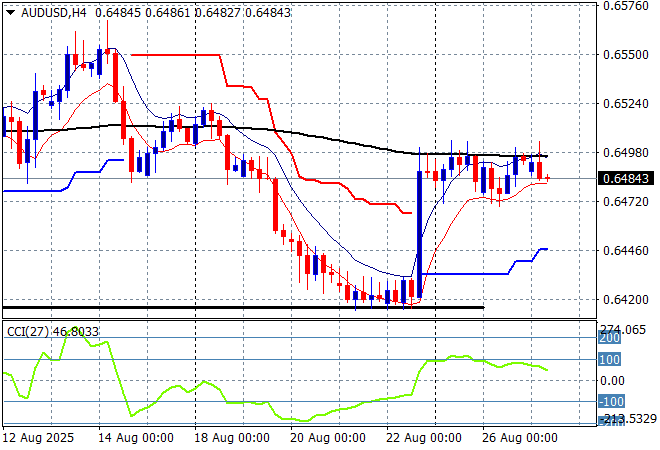

Asian share markets are still failing to translate the Friday night gains on other equity markets as the tariff threats and actual actions from the Trump regime are still being felt across the region, with India in the crosshairs today. Meanwhile the continued attack on the independence of the US Federal Reserve has seen more weakness in the USD creep in although this is early days yet with the risk of a deeper selloff in “King” Dollar not there yet. The Australian dollar absorbed a hotter than expected monthly CPI print as it remains robust just under the 65 cent level.

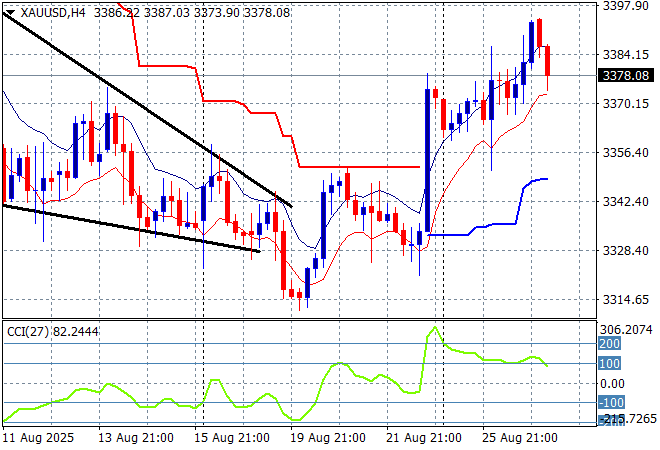

Oil markets are failing to get out of their recent depressed mood despite the successful Ukrainian strikes on Ruzzian oil refineries with Brent crude back towards the $66USD per barrel level while gold is doing well to hold on to its Friday night breakout as it steadies just below the $3380USD per ounce level:

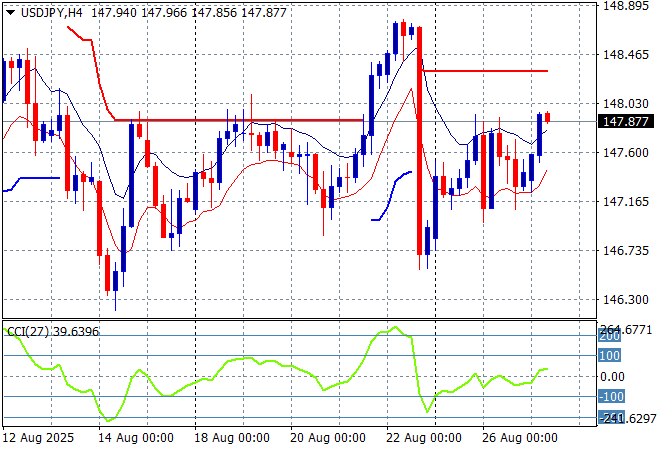

Mainland Chinese share markets are falling slightly going into the close with the Shanghai Composite losing nearly 0.2% but staying above the 3800 point level while the Hang Seng Index is down around 0.3% to 25445 points. Japanese stock markets are basically stuck as well with the Nikkei 225 up just 0.1% at 42442 points with the USDPY pair making a new daily high that is just shy of the 148 level as it begins to recover a fair amount of its Friday night losses:

Australian stocks are up slightly on the CPI print with the ASX200 closing 0.2% higher at 8952 points while the Australian dollar has pulled back slightly but is still holding on to most its gains to remain below heavy resistance at the 65 handle:

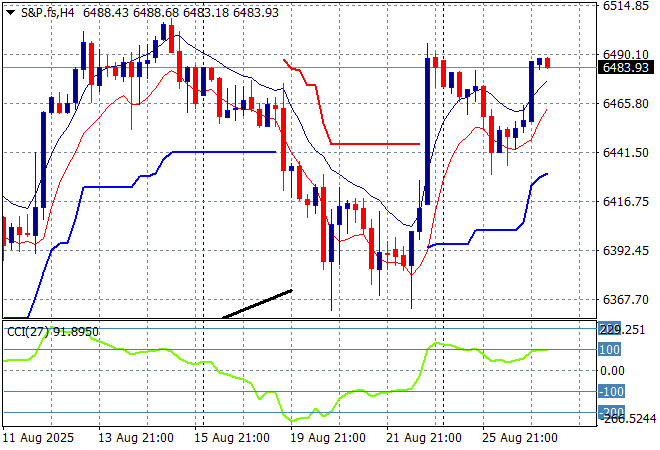

S&P futures and Eurostoxx futures are flat going into the London session with the S&P500 four hourly chart showing the market likely to hold just below the 6500 point level with only modest upside momentum as it continues to fall just short of the early August highs:

The economic calendar is relatively quiet tonight with German consumer confidence and some US oil data the only releases of note.