DXY fell last night.

AUD bounced but it’s not exactly tearing the roof off.

Lead boots are stuck fast.

Gold was disappointed.

Base metals are king dollar playthings.

Big miners are having another crack at the big bear.

EM at the highs.

Junk breaking out. Bullish.

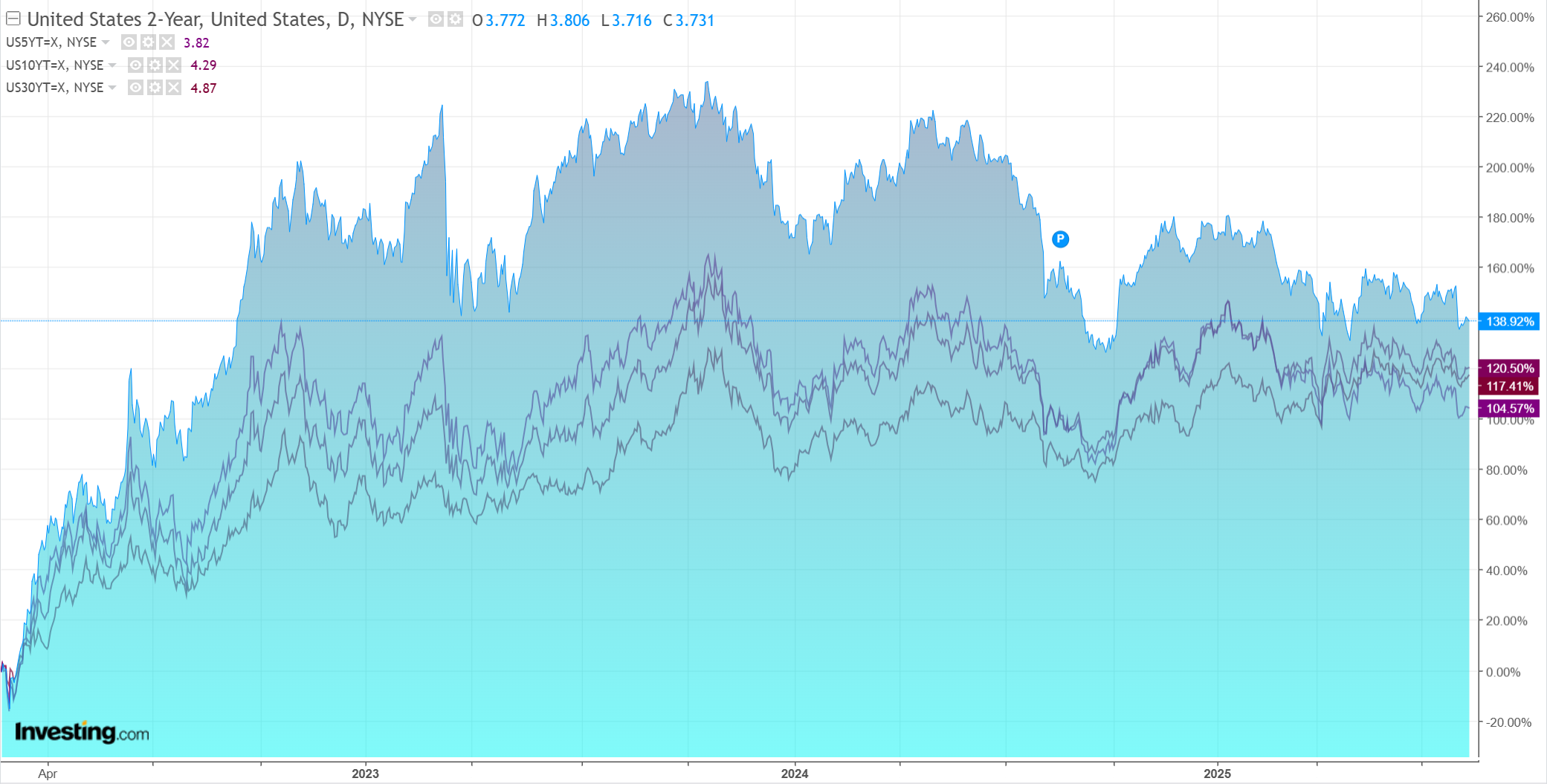

Yields muted after US CPI.

Stocks certain of Fed cuts.

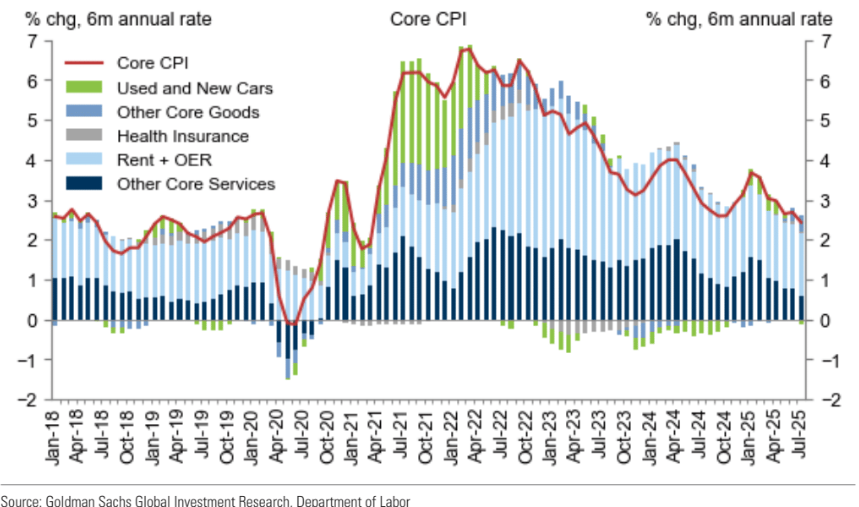

US CPI was pretty warm and, oddly, the mix was bad, with services leading the way higher, not goods. Still, the PCE calculation came down and was rocket fuel for the blowoff. Goldman.

July core CPI rose 0.32% month over month, in line with expectations, and the year-over-year rate rose to 3.06%.

The volatile airfares component boosted the core by 4bp in July, and the medical care services component boosted the core by another 7bp, partially reflecting the largest month-over-month increase in dental services CPI on record (+2.7% month-over-month).

On the negative side, lower hotel prices exerted a 2bp drag on the core in July.

Based on the details in the CPI report, we estimate that the core PCE price index rose 0.26% in July (vs. our expectation of 0.31% prior to today’s CPI report), corresponding to a year-over-year rate of +2.88%.

I wouldn’t be cutting if I were the Fed, but the market is convinced, so, at this point, it would be curmudgeonly to resist.

On the other hand, the RBA’s hawks are breaking down, so it’s now a race to the bottom.

With the big short in the AUD and DXY, chaos will continue, but I can’t see the AUD flying much higher.