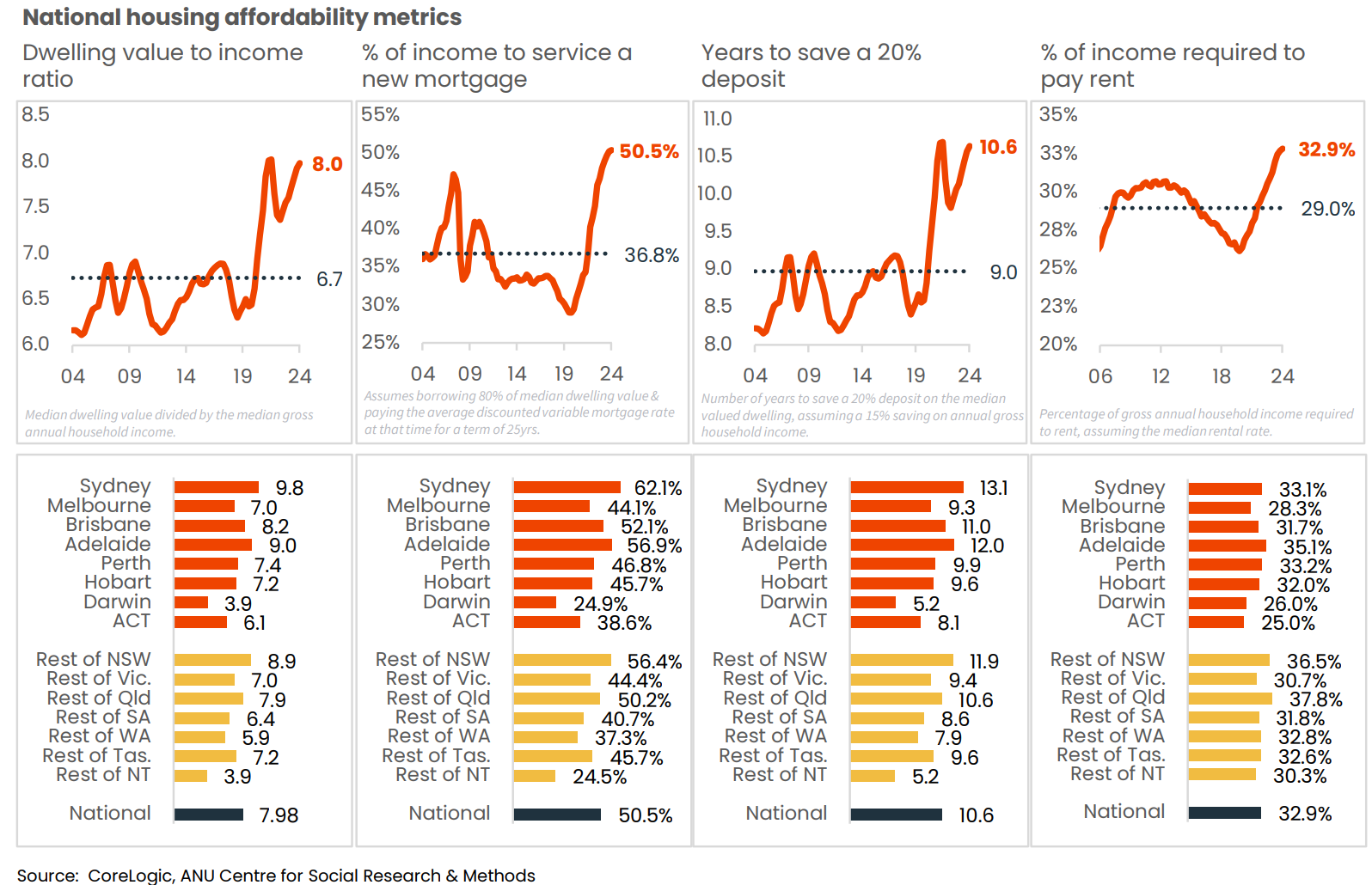

At the end of 2024, CoreLogic (now Cotality) reported that the national dwelling value to income ratio and the percentage of income required to service a new mortgage were tracking at a record high.

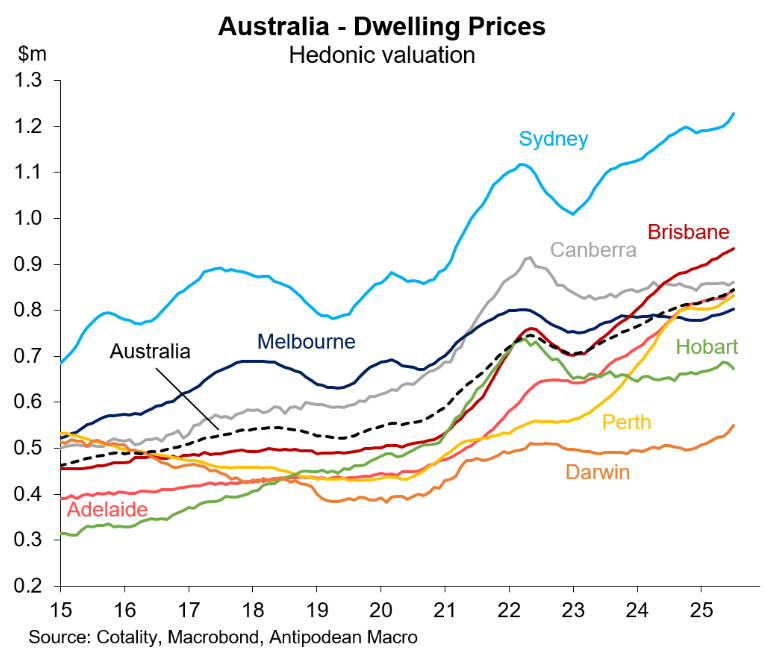

Cotality’s July housing report showed that the median dwelling value across Australia’s capital cities was $926,854 at the end of July.

As shown below by Justin Fabo from Antipodean Macro, Sydney ($1,228,435) and Brisbane ($934,623) were Australia’s two most expensive housing markets at the end of July, following growth of 35.5% (Sydney) and 76.3% (Brisbane) over five years.

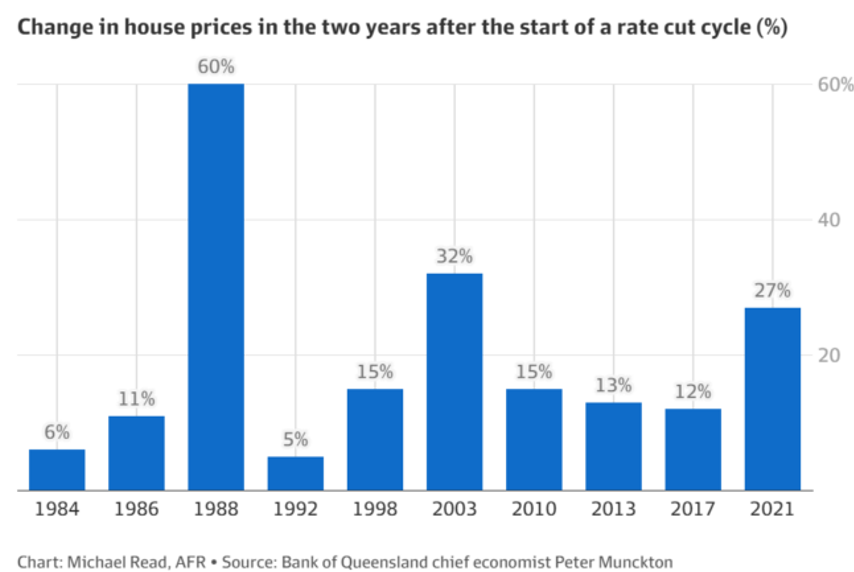

Recently released analysis from the Australian Financial Review showed that Australian dwelling values typically increase by a double-digit percentage two years following the commencement of a rate-cutting cycle by the RBA:

However, Cotality Australia Research Director, Tim Lawless, noted that while “the rate cut is a net positive for housing markets, supporting demand through increased borrowing capacity and loan serviceability”, stretched affordability is likely to keep the housing market in check.

“Although rates are coming down, they are doing so from a high base, and monetary policy settings remain in restrictive territory”, Lawless noted following the latest rate cut from the RBA.

“Even if interest rates decrease by another 50 basis points to 3.1%, the cash rate would only be around neutral territory. Prior to the pandemic, the decade average cash rate was just 2.55%”.

“Overall, we expect housing markets to respond positively to the rate drop, which is occurring against a backdrop of low supply. However, stretched housing affordability and prudent lending standards are likely to temper the upswing”, he said.

Aside from several more expected interest rate cuts, Australia’s governments have announced several demand-side policies that will lift homebuyer demand and prices.

These policies include the Albanese government’s 5% deposit scheme for first-time home buyers, the expansion of the Help-to-Buy shared equity scheme, changes to lending rules that exclude student debts from loan serviceability assessments, and state-specific policies, including the generous shared equity scheme announced in the most recent Queensland state budget.

Earlier this month, Tim Lawless cautioned that Australian home values could increase by as much as 13% by the end of 2026, in line with the Australian Financial Review’s analysis above.

As a result, the median value of Australian housing relative to incomes is projected to increase from 8.0 times at the end of 2024 to 8.4 times the median household income.

Therefore, Australian housing is set to become structurally less affordable to purchase.

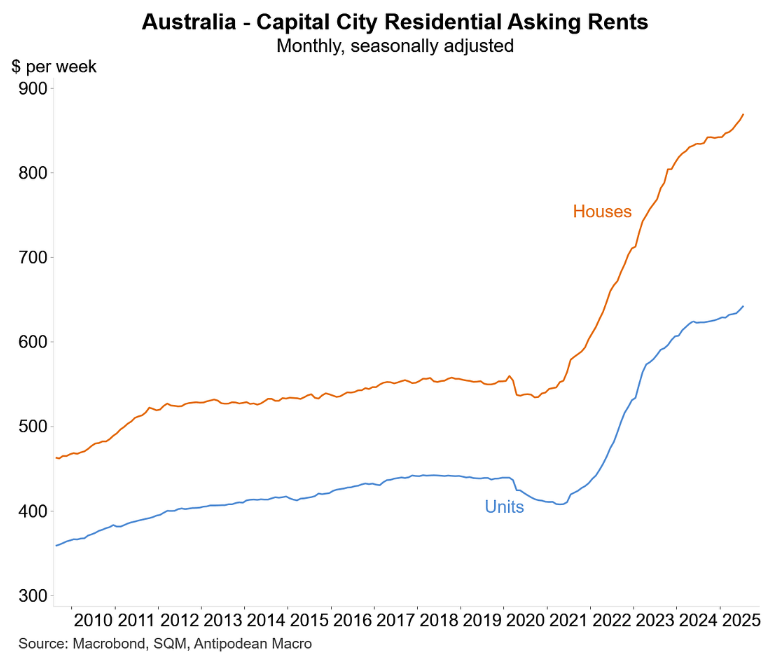

Rental affordability also continues to worsen as population demand (read immigration) continues to run ahead of supply.

In summary, there is little joy ahead for Australian tenants and first home buyers.

Slower price appreciation will merely slow the rate by which housing becomes less affordable.