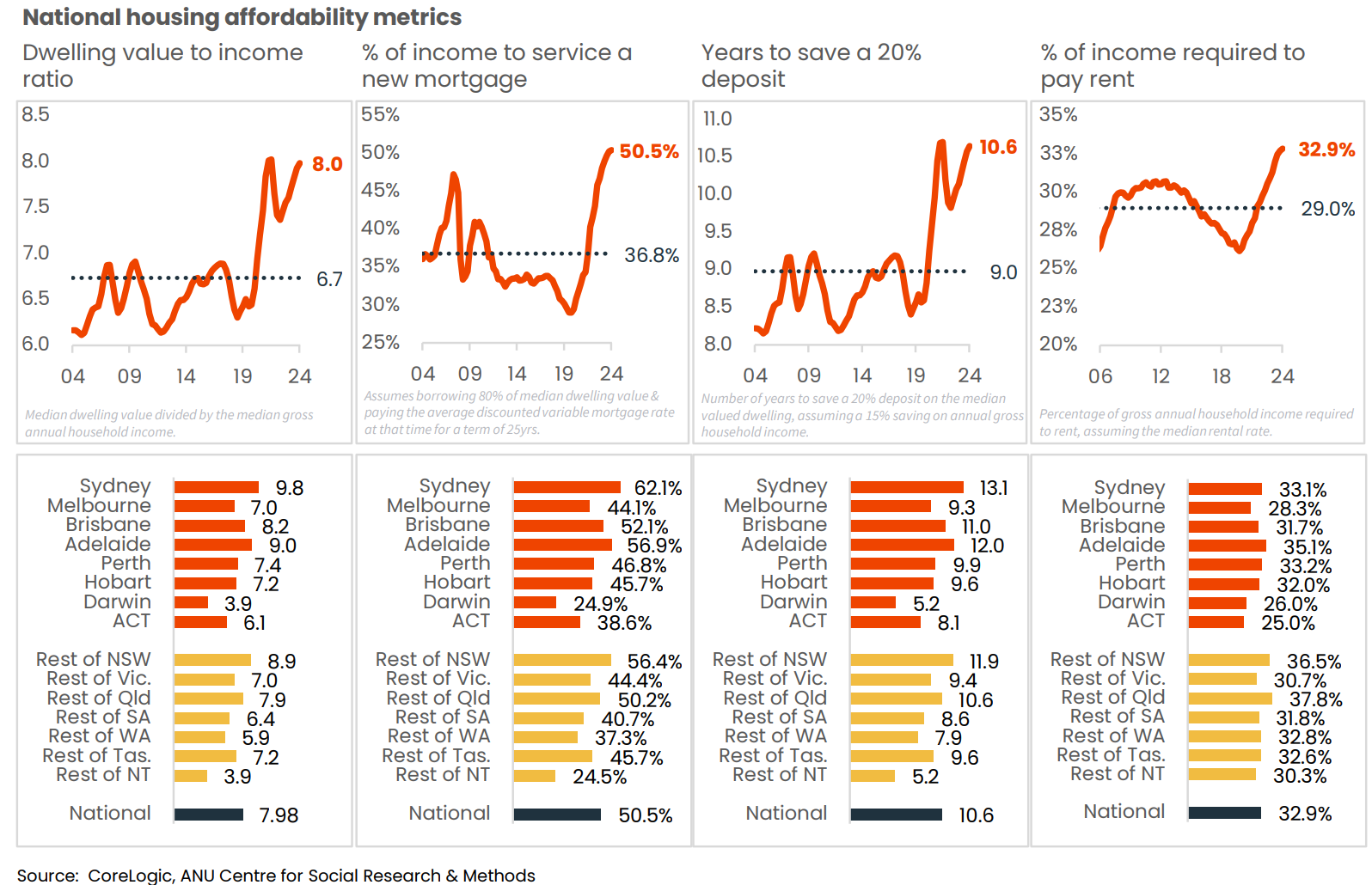

At the end of 2024, CoreLogic (now Cotality) reported that Australia’s housing affordability—both to purchase and rent—was the worst on record, as illustrated by the graphic below.

Home prices relative to incomes, the percentage of income required to service a mortgage, the number of years taken to save a deposit, and the percentage of income required to pay rent were each tracking at historical highs nationally.

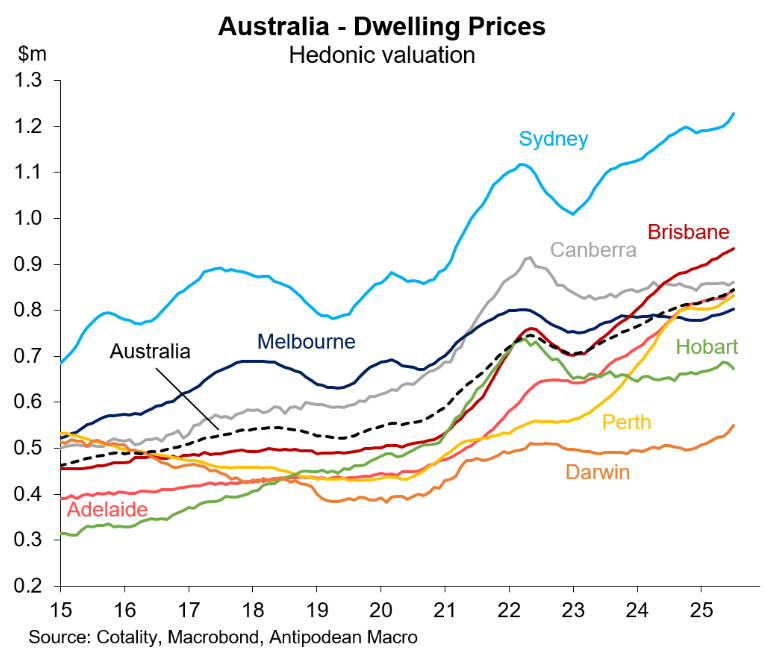

As illustrated below by Justin Fabo from Antipodean Macro, home values have continued to march higher, registering solid growth over the first seven months of 2025.

Cotality reported that the median dwelling value across Australia’s capital cities was $926,854 at the end of July.

Sydney ($1,228,435) and Brisbane ($934,623) had the nation’s two most expensive housing markets at the end of July, following growth of 35.5% (Sydney) and 76.3% (Brisbane) over the past five years.

A few weeks back, Cotality warned that home values could increase by as much as 13% by the end of 2026, lifted higher by falling interest rates and stimulatory government policies.

Cotality head of research Tim Lawless warned that home values will continue rising faster than household incomes, which will increase the price of housing relative to incomes.

The median value of Australian housing relative to incomes is expected to rise from around 8.0 times at the end of 2024 to 8.4 times the median household income.

Sydney’s home price-to-income ratio is forecast by Cotality to rise from 9.8 at the end of 2024 to 10.3 by the end of 2026.

Brisbane’s home-price-to-income ratio is projected to rise from 8.2 at the end of 2024 to 8.7 at the end of 2026.

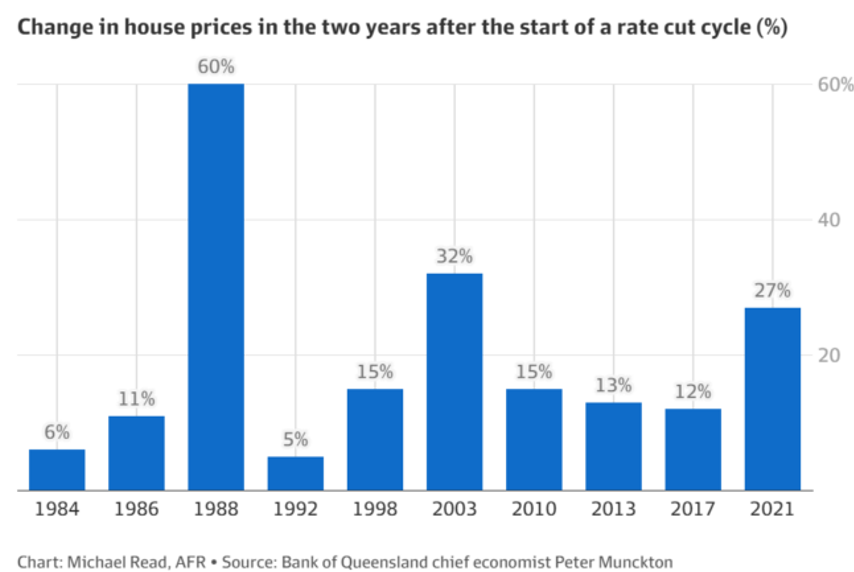

Financial markets project that the Reserve Bank of Australia (RBA) will deliver three 25 bp official cash rate cuts over the next 12 months, to 3.10%.

Cotality’s research shows that if the cash rate is cut to 3.10% within the next 12 months, then a typical Australian mortgage holder would save around $165 on their monthly loan repayments.

Recent research from the Australian Financial Review comparing home price growth against previous rate-cutting cycles showed that home values typically rise by double-digit rates two years after the commencement of a rate-cutting cycle.

Our governments have also announced a bunch of demand-side policies to boost homebuyer demand and prices.

These policies include the Albanese government’s 5% deposit scheme for first-time home buyers, the expansion of the Help-to-Buy shared equity scheme, changes to lending rules that exclude student debts from loan serviceability assessments, and state-specific policies, including the generous shared equity scheme announced in the most recent Queensland state budget.

The combination of lower borrowing rates and government stimulus will inevitably lift home values, making affordability structurally worse.

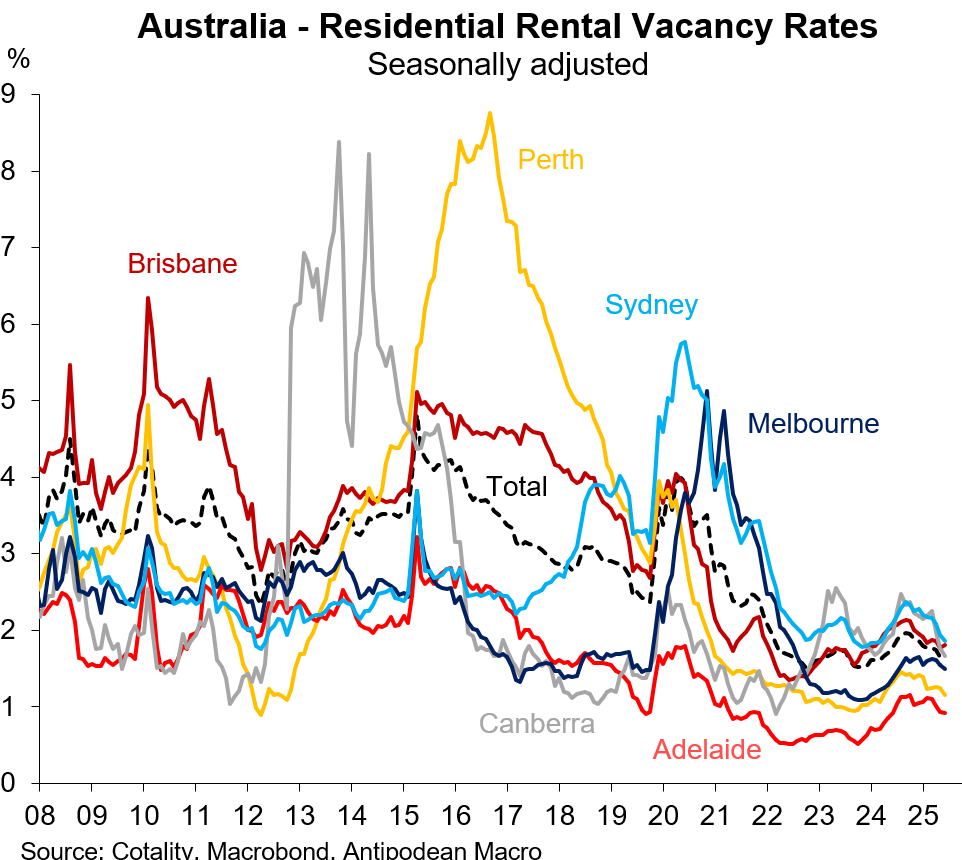

To add further insult to injury, Cotality also warned that rental vacancy rates have edged back down to historical lows of just 1.7%, while asking rents have begun to reaccelerate.

Cotality reported that median rents have increased by 43% nationally over the past five years, forcing the typical tenant household to pay $10,350 extra per year on rent.

Thus, it appears that housing affordability—both to purchase and rent—is set to worsen.