Deutsche this time.

Nature of the USD move shifting to a more AUD-supportive one:As we’ve noted, a key reason for AUD’s lack of ‘high-beta’ status earlier in the year (when wer emained neutral), and our later shift to be being more bullish has been the changing volatility or risk context.

For the most part, the USD’s decline this year has been a risk-negative one (given trade, capital & other policy uncertainties), with the risk-positive elements isolated to European currencies thanks to German fiscal.

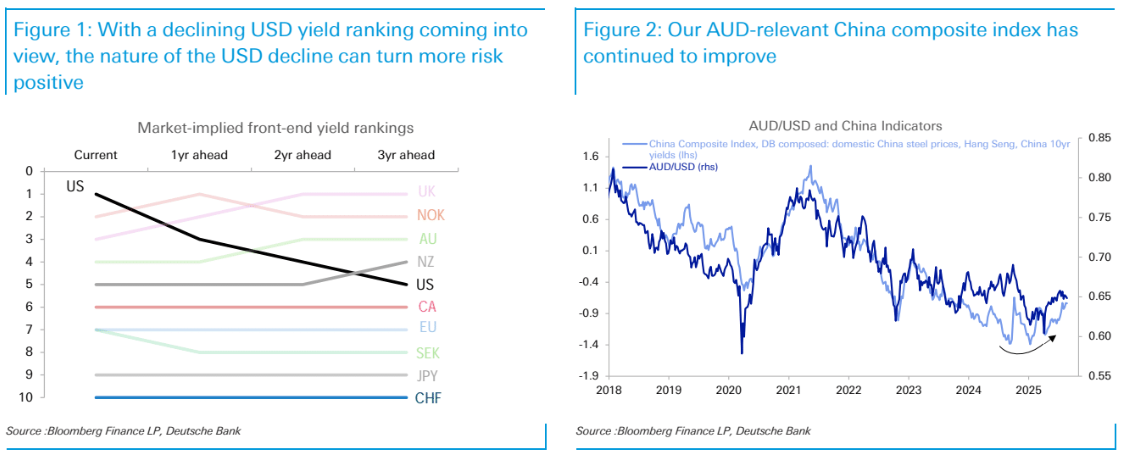

However, more recently the prospects may be rising for a more traditional low-volatility easing in the USD as the Fed eases rates vs peers, helping loosen global financial conditions, and eroding the USD’s yield ranking, as is currently priced(Figure1).

Almost all of our fundamental models suggest AUD/USD is cheap…As well as the broader risk context, AUD’s more specific fundamentals have generally continued to improve lately, broadly in-line with the outlook we depicted few months ago.

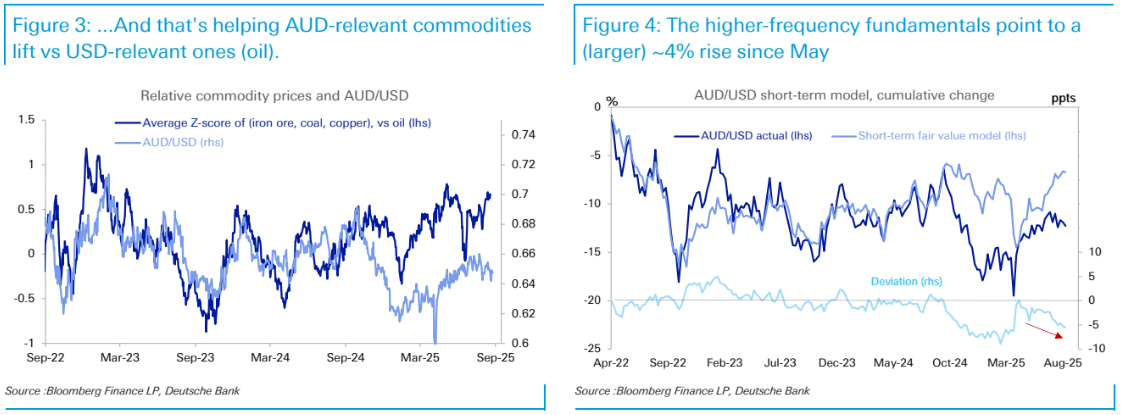

Our AUD-relevant China composite index has edged up further from its recent turning point (Figure2).

Our China economists note that supply-side measures, a ‘policy put’ on demand, as well as ample liquidity and better sentiment around tariffs are all helping support markets in China recently.

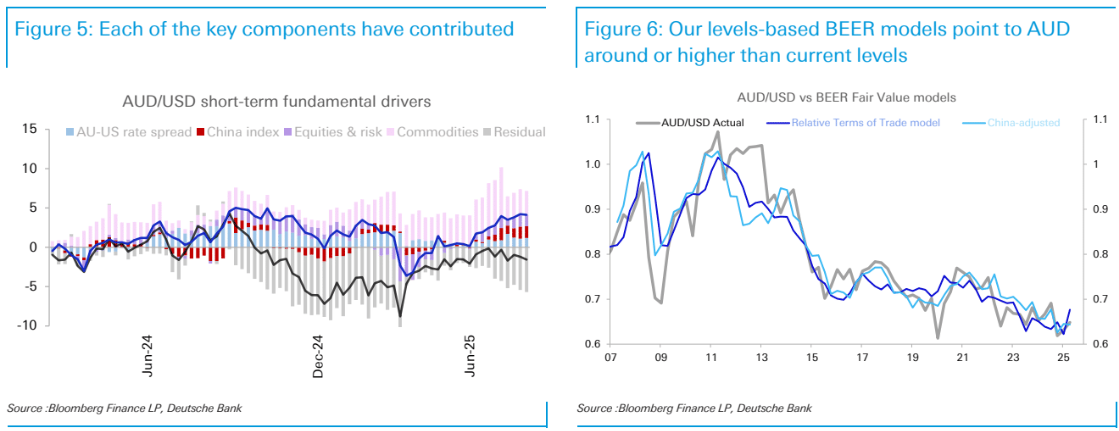

Alongside that, commodities like iron ore and coal have improved from their lows, and against softer oil prices, this has lifted our proxy for AUD/USD’s relative terms of trade – the relative commodity price backdrop – to be back around pre-liberation day highs (Figure3).

Plus rate support has also edged up in AUD’s favour (Figure5).

Feeding this through our suite of models, and the recent changes in AUD’s higher-frequency fundamentals point to a 4% rise since mid-May, or roughly 0.6850 in level terms.

Meanwhile, our more medium-term levels-based models point to a 0.68 fair value for our Relative Terms of Trade (BEER) model (accounts for the US change to net oil & gas exporter), while rate spreads on their own point to ~0.70 (Figure7).

That said, our China-adjusted BEER model (accounts for the rise of AUD’s China correlations) points to a fair value broadly in-line with current levels (Figure6), as does a simple mapping of our China composite index to AUD/USD (Figure2).

My own view is China remains stuffedand iron ore too. So I agree with Figure 2. AUD to rise slowly and not much further before it rolls next year with the Terms of Trade.