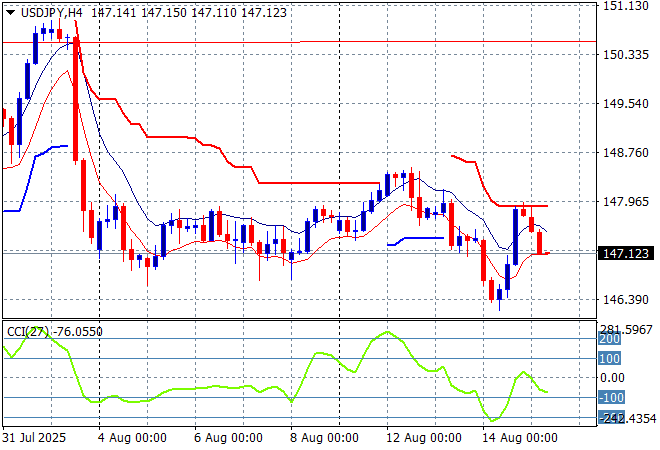

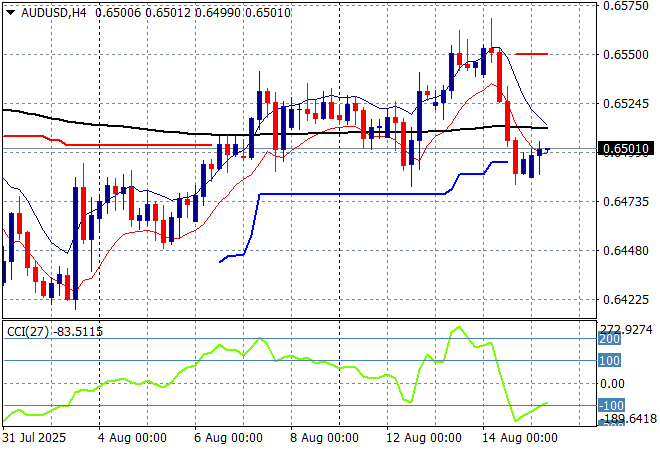

Asian share markets were dominated by Chinese data today with weakness across their domestic economy while Japanese GDP data came in slightly better than expected. Most markets are up as a result as Chinese traders expect more stimulus while the BOJ seems to be faring okay with its inflationary targets not pulling back growth. The USD is losing some ground against the majors as Euro tries to get back to the 1.17 handle while the Australian dollar has returned to the 65 cent level after falling back on last night’s hotter than expected US PPI print.

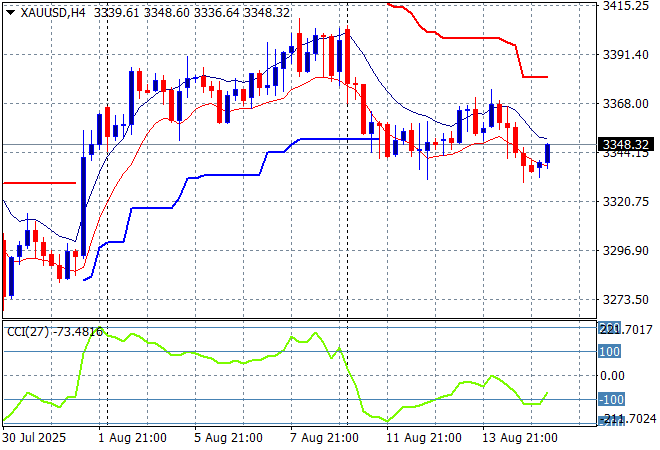

Oil markets sold off all last week and continue to struggle to make any gains with Brent crude stuck at the $66USD per barrel level while gold remains somewhat depressed but is slowly lifting after giving up its last Friday night gains, currently holding steady just below the $3350USD per ounce level:

Mainland Chinese share markets are pushing higher going into the close with the Shanghai Composite up more than 0.6% to extend well above the 3600 point level while the Hang Seng Index is not playing along, down 1.3% to almost cross below the 25000 point level. Japanese stock markets are seeing a rebound on the GDP print with the Nikkei 225 up more than 1.3% to 43242 points with the USDPY pair sinking back to the 147 level this afternoon:

Australian stocks are doing well in the final session with the ASX200 lifting more than 0.5% to 8923 points while the Australian dollar has just edged back above the 65 cent level against USD after last night’s sharp reversal:

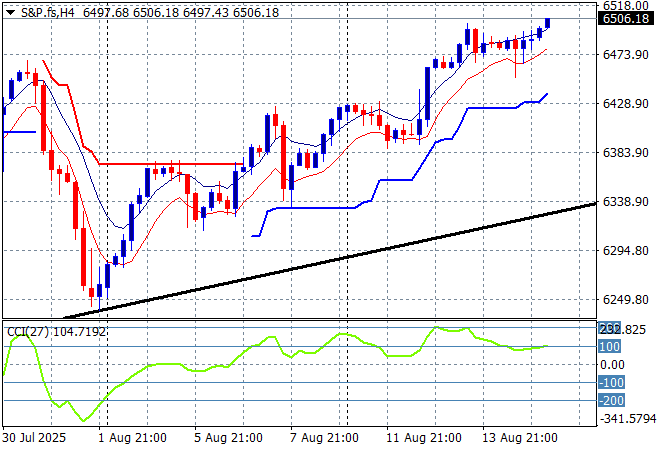

S&P and Eurostoxx futures are starting to lift going into the London session with the S&P500 four hourly chart showing the market wanting to continue its rebound and return to the previous highs as momentum goes into overdrive in the short term:

The economic calendar finishes the trading week with quite a few important US reports, namely retail sales and industrial production.