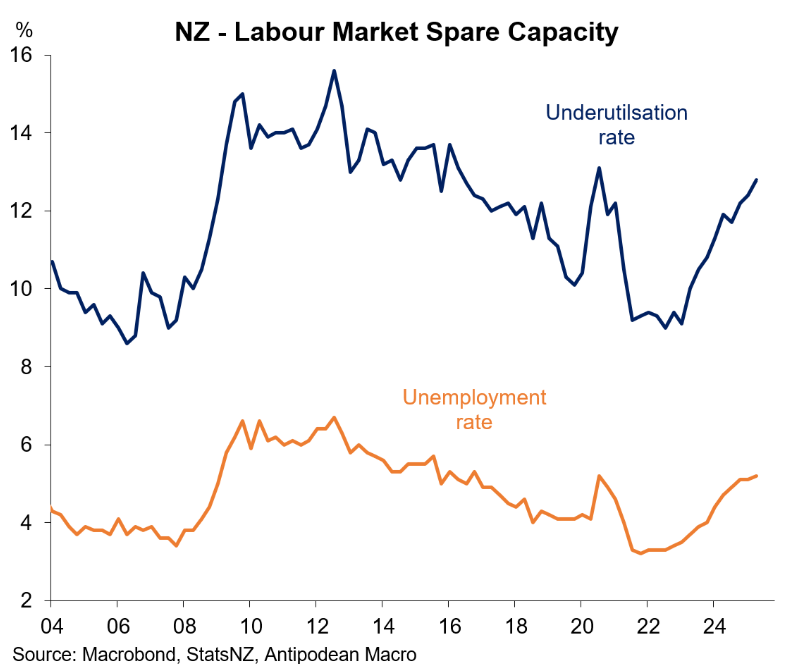

New Zealand’s unemployment rate rose 0.1% to 5.2% in Q2. This compares to 4.7% in Q2 2024. The underutilisation rate has also risen by 3.5% over the same period to 12.8%.

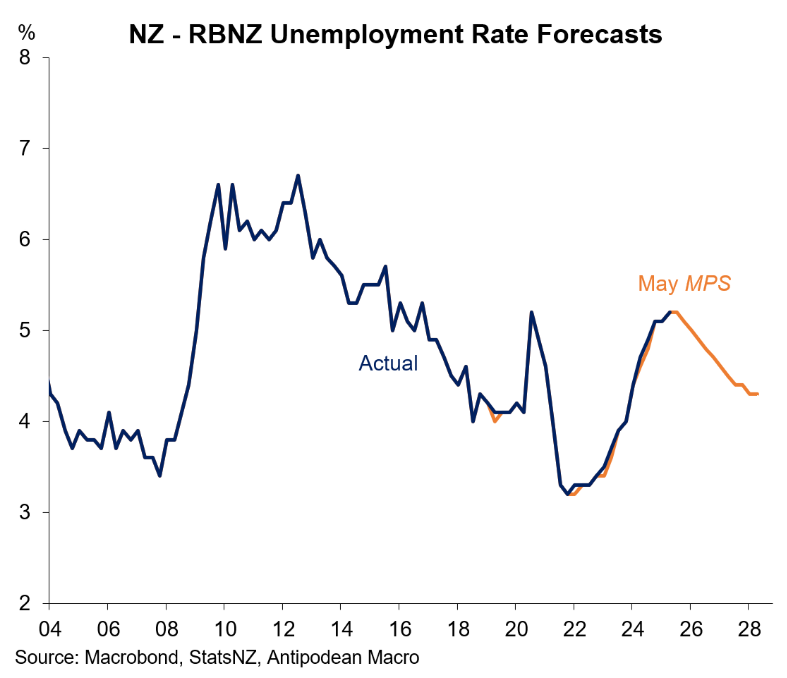

While the 5.2% unemployment print was in line with Reserve Bank forecasts, the May Statement of Monetary Policy projected a sharp fall in the unemployment rate over the next two years.

However, ANZ Senior Economist Miles Workman has warned in a research note that the unemployment rate could rise to 6% if employers stop hoarding workers in the coming months.

“Firms appear to have been hoarding labour in anticipation of an eventual economic recovery. We estimate this has kept the unemployment around 0.5% pts lower than otherwise in recent quarters”, Workman wrote.

“If the recovery doesn’t materialise with the gusto firms have been anticipating, the labour market could be hit with a double whammy: weaker-than-otherwise demand for labour and a shedding of hoarded labour”.

“The recent deterioration in the high-frequency data combined with signs that firms’ capacity to hold out for the recovery is diminishing suggests risks are skewed to weaker labour market outcomes than we or the RBNZ have been forecasting for the next year or so”.

If that happens, Workman says the Reserve Bank would have to cut the official cash rate below 2.5% to avoid inflation falling below its 1% to 3% target band.

“If firms are forced to “right-size” their labour input with layoffs instead of the economic recovery doing it for them, the OCR would likely need to be cut below the 2.5% terminal we have pencilled in in order to avoid a persistent inflation undershoot”, Workman wrote.