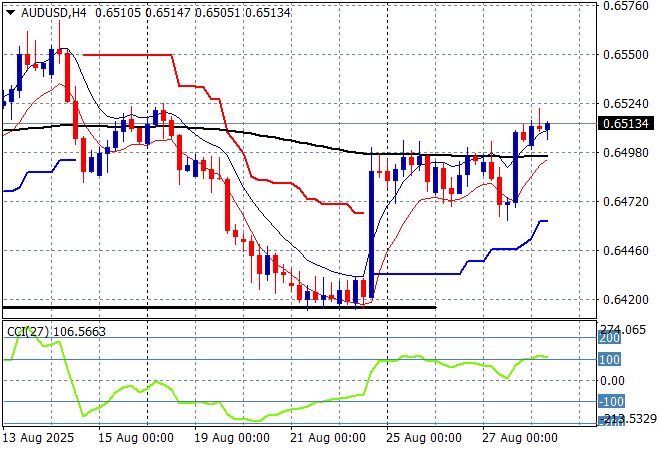

Asian share markets are in a mixed mood that is being reflected by Wall Street futures off slightly despite the better than expected NVIDIA results after the close with European shares also looking to open flat. The USD is losing ground against all the majors again as fears over the loss of independence at the US Federal Reserve as the Trump regime sacks anyone with pigment on the board. The Australian dollar absorbed the worse than expected private CAPEX print as it pushes above the 65 cent level.

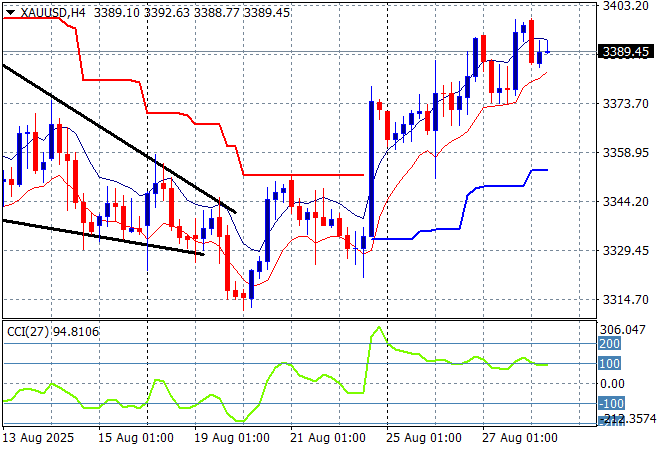

Oil markets are failing to get out of their recent depressed mood despite the successful Ukrainian strikes on Ruzzian oil lines and refineries with Brent crude back towards the $66USD per barrel level while gold is doing well but just can’t seem to breach the $3400USD per ounce level:

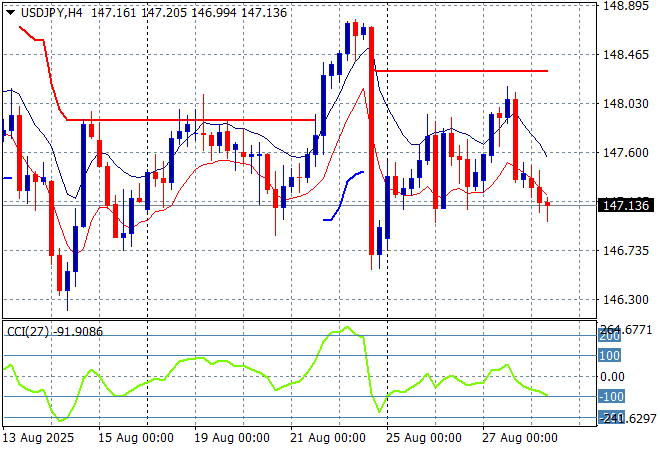

Mainland Chinese share markets are holding on to some meagre gains going into the close with the Shanghai Composite up just 0.3% to stay above the 3800 point level while the Hang Seng Index is down over 1% to 24943 points. Japanese stock markets are doing much better despite the stronger Yen with the Nikkei 225 up 0.6% at 42800 points with the USDPY pair giving up its recent new daily high to retreat down to the low 147 level:

Australian stocks were up slightly with the ASX200 closing 0.2% higher at 8980 points while the Australian dollar has pushed up through the heavy resistance at the 65 handle for a new weekly high:

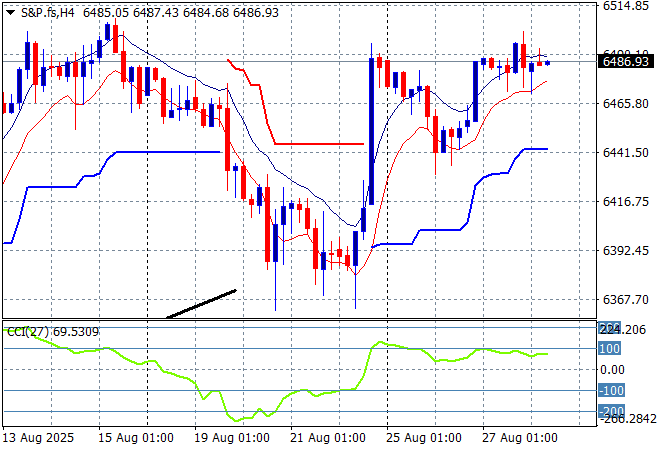

S&P futures and Eurostoxx futures are flat or slightly down going into the London session with the S&P500 four hourly chart showing the market likely to hold just below the 6500 point level with only modest upside momentum as it continues to fall just short of the early August highs:

The economic calendar will focus squarely on the latest 2Q GDP estimates from the US tonight.