DXY is dropping again.

Sticking with the recent rally pattern, AUD is not rising as fast.

Lead boots are stable.

Gold is firm, oil weak.

Metals tracked DXY.

Big bear intact.

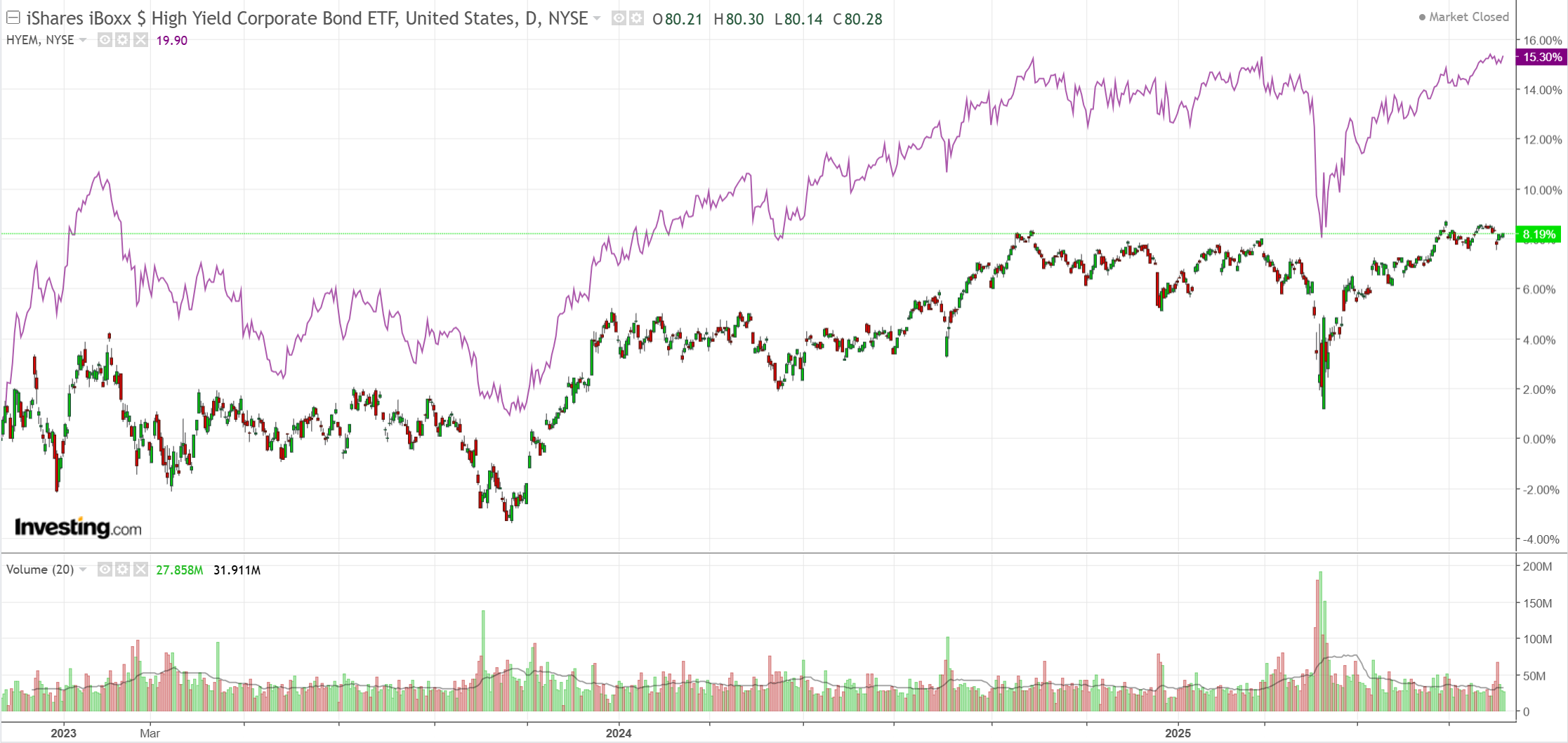

EM rebound.

Junk too.

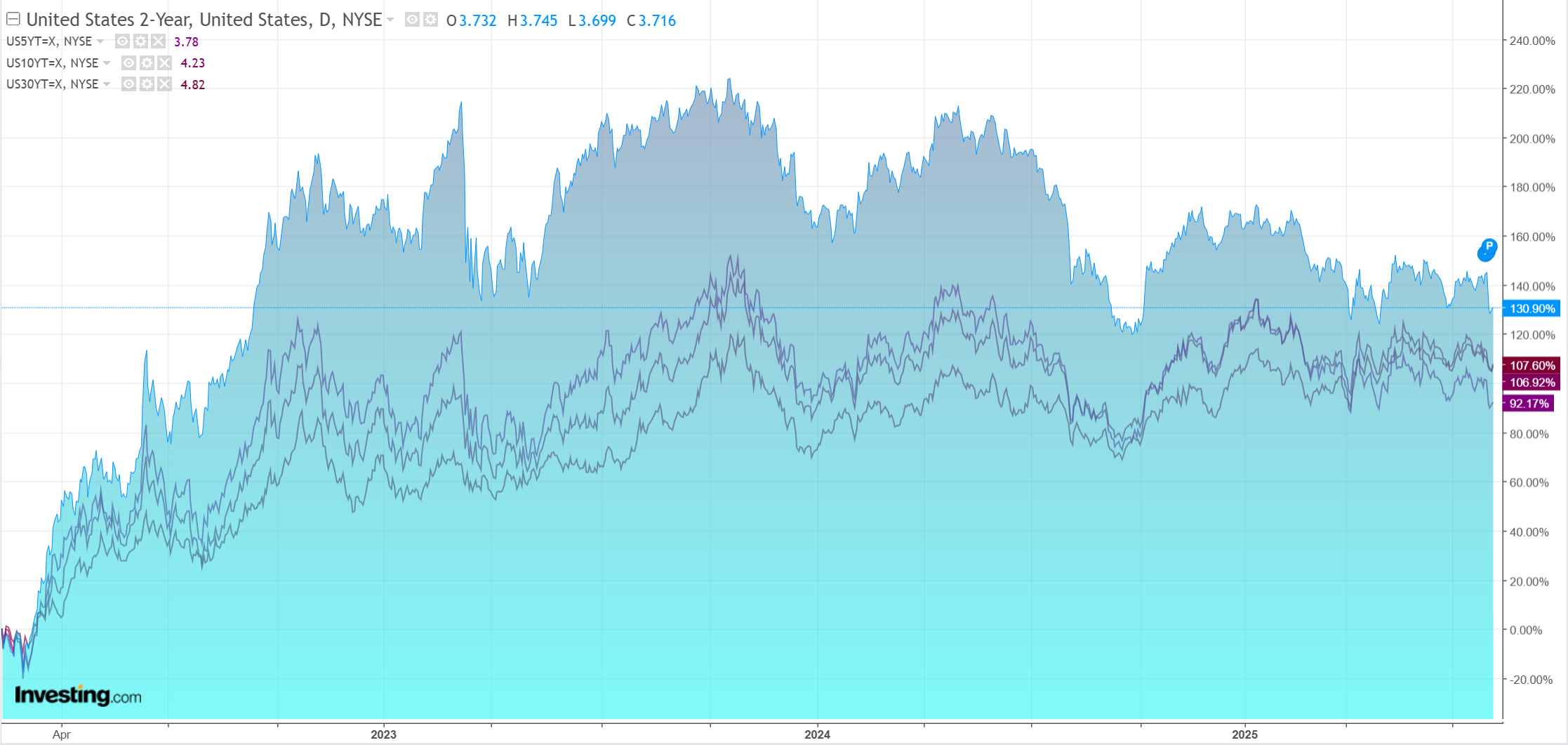

Yields firmed.

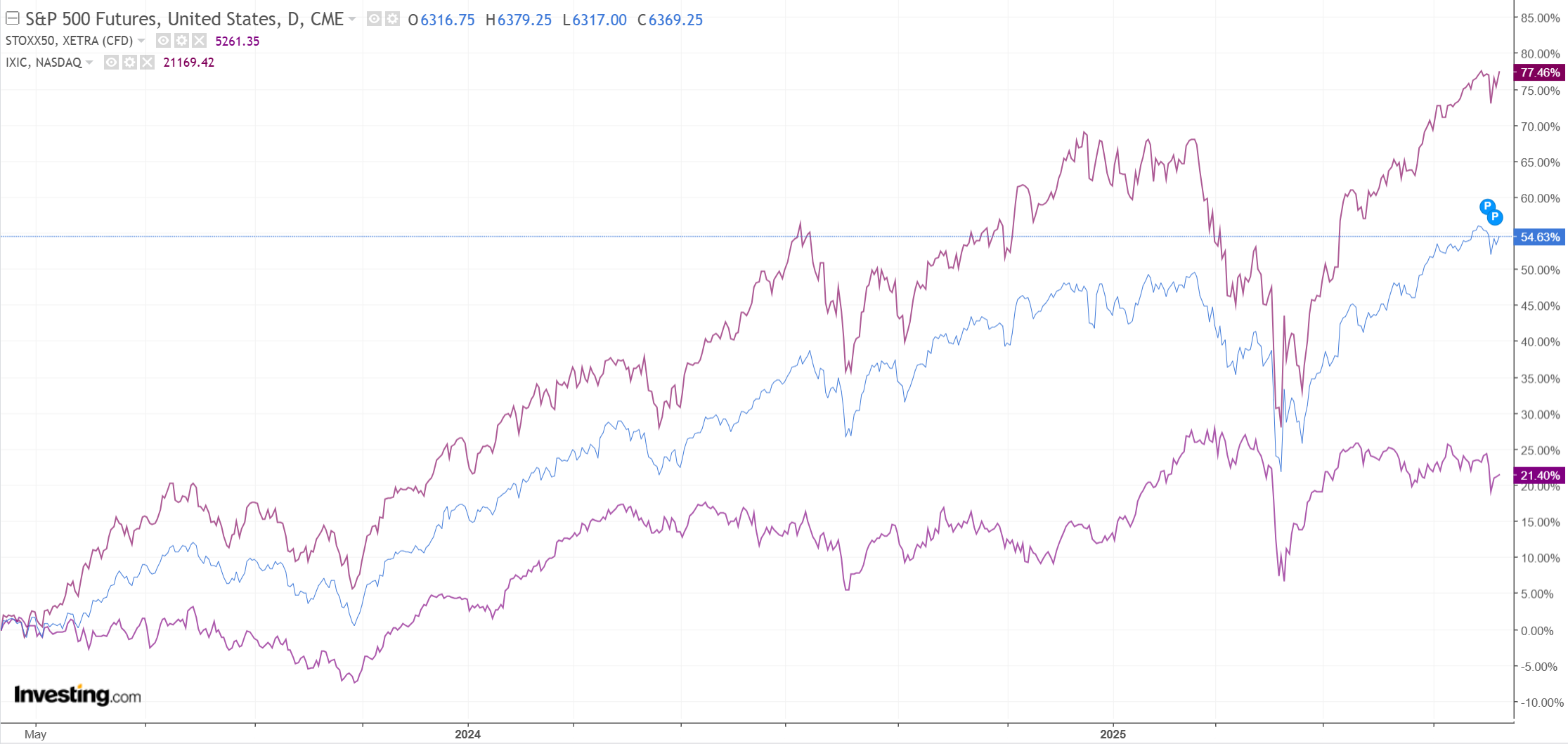

BTFD!

The AUD has resumed rising with broader risk. Or, should we say, resumed inflating with the broader bubble.

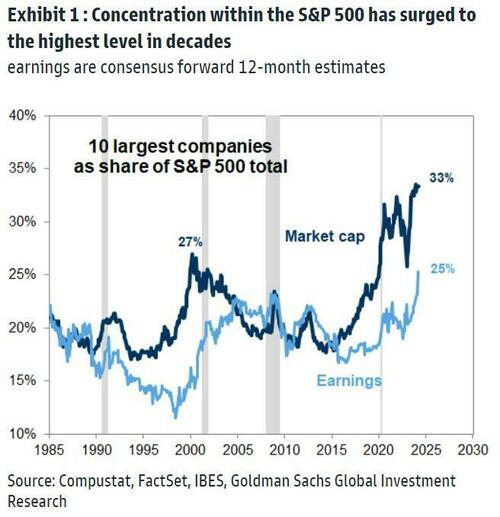

It is perilous looking for tops in bubbles, the AI version being no exception. As BofA recently pointed out, railway stocks were double the market concentration of the AI in the 1920s before they came apart.

There is, increasingly, an economic distortion coming with this. The AI capex build-out, which is in full swing in data centres, is threatening to tip next into power stations.

If AI does not live up to the hype, or even if it does but is commodified along the way, then this investment is not going to get a satisfactory return.

And a lot of it is buried in the balance sheets of the ten largest US companies.

For now, it is an academic question as Fed cuts loom to stoke this frenzy into some final blowoff. But, an apposite question is, would the bursting of this bubble derail or lift the AUD rally?

In the 2000 case, the bursting tech bubble witnessed one of the greatest surges in the AUD on record as it doubled to 2008.

That will not happen again given the relentless Chinese decline.

But it is a salient lesson for AUD bears.