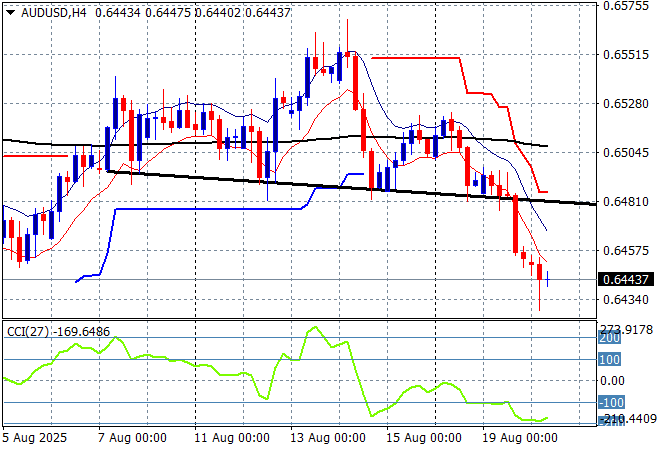

Asian share markets are mainly down across the board as risk sentiment continues to shift further into negative space as we all await the Jackson Hole conference on Friday with Fed Chair Powell expected to make some comments regarding the actual trajectory of the US economy before he likely gets fired. The RBNZ cut rates again today and have become quite dovish as the New Zealand economy continues its slowdown with the Kiwi putting in a new six month low against USD while the Australian dollar has retraced slightly in sympathy.

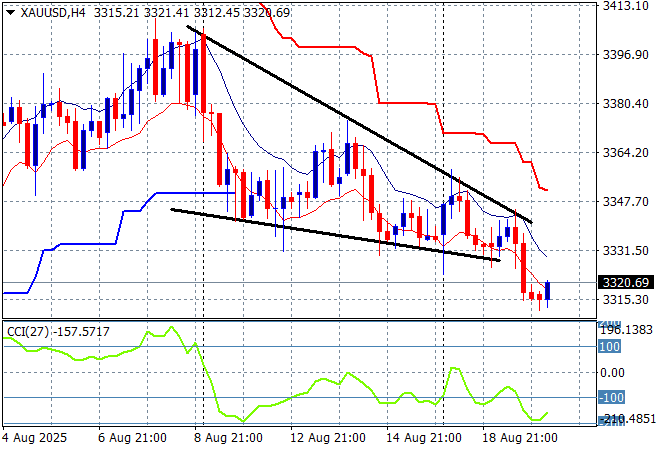

Oil markets are still depressed with Brent crude stuck at the $66USD per barrel level while gold is trying to get out of its own depression as it finds some small bids to get back above the $3320USD per ounce level:

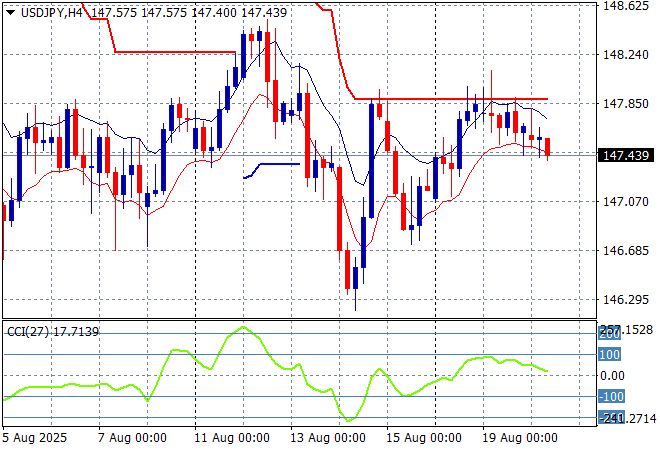

Mainland Chinese share markets are rebounding going into the close with the Shanghai Composite to stay just above the 3700 point level while the Hang Seng Index is down 0.4% as it almost crosses below the 25000 point level. Japanese stock markets are falling back further however with the Nikkei 225 off by more than 1.4% at 42859 points with the USDPY pair slowly slipping, now just below the mid 147 level this afternoon:

Australian stocks were the odd ones out in the region with the ASX200 set to close slightly higher at 8913 points while the Australian dollar has slipped further below the 65 cent level against USD in sympathy with the Kiwi, now at a two week low:

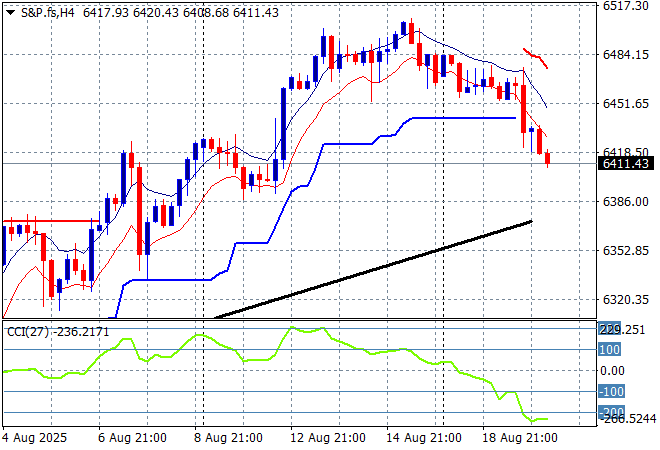

S&P futures and Eurostoxx futures are down slightly going into the London session with the S&P500 four hourly chart showing the market rolling over after failing to continue its rebound and return to the previous highs as momentum dives into negative territory:

The economic calendar continues quietly with the release of the final core CPI print for the EU, then the release of the latest FOMC minutes.