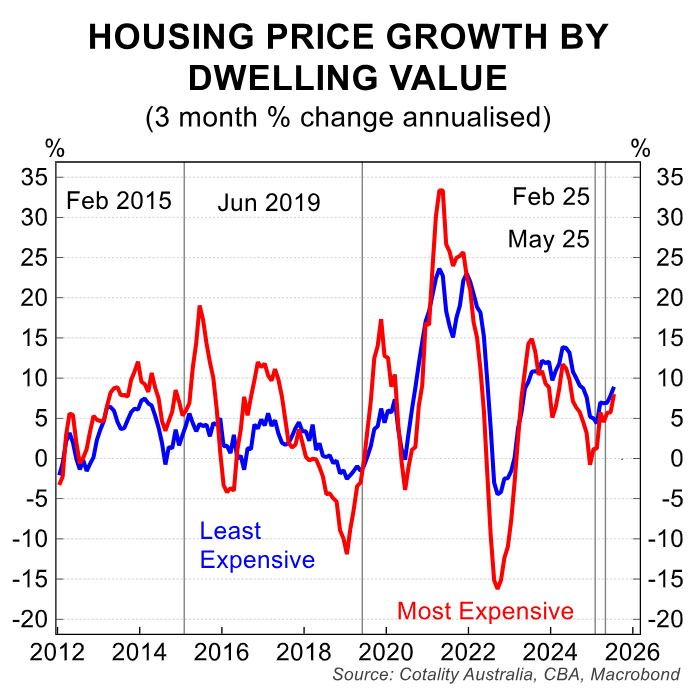

Higher-priced properties are typically the most volatile and sensitive to changes in interest rates.

This volatility is illustrated by CBA below, which plots quarterly dwelling value growth for the most expensive homes against the least expensive homes.

This greater volatility reflects the fact that the market for the most expensive homes is thinner and when mortgage rates fall, higher-income households see a bigger boost in their borrowing capacity (and vice versa).

The latest Westpac consumer sentiment survey indicated that house price expectations have risen to a cyclical high, while the “time to buy a dwelling” sub-index is also rising.

Not surprisingly, then, the two interest rate cuts delivered by the Reserve Bank of Australia (RBA) and the expectation of further easing have driven an upswing in home prices.

However, CBA Associate Economist Lucinda Jerogin noted that “since the RBA started cutting rates in February, price growth for the least expensive homes has outpaced that for the most expensive, rising by 4% and 3% respectively”.

“The driver of this trend reversal is likely linked to ongoing affordability challenges”.

“Constrained housing affordability may have lowered buyer’s purchase ability and pushed more buyers to bid on cheaper homes”, Jerogin explained.

“Greater demand for less expensive dwellings coupled with limited supply have driven up prices for this market segment”.

Demand for these entry-level homes will increase next year following the introduction of the Albanese government’s 5% deposit scheme for first home buyers.

This scheme, which comes into effect on 1 January 2026, will see the government (read taxpayers) guarantee 15% of a first home buyer’ mortgage.

As a result, first home buyers will be able to purchase a home with only a 5% deposit without requiring lenders’ mortgage insurance.

More first home buyers will be pulled into the market and will compete for the same number of mostly entry-level homes, driving up their price.

Like all demand-side measures, Labor’s 5% deposit scheme will be self-defeating from an affordability perspective.

Future cohorts of first home buyers will simply be required to take out larger mortgages to purchase what will become more expensive homes.