Goldman with the note.

For much of the week, our Dollar views were on the wrong side of market moves, but the substantial revisions to the employment situation should, in turn, revise the emerging narrative that the FX reaction to tariffs has changed again.

On the tariff narrative, we see three key aspects to our view that the Deals should not derail Dollar downside.

First, and most fundamentally, we expect that the US will bear most of the cost of the tariffs, which will weigh on its terms of trade.

This is partly because of the breadth of the tariff increases, which will make it difficult for US firms and consumers to find suitable substitutes.

This is where we disagree with the market and media narrative this week that individual deals were more negative for trading partners because of the disparity in tariff rates.

We think it is likely that the sequential announcements drew attention to individual deals, while the overall picture is still one where the US effective tariff rate will rise the most, and relative competitiveness of foreign exports will not change much.

Second, it is likely that a part of the Dollar’s depreciation in April stemmed from expected US underperformance—as the elevated occurrence of “sell America” days demonstrates—and arguably that has looked less compelling lately.

This is where the NFP revisions are most important, as they change the picture from the labor market looking—in Chair Powell’s words—“quite solid” to now aligned with the softer growth data.

The revised data now show a slowdown that is much closer to initial market expectations for a sooner, sharper decline in activity data, even as our economists’ earlier analysis suggested that slowdown risks were most acute in mid-to-late summer (i.e., now).

Third, we and others noted that part of the Dollar’s decline was due to the back-and-forth nature of the implementation and hard-to-pin policy goals.

Admittedly, this has changed somewhat—or at least has become less surprising—since the initial Liberation Day market response, and it is hard to make an exact attribution to each of these factors.

But we think concerns over institutional governance will continue to weigh on the Dollar.

And while rate cuts are not required for further Dollar downside, they obviously would still help.

With the changing labor market landscape, we expect markets will price some likelihood of nearer, deeper and faster Fed cuts.

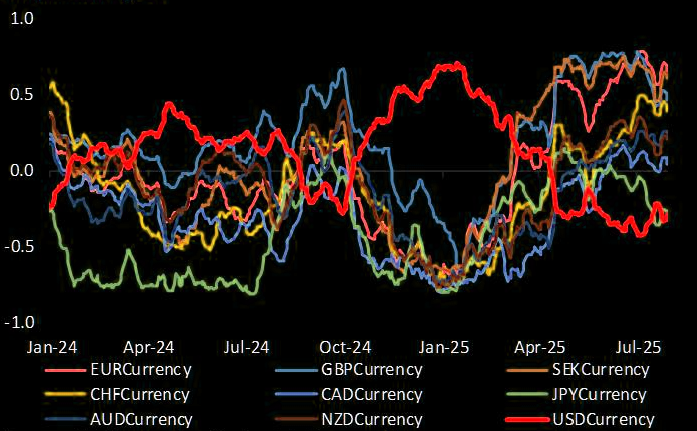

The world is already very short DXY.

This leaves the currency ready to bounce on the slightest good news.

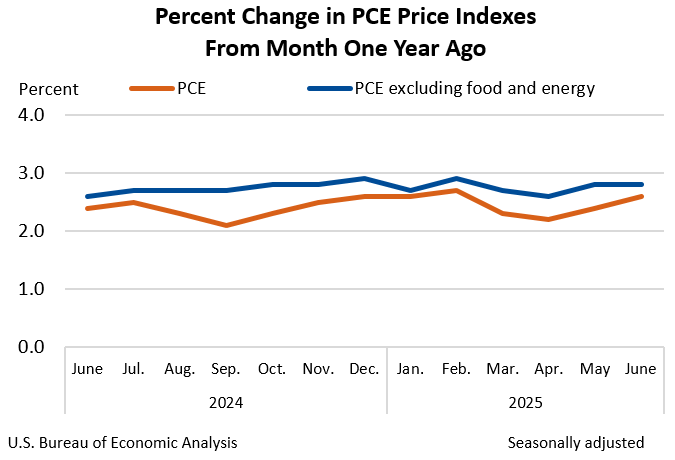

If Americans are going to pay for the tariffs, then a warming PCE is not going to stop through H2, and it is well above the Fed’s 2%.

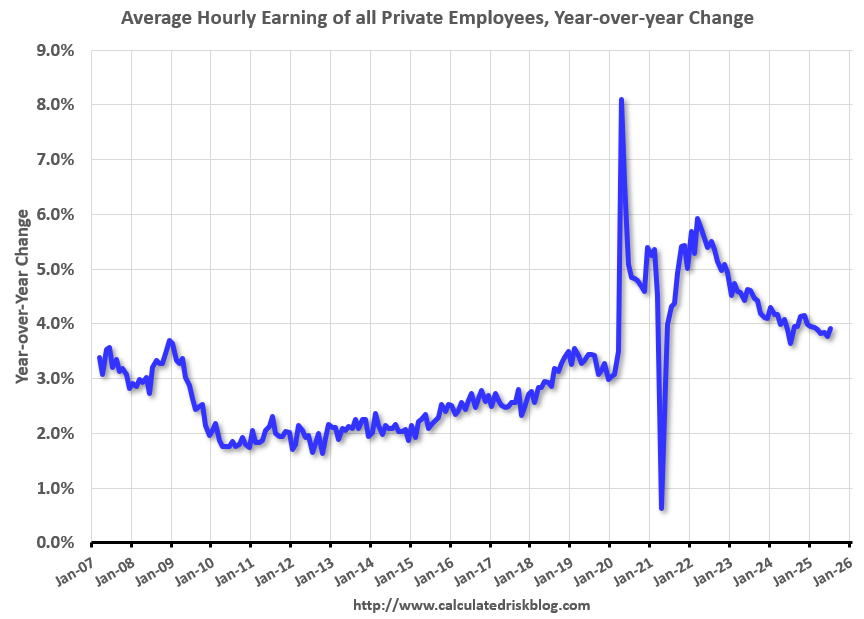

Moreover, wages are firm despite weak jobs, as collapsed immigration holds the unemployment rate down.

I don’t see the Fed panicked into stagflationary cuts, which means intensifying pressure from the White House

AUD whiplash is set to continue.