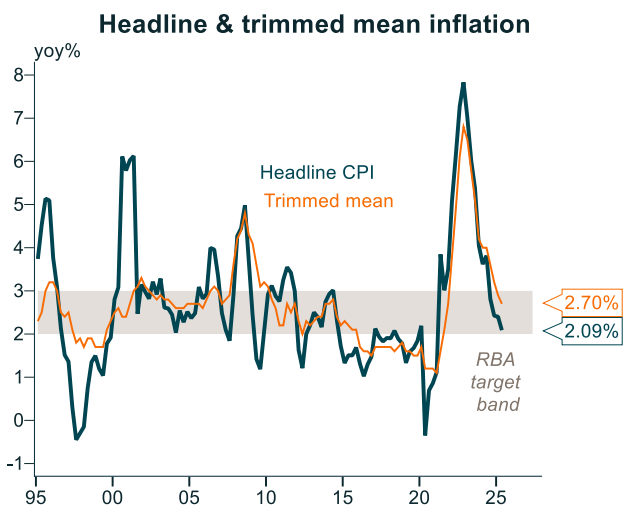

The news on inflation continues to improve, following the latest benign Q2 CPI print from the Australian Bureau of Statistics (ABS).

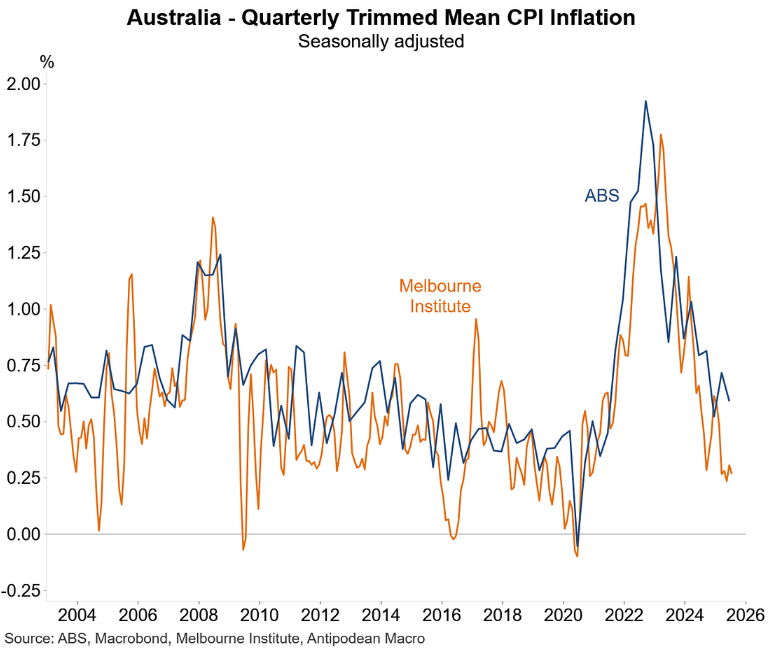

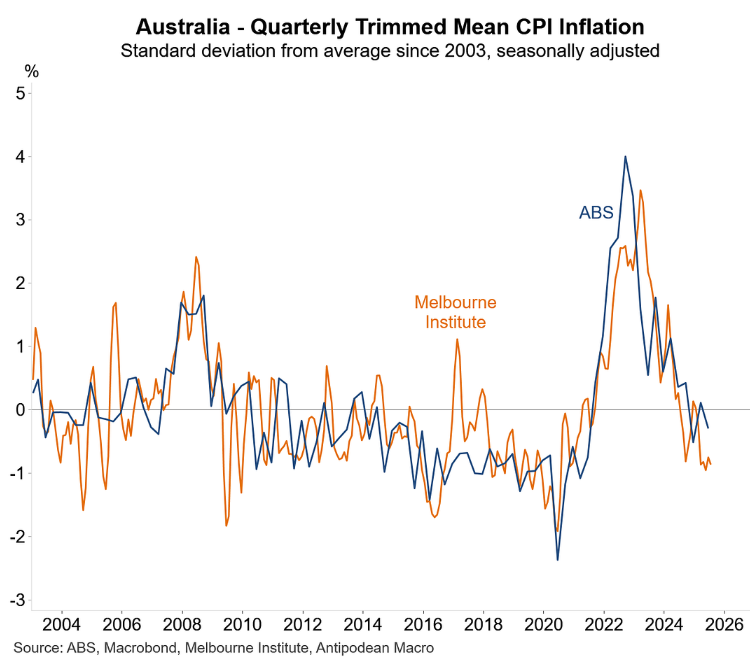

On Monday, the Westpac-Melbourne Institute (MI) monthly CPI gauge was released. As illustrated below by Justin Fabo from Antipodean Macro, quarterly trimmed mean inflation remained low in July, undershooting the ABS measure.

On Fabo’s preferred standardised basis, the MI gauge continued to be “a bit softer” than the official ABS quarterly trimmed mean inflation.

With inflation seemingly benign, the Reserve Bank of Australia (RBA) is almost certain to cut the official cash rate (OCR) by 0.25% at next week’s monetary policy meeting.

Financial markets have ascribed a 98% likelihood of a cut next week and anticipate two more reductions by early next year.

However, a growing number of economists are less optimistic and believe that the RBA is close to the end of its rate-cutting cycle.

Former RBA executive turned chief economist at Challenger, Jonathan Kearns, believes that the RBA will deliver only two more rate cuts at its August and November meetings.

“The RBA will be very cautious, and indicate that as they’re getting closer to a neutral setting, and that it’s not appropriate to be cutting at a rapid rate”, Kearns noted pointing to the resilient labour market.

“We’re much more likely to see two cuts this year than three cuts, which the market has been pricing”.

Barrenjoey chief rates strategist Andrew Lilley agrees with Kearns’ assessment that there could be fewer cuts.

“The RBA will be completely unperturbed by a slow loosening of the labour market, particularly if it’s coming with no loss of jobs, which is what we’ve had so far”, he said.

CBA economist Lucinda Jerogin argued that “it would take a considerable weakening in the economic data, particularly the labour market through a meaningful lift in the unemployment rate, to consider the meeting on September 29-30 ‘live’”.

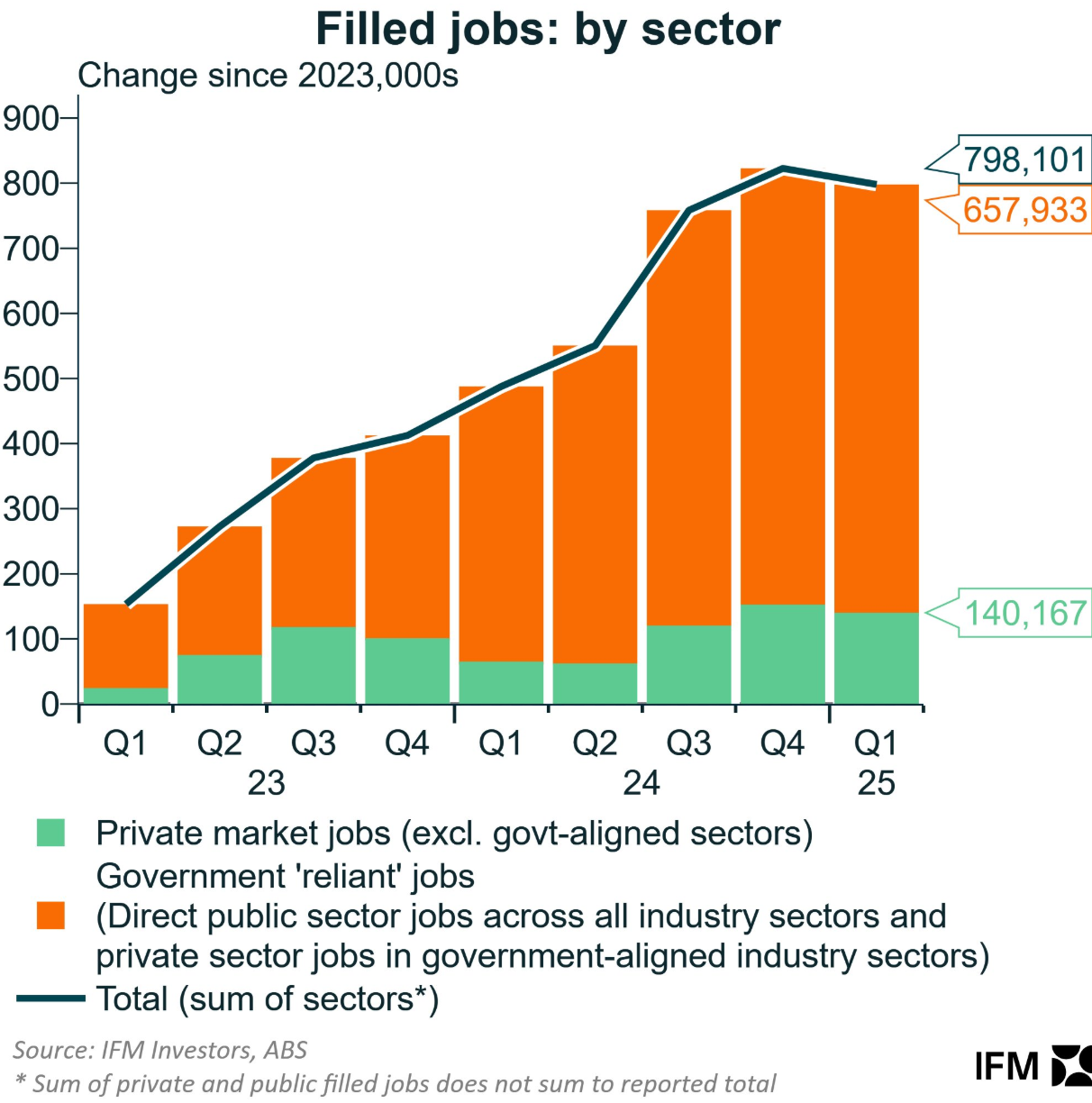

The future path of rate cuts will hinge greatly on the labour market.

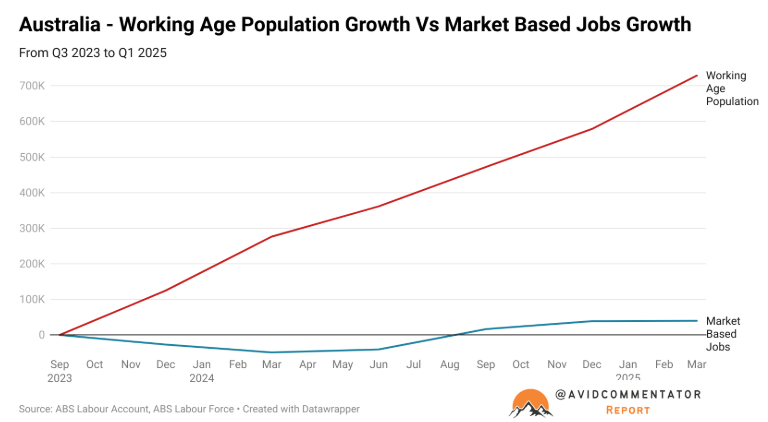

Around 80% of the nation’s job growth over the past two years has come from the non-market (government-aligned) sector, principally via the expansion of the NDIS.

The market (private) sector, meanwhile, has experienced recession-like conditions and barely any job growth.

With federal and state budgets under pressure and seeking to cut costs, the RBA is anticipating a smooth handover from government-funded job creation to private sector job creation.

There is a strong likelihood that this handover does not occur smoothly, resulting in unemployment rising far above the RBA’s expectations.

If this scenario plays out, then the RBA will cut rates harder than economists or the market are expecting.