New Zealand’s economy continues to struggle.

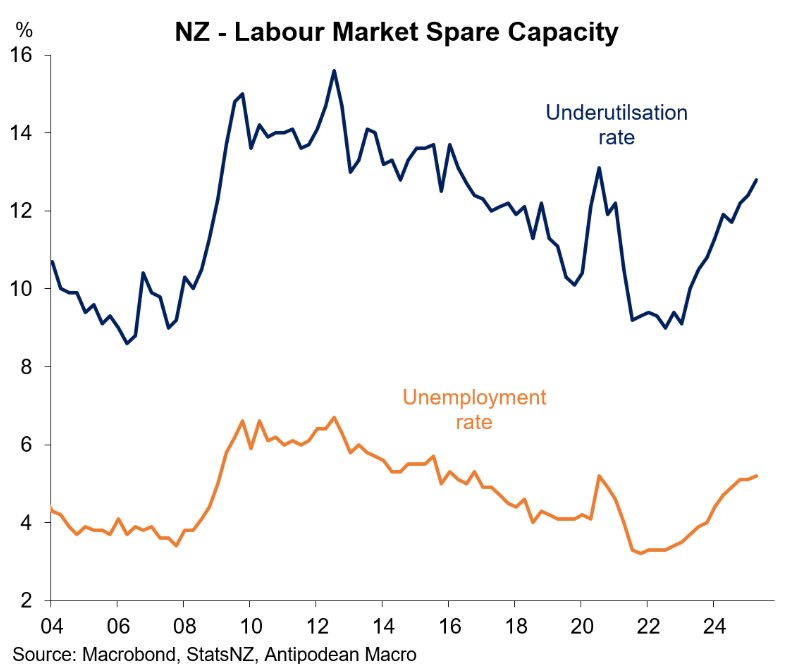

The nation’s labour market has seen unemployment and underutilisation rates soar to near-decade highs outside of the pandemic.

New

New New Zealand has lost close to 40,000 jobs since late 2023, with younger workers bearing the brunt.

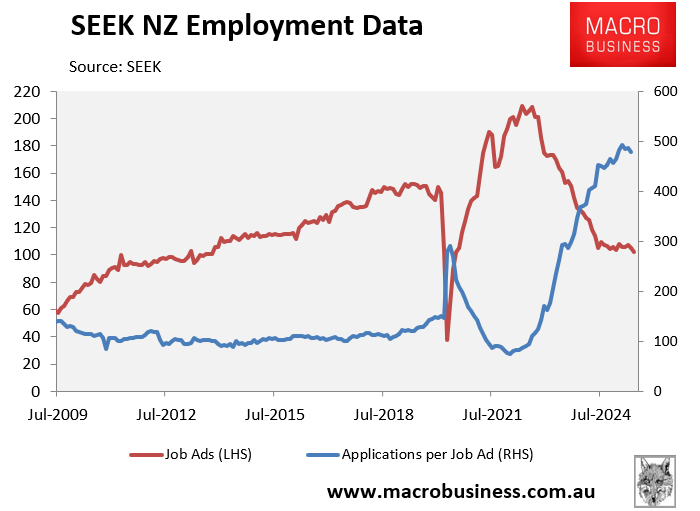

Unofficial labour market indicators, including SEEK’s job ad and applications per job ad series, also show serious weakness.

ANZ Senior Economist Miles Workman warned last week that New Zealand’s unemployment rate could soar to 6% if firms cease hoarding and “right size” their workforces.

New Zealand is also now operating with 15% US tariffs on $9 billion of its goods exported to the United States, their highest level since the 1930s.

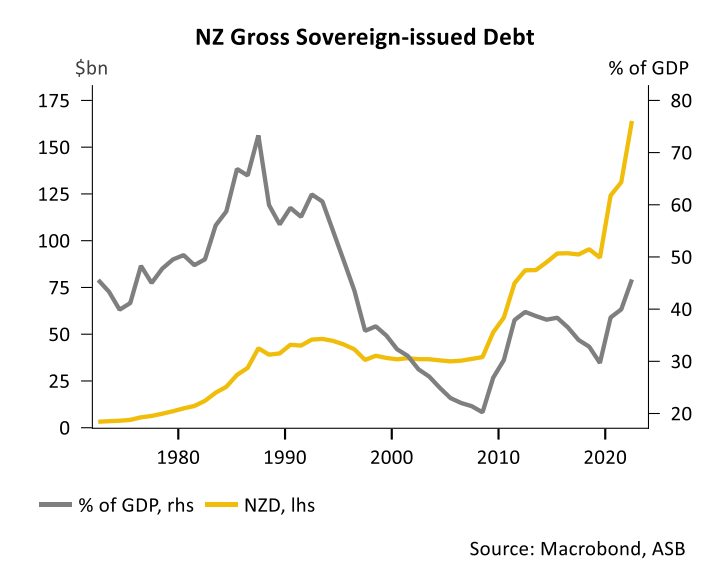

Meanwhile, the fiscal screws are tightening amid rising national debt. Austerity measures have reduced public sector administration jobs by around 15,000 from a year ago.

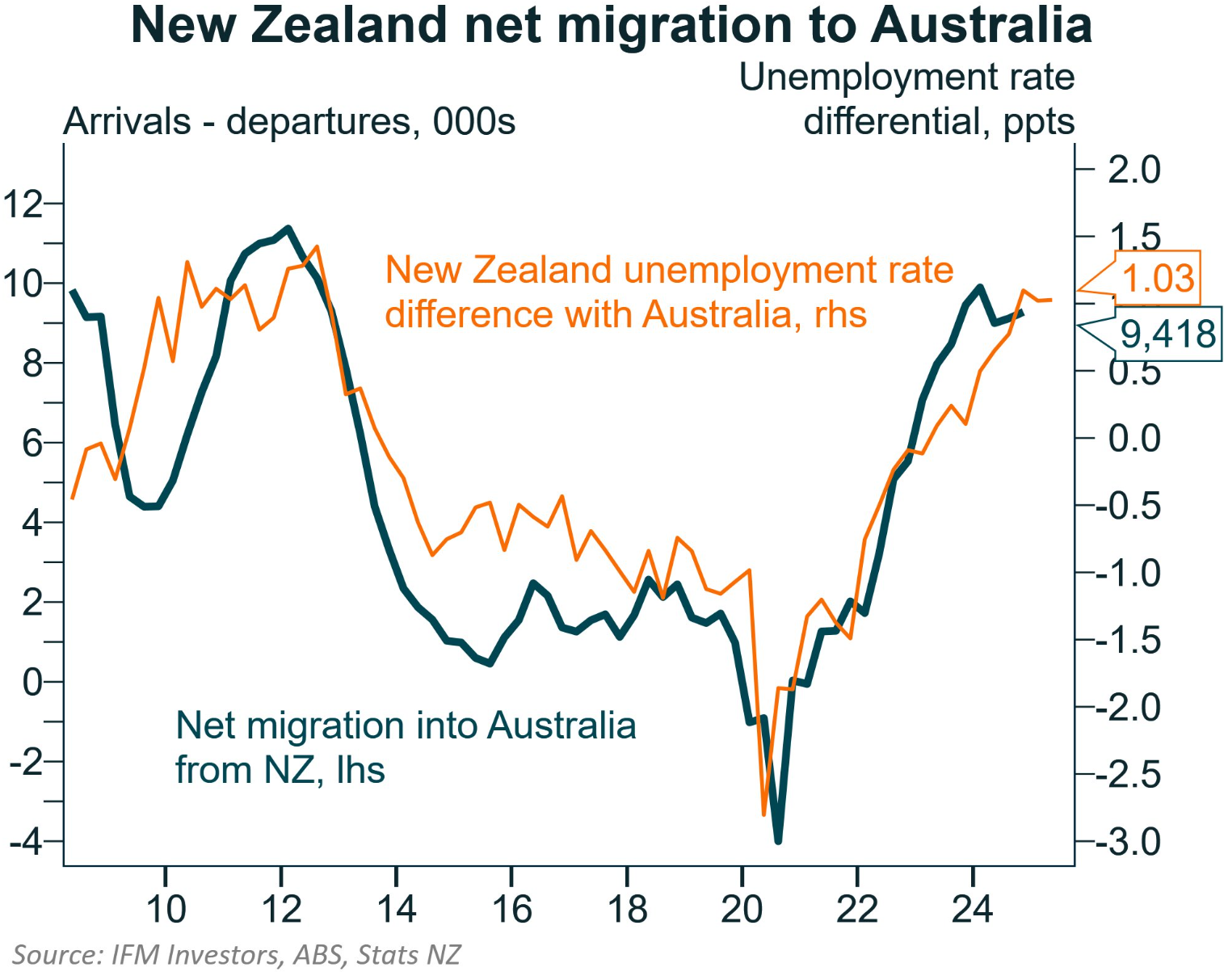

Net overseas migration into New Zealand is also at a 2.5-year low due to a surge in residents seeking better opportunities in Australia.

Given the stretched public finances, major bank ASB has called for deep interest rate cuts from the Reserve Bank to drive growth:

“Fiscal policy needs to now be focusing on rebuilding buffers rather than depleting them. Continued structural fiscal deficits will not put the government’s balance sheet in the position that it needs to be”.

“Taking the OCR back to circa 3.25% neutral levels simply won’t do it. It’s time for #2 the Terrace to assume the growth baton from #1″…

“The RBNZ need to quickly transition from tapping the monetary policy brakes to the pressing the accelerator. How much will be needed depends on the economic outlook”…

“How far and for how long the RBNZ will need to apply the monetary policy accelerator is unknown, but it looks increasingly likely that the OCR will be below 3% by the end of 2025”.

New Zealand Prime Minister Chris Luxon would certainly agree. His support is the lowest for a new prime minister since Jim Bolger in the 1990s, amid the deteriorating economy and his government’s austerity approach of restricting spending growth to reduce deficits.