New Zealand’s economy continues to face severe challenges.

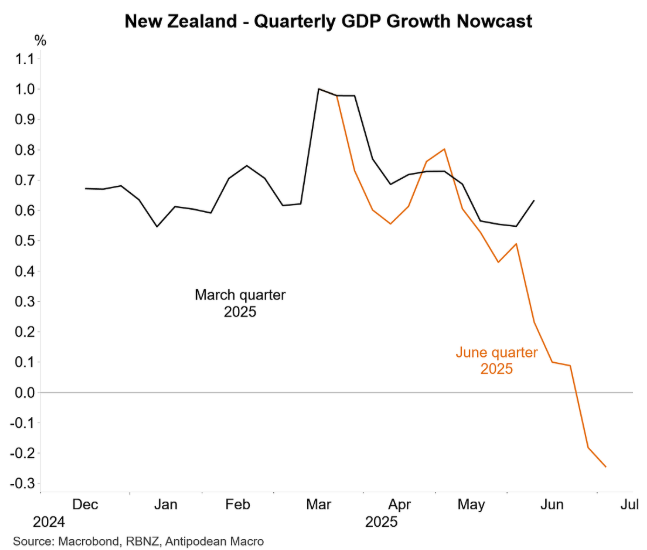

As illustrated below by Justin Fabo from Antipodean Macro, the Reserve Bank of New Zealand’s GDP growth nowcast is pointing to a 0.2% decline in real GDP in Q2 2025.

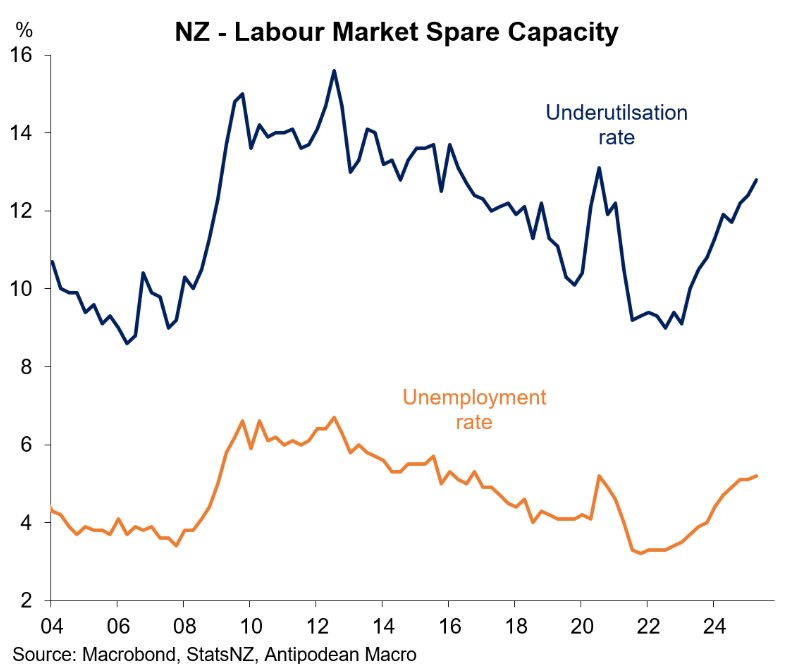

New Zealand’s labour market is also in dire straits, with unemployment and underutilisation rates soaring to near-decade highs outside of the pandemic in Q2 2025.

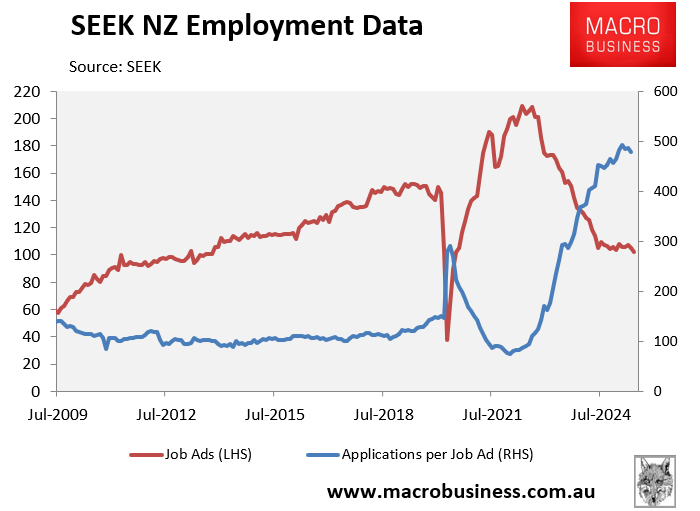

Unofficial labour market indicators point to further weakness.

SEEK shows that job ads are tracking well below pre-pandemic levels, whereas the number of applications per job ad remains near historical highs.

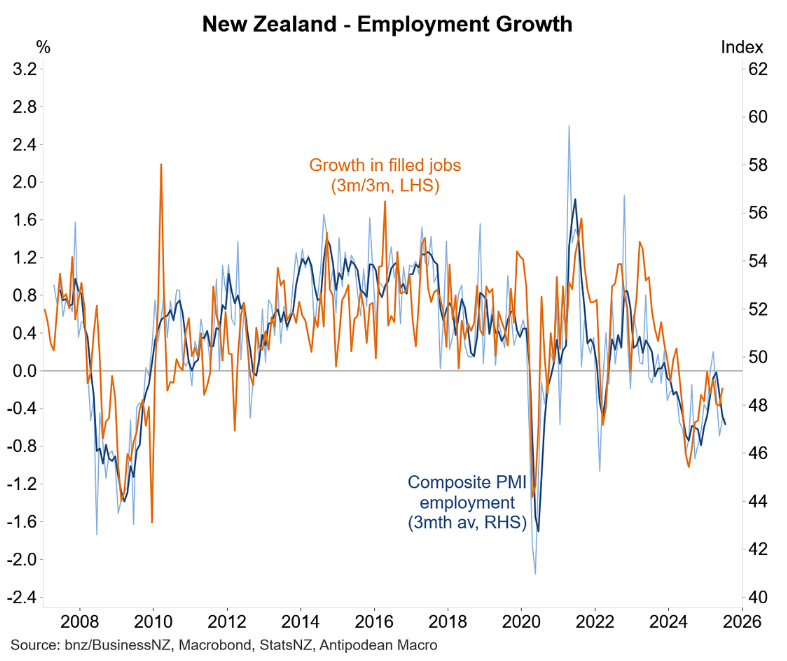

The latest composite PMI employment index remained in the doldrums in July, pointing to higher unemployment.

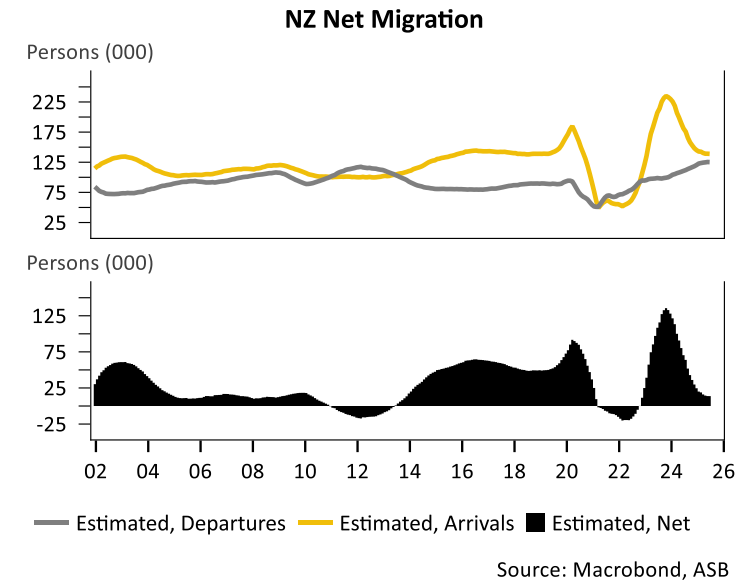

Meanwhile, net immigration inflows fell to fresh 2½-year lows in July and are one of the key factors contributing to sluggishness in consumer spending and the housing market, despite 225 bps of interest rate cuts by the Reserve Bank.

Major bank ASB expects the Reserve Bank of New Zealand to cut the official cash rate (OCR) by 25 bp at this week’s monetary policy meeting.

“With few catalysts that would kick start a domestic expansion besides monetary policy support, there is an increased likelihood that we will see a sub-3% OCR by year end”, ASB wrote in a note following the latest migration figures.

In a separate note, ASB argued that “the NZ economy needs a policy nudge to reduce excess capacity, and lowering the OCR looks to be the prudent move”.

“We expect the RBNZ to cut the OCR by 25bps as it transitions from tapping the monetary policy brakes to pressing the accelerator. How much lower than 3% the OCR will need to go will depend on the economic outlook”.

Based on the above data, it is hard to disagree. The New Zealand economy is running on empty.