No bad surprises were contained within the US CPI print released overnight although the core inflation figures continue to lift higher, it still gave most market respondents and sycophants alike the opportunity to push for a September rate cut from the US Federal Reserve which has sent Wall Street flying higher and pushed the USD lower. The “King” currency was lower against most of the majors especially Pound Sterling and Euro while the Australian dollar even advanced above the 65 cent level after yesterday’s long expected cut by the RBA. Treasury yields were mixed with the longer end steepening as the 10 year nearly pushed above the 4.3% level while the new Statistics Tzar/Bootlicker in the Trump regime indicated he wants to get rid of the monthly non-farm payroll release – see image above for reasons…

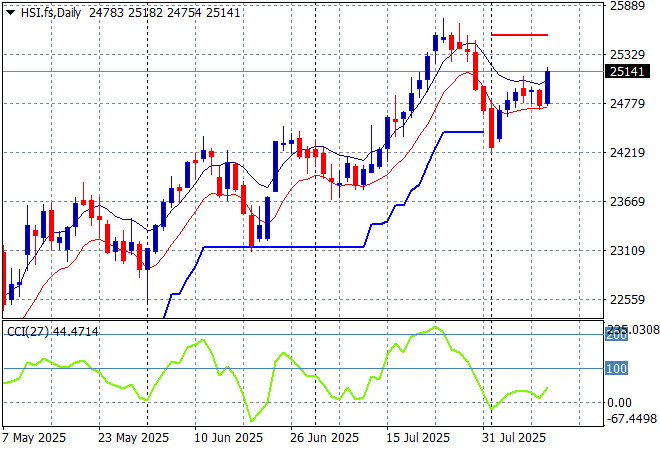

Looking at stock markets from Asia from yesterday’s session, where mainland Chinese share markets rose swiftly going into the close with the Shanghai Composite pushing well above the 3600 point level while the Hang Seng Index is still treading water as it fails to get back above 25000 points.

The daily chart shows a complete fill of the March/April selloff with momentum reversing after failing to make new highs. Resistance at the 25000 point level has turned into a stall play here with support at the 24000 point level holding:

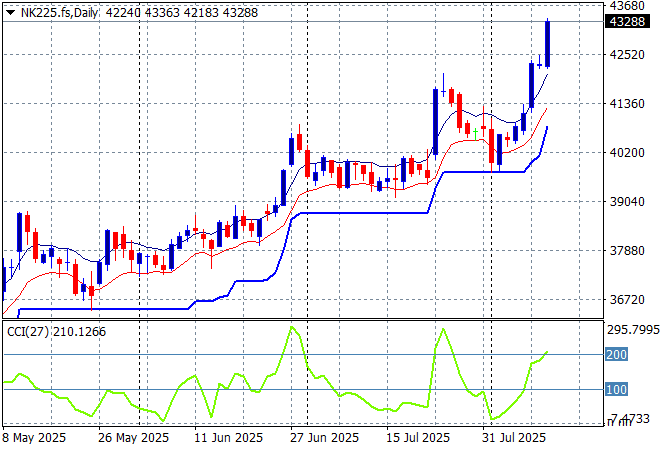

Japanese stock markets reopened from their long weekend with a strong surge with the Nikkei 225 lifting more than 2% to push above the 42000 point level, closing at 42718 points.

Daily price action was looking very keen indeed as daily momentum has accelerated after clearing resistance at the 36000 point level with another equity market that looks very stretched and breaking out a bit too strongly here. ATR support has been ratcheting up for awhile but is not stopping:

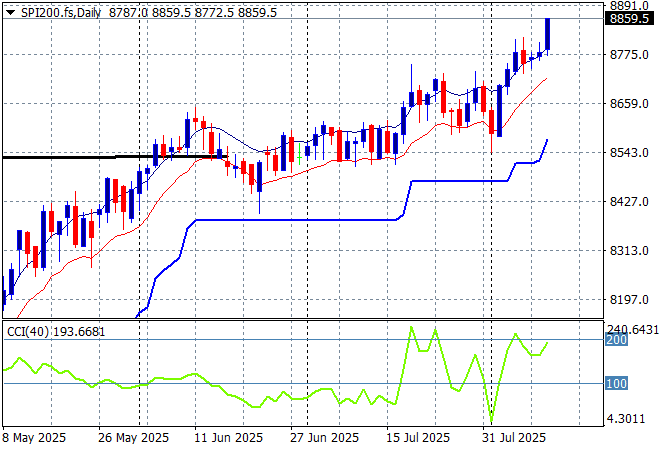

Australian stocks were the poorest performers relatively speaking, but were able to make some modest gains, with the ASX200 lifting 0.3% higher to 8872 points. SPI futures are up slightly due to the strong lead from Wall Street overnight.

The daily chart pattern is suggesting further upside still possible with a base built above the 8500 point level as daily momentum has regained its overbought status:

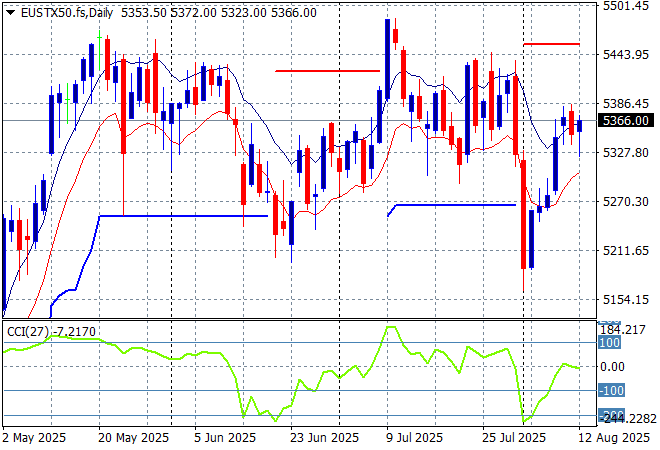

European markets are still stuck as confidence wanes across the continent with the Eurostoxx 50 Index closing just 0.1% higher overnight to finish at 5331 points.

Weekly support hadn’t moved in a few months but has now been decisively breached, with the market unable to get push any further above the pre “Liberation Day” highs. There could be daylight below but momentum was quite oversold so this might be overdone:

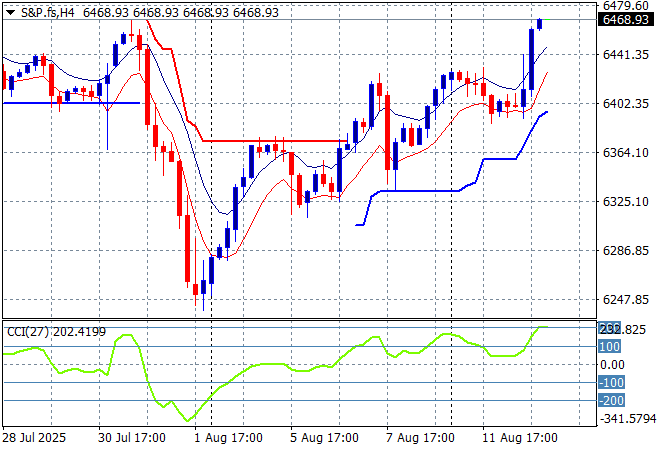

Wall Street loved the CPI print with more record highs for everyone! The NASDAQ was up 1.3% alongside the S&P500 which finished more than 1% higher at 6445 points in a similar bullish session.

The four hourly chart was looking confused with recent support at the 6200 point level coming under pressure before resistance at the 6350 point level was taken out as more record highs were made. This is looking like another attempt at getting back towards the 6500 point level as short term momentum drives back into well overbought status:

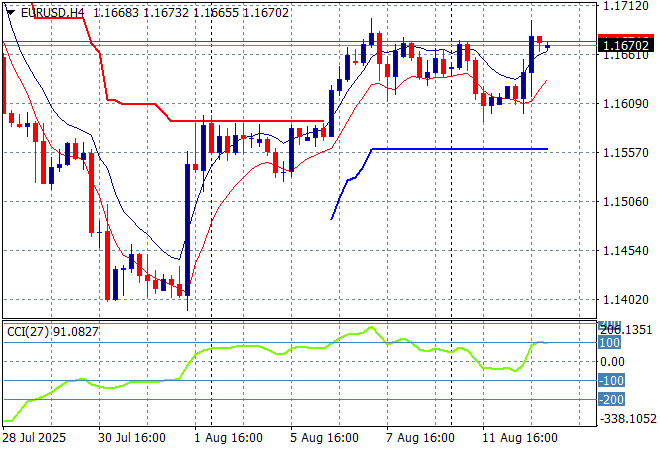

Currency markets remain against USD following a succession of poor US domestic economic prints with calls for a September cut form the Federal Reserve increasing in the wake of the consensus CPI print overnight, even though core inflation doesn’t seem contained at all! Euro and Pound Sterling among others pushed higher in the wake of the print with the former pushing well above the the 1.16 handle proper.

The union currency had been building strength continuously as bad domestic economic news from the US overshadowed any continental slowdown but had reversed that trend in recent weeks. Short term momentum was suggesting a proper rout with a new weekly low at the 1.14 handle but this is a strong reversal that may have more upside:

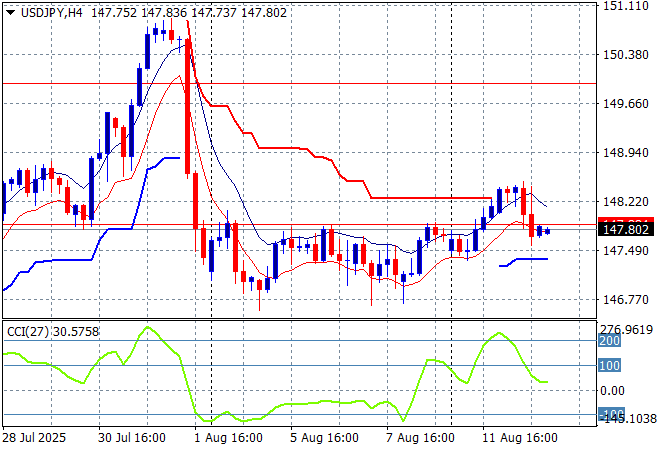

The USDJPY pair is getting pushed around its recent point of control at the 148 level on temporary Yen weakness following the Japan/US trade “deal” as it pulled back slightly overnight on USD weakness around the CPI print.

The previous price action was sending the pair beyond the March highs and had the potential to extend those gains through to start of year position at the 158 handle but the jobs surprise puts this all on the backburner. There could be another attempt here to get back to the 150 handle in the short term however:

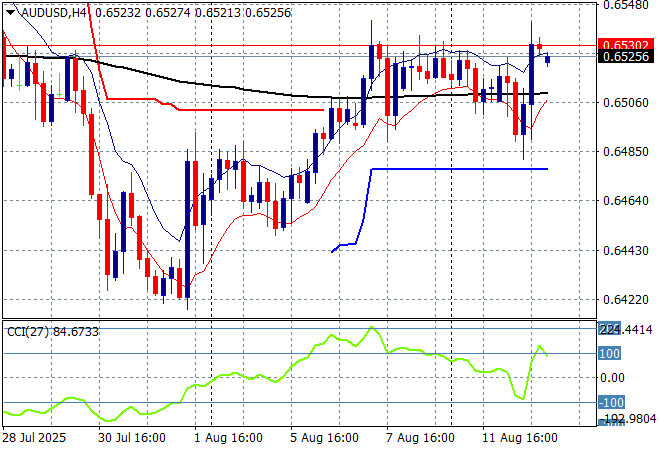

The Australian dollar was largely unchanged by yesterday’s well expected RBA cut where it held above the 65 cent level but then even pushed higher overnight on the US CPI print to match its recent weekly highs nearer the mid-65 handle.

Keep an eye on temporary support at the 63 cent level and also the series of lower highs in recent weeks of signs of less internal support, as there is potential for a rollover if Fed signalling does not become more dovish:

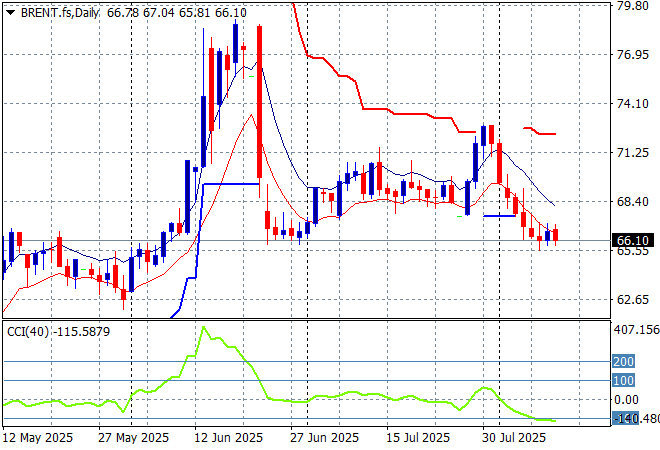

Oil markets tried to stabilise overnight with Brent crude remaining just above the $66USD per barrel level to steady at the recent weekly lows, lacking any upside momentum.

The daily chart pattern shows the post New Year rally that got a little out of hand and now reverting back to the sideways lower action for the latter half of 2024. The potential for a rally up to the $80 level after making new substantive daily highs was gaining traction but needs a lot more support in the short term:

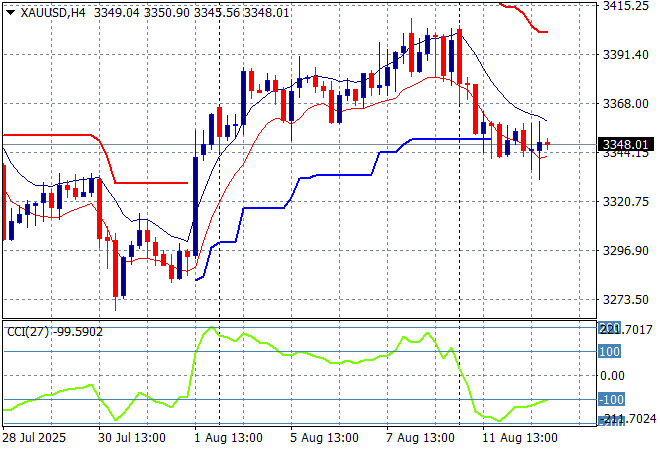

Gold is still failing to revive its recent bounceback amid concerns that the stupid Trump regime tariffs will extend to the shiny metal as it holds well below the $3400USD per ounce level, largely unchanged by the CPI print overnight to close at $3350.

Short term support had been under threat most of the last three weeks with price almost returning to the late June lows as the USD gained strength. Daily momentum was getting back into the positive zone, as support was being built but the life has gone out of this recent rally:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out/wrong on your position, so cry uncle and get out!