ANZ has a funny cash rate analysis today. It has been, and remains, one of the most hawkish forecasters.

We expect a 25bp rate cut from the RBA’s 11–12 August Monetary Policy Board meeting.

The ‘no change’ decision in July showed the Board does not see itself as under pressure to cut the cash rate rapidly.

We therefore expect a variation of its ‘cautious and gradual’ approach to date to be reflected in the August post-meeting statement and the tone of Governor Bullock’s press conference.

We forecast a follow-up cut in November, with the cash rate to then stay at 3.35% for an extended period.

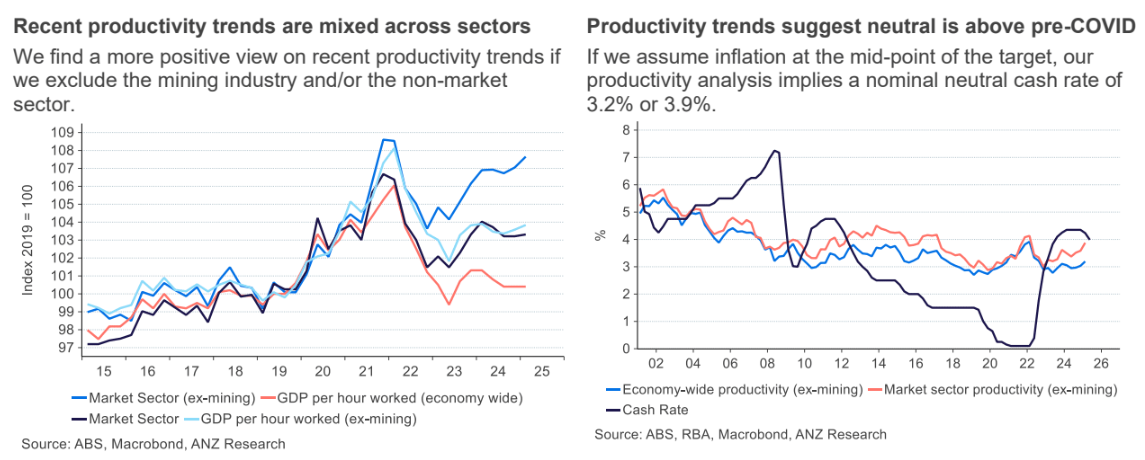

Measures of productivity that tend to be most correlated with the neutral cash rate are showing faster growth than before the pandemic, so the neutral cash rate should be higher.

Average productivity growth across those two ex-mining measures since Q1 2019 would imply a real neutral cash rate of 0.7% (economy wide ex-mining) or 1.4% (market sector ex-mining).

Assuming inflation at the mid-point of the RBA’s target band gives 3.2% or 3.9% for ‘nominal neutral’.

The former estimate is likely to be, in our assessment, similar to where the RBA sees the neutral cash rate.

Ahem…where is the stronger productivity? What is the correlation between productivity and the neutral cash rate?

In the period after 2012, when immigration shifted from a complement to growth to the driver of growth, inflation, productivity, and the cash rate all pancaked.

All that has changed since then is that we have stronger immigration and public spending, meaning even lower productivity and a developing stall in wage growth, driving down inflation.

Next year, we will embark on a repeat of the post-2012 national income smash as iron ore and coking coal tumble to boot.

The neutral cash rate is much lower than ANZ thinks.