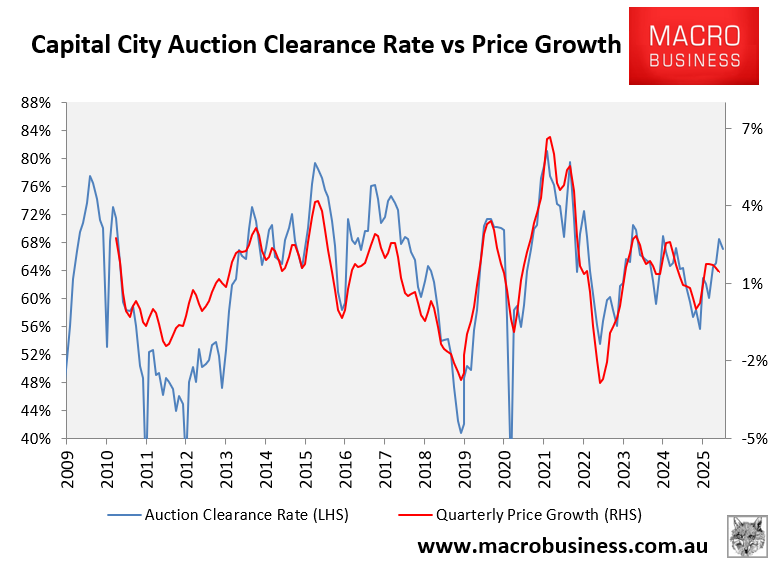

After months of strong results, Australia’s auction market has experienced a loss of momentum alongside a stalling of price growth.

Last week’s final auction clearance rate fell to 67.1%, the lowest clearance rate in six weeks. PropTrack also recorded slower price growth over the July quarter:

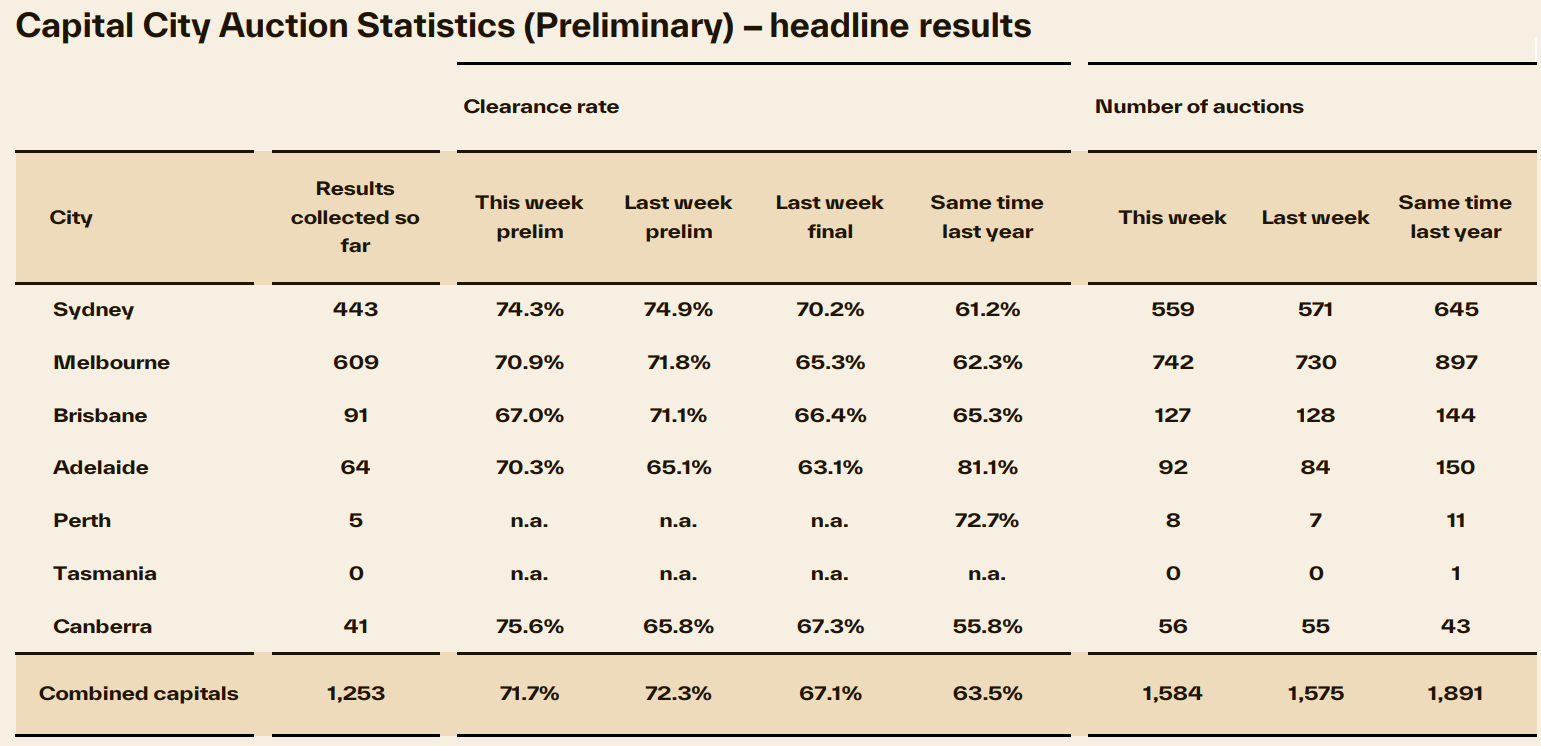

Cotality’s preliminary auction results for this weekend indicate a pause among buyers.

Across the combined capital cities, the preliminary auction clearance rate fell to 71.7%, down from 72.3% a week ago, which ended up producing the softest final result in six weeks.

Source: Cotality

While the preliminary capital city clearance rate has held above the 70% mark for nine weeks running, the loss of momentum is clear.

Melbourne’s preliminary clearance rate was 70.9% this weekend, the 15th consecutive week above 70%, but the lowest in four weeks.

Sydney’s preliminary clearance rate was stronger at 74.3%, the ninth consecutive week above 70%. However, it was lower than the 74.9% recorded a week ago.

Homebuyers might be waiting for the Reserve Bank of Australia (RBA) to cut rates before taking the plunge.

Financial markets and virtually all economists expect the RBA to cut the official cash rate by 0.25% at this week’s monetary policy meeting.

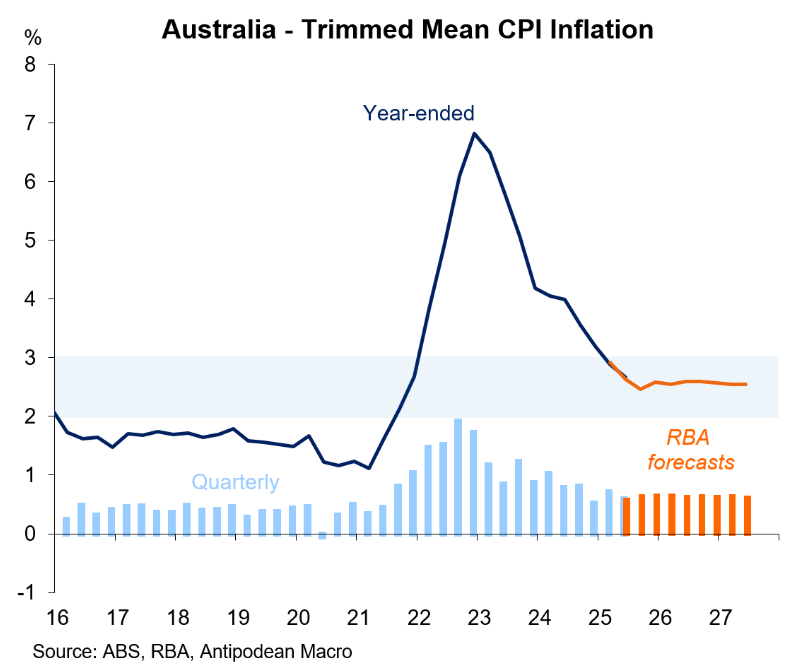

Five weeks ago, the RBA shocked the market by keeping rates on hold at its July meeting. However, the flow has since supported further monetary easing.

The all-important Q2 2025 CPI report confirmed that the disinflation impulse in the Australian economy continued in the June quarter.

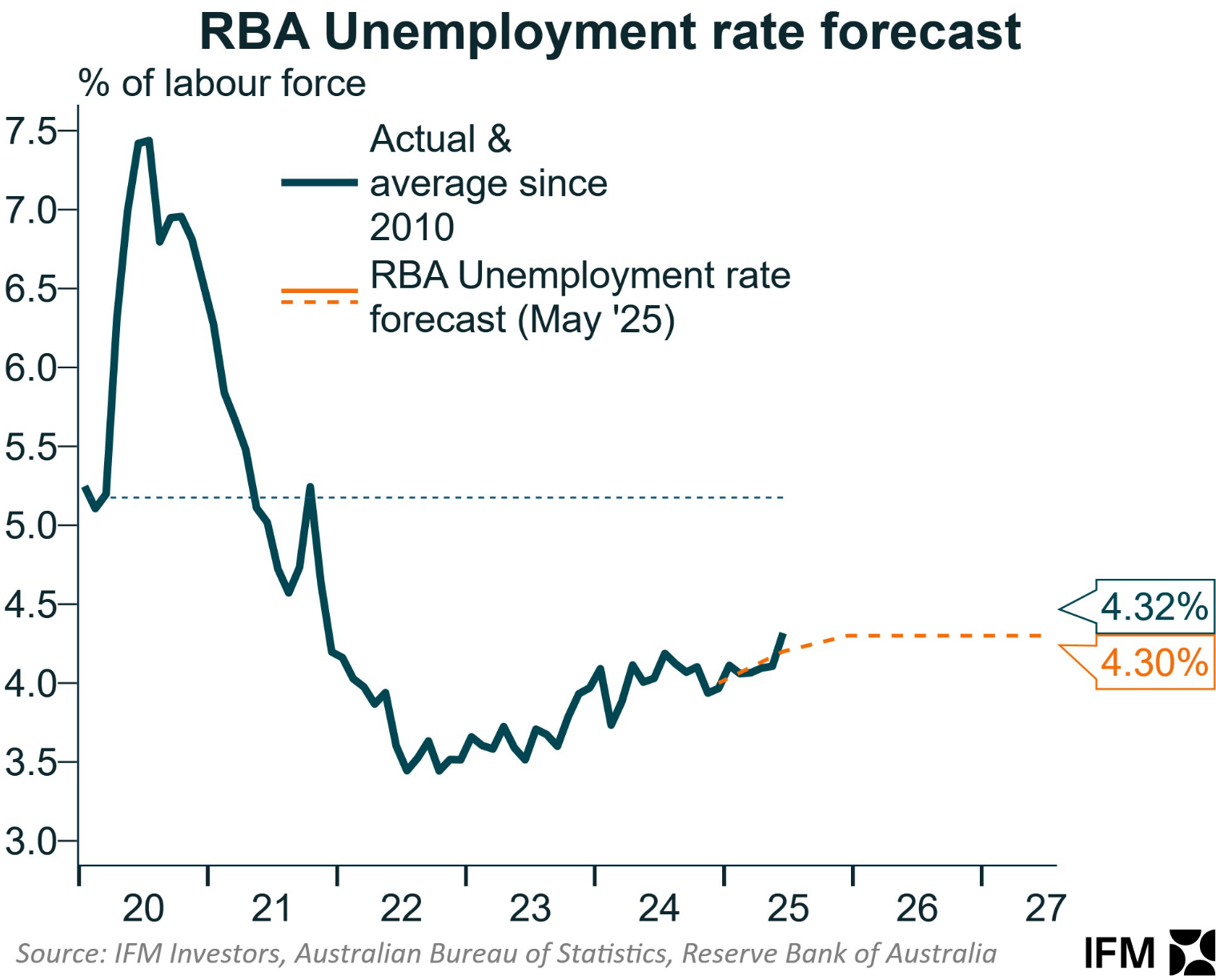

The other key piece of data was the June labour force release, which came in soft. The national unemployment rate came in above the RBA’s forecasts from May at 4.3%.

Financial markets have priced in an additional two rate cuts by mid-2026, which will stimulate buyer demand and home prices.

The federal and state governments have also launched demand-side policies aimed at increasing homebuyer demand and thus prices.

These policies include the Albanese government’s 5% deposit scheme for first-time homebuyers, the expansion of the Help-to-Buy shared equity scheme, changes to lending rules that exempt student debts from loan serviceability assessments, and state-specific policies such as the generous shared equity scheme announced in the most recent Queensland budget.

Lower borrowing rates and stimulatory policies will increase demand and prices, ultimately worsening housing affordability.