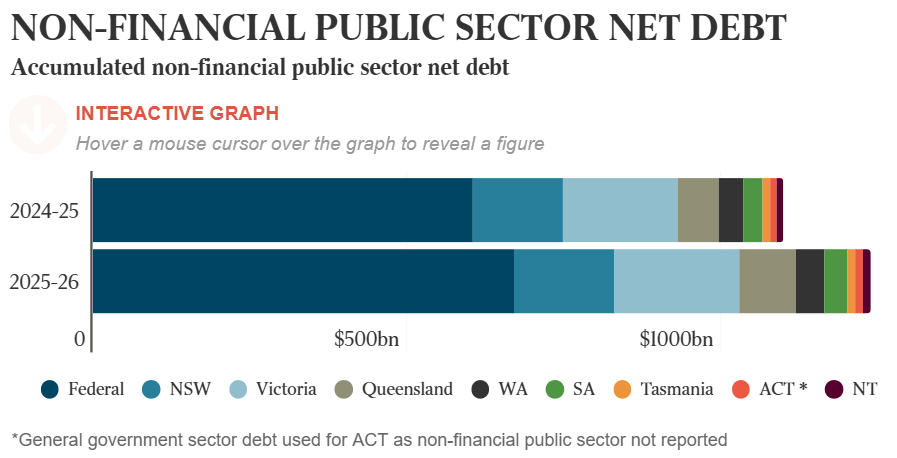

Last month, credit ratings firm S&P estimated that Australia’s state and federal governments’ combined budget deficits totalled $52 billion, with net debt exceeding 60% of GDP.

This translates to a $1,897 per capita deficit and a net debt of $45,183 per person.

Meanwhile, the aggregate net debt of the federal, state, and territorial governments is expected to reach $1.2 trillion in 2025-26.

Federal Treasurer Jim Chalmers acknowledged that state and federal governments are under renewed pressure to tighten their fiscal positions, and they must all make painful decisions to make their budgets more sustainable while still funding essential services.

“We’ve all got difficult decisions to take to make our budgets more sustainable and to fund the critical services the people we represent rely on”, Chalmers said. “Whether it’s the budgets in Queensland, NSW yesterday, the ACT … I try not to engage in the running commentary”.

Independent economist Saul Eslake cautioned that the surge in state debt will negatively influence the federal government’s credit rating, as it is the guarantor of state debt. Given the federal government’s implicit guarantee of the banking sector, any downgrade of its credit rating may raise mortgage borrowing prices.

“The state debt is a direct threat to commonwealth credit rating, too, because the commonwealth guarantees the states. The commonwealth rating is then a threat to Australia’s banks because they can’t have a higher rating than the sovereign”, Eslake said.

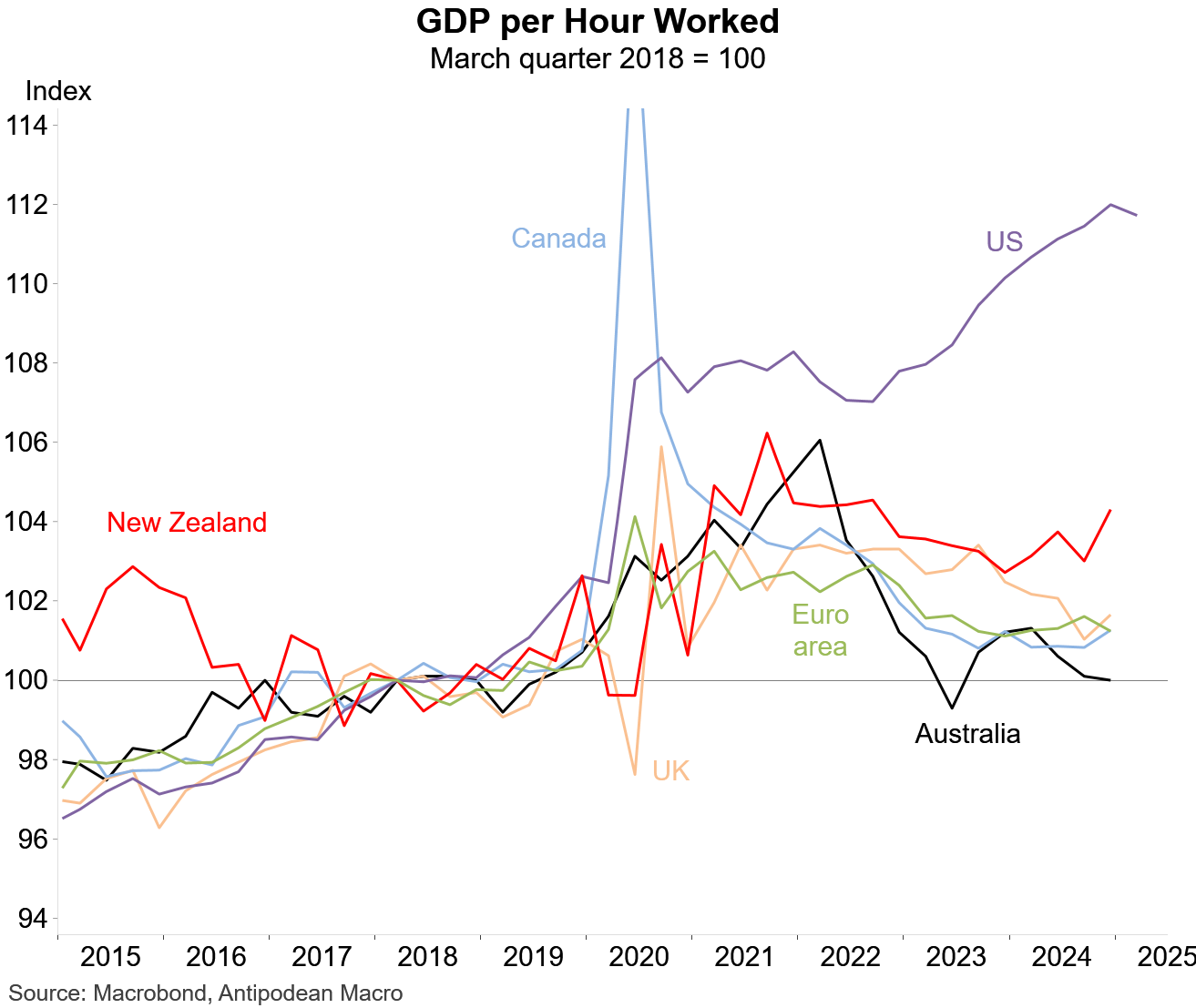

KPMG chief economist Brendan Rynne likewise warned that budget finances are “more challenging now than ever because the states’ ability to repay growing debt is more limited because the biggest revenues come from GST”.

Meanwhile, leaked Treasury advice has recommended that Treasurer Jim Chalmers find “additional revenue and spending reductions” to ensure a “sustainable budget”.

“Improvements to the budget will need to come from economic growth, additional revenue and spending reductions”, the leaked advice read. “Tax should be raised as part of broader tax reform”.

Treasury’s advice comes as the federal budget faces a decade of deficits amid the unwinding of commodity prices, the ageing population, and increasing spending on aged care, the NDIS, defence, and the “net zero” transition.

The Commonwealth Bank of Australia has used its submission to a Productivity Commission review to argue that the federal government should consider major tax reform to boost productivity and ensure the sustainability of the budget.

Their recommendations include income tax relief, a cap on superannuation concessions, the introduction of a wealth tax, and changes to the goods and services tax (GST).

The CBA also contends that other reforms aimed at lifting productivity are a higher priority than company tax cuts, putting the bank at odds with the Business Council of Australia (BCA).

“Australia needs to find a way to lower its dependence on income taxes”, the CBA submission said. “We believe it should be possible to achieve a revenue-neutral but more sustainable tax mix through a package of measures”.

“Australia’s prosperity has been built on waves of reform to align our tax system to the economic demands and opportunities of the time”.

“We now need to catalyse the next wave of tax reform debate, which should include the appropriate levels and role for consumption and wealth taxes, for distributional fairness, and incentivising productive activity in the economy”.

“We would support a superannuation cap, set at a level that encourages aspiration, and set well above the level where there is dependence on the state for support in retirement”, the CBA said.

The CBA added that the Henry Tax Review from 2010 was “a sensible starting point” to launch a national conversation about tax reform.

I couldn’t agree more. The Henry Tax Review laid out the blueprint for fixing Australia’s tax system 15 years ago. Everything should be on the table, including raising the GST.

It is crucial to shift the tax burden from workers through personal income taxes to resources, wealth, and consumption.

Australia should also eliminate inequitable and costly tax breaks, such as those related to superannuation, property, and electric vehicles.

More broadly, Australia is rich in natural resources, including some of the world’s largest deposits of iron ore, natural gas, coal, nickel, lithium, uranium, and others.

Australia has everything the world requires except oil.

Given its small population, Australians should be among the world’s wealthiest, with robust public finances.

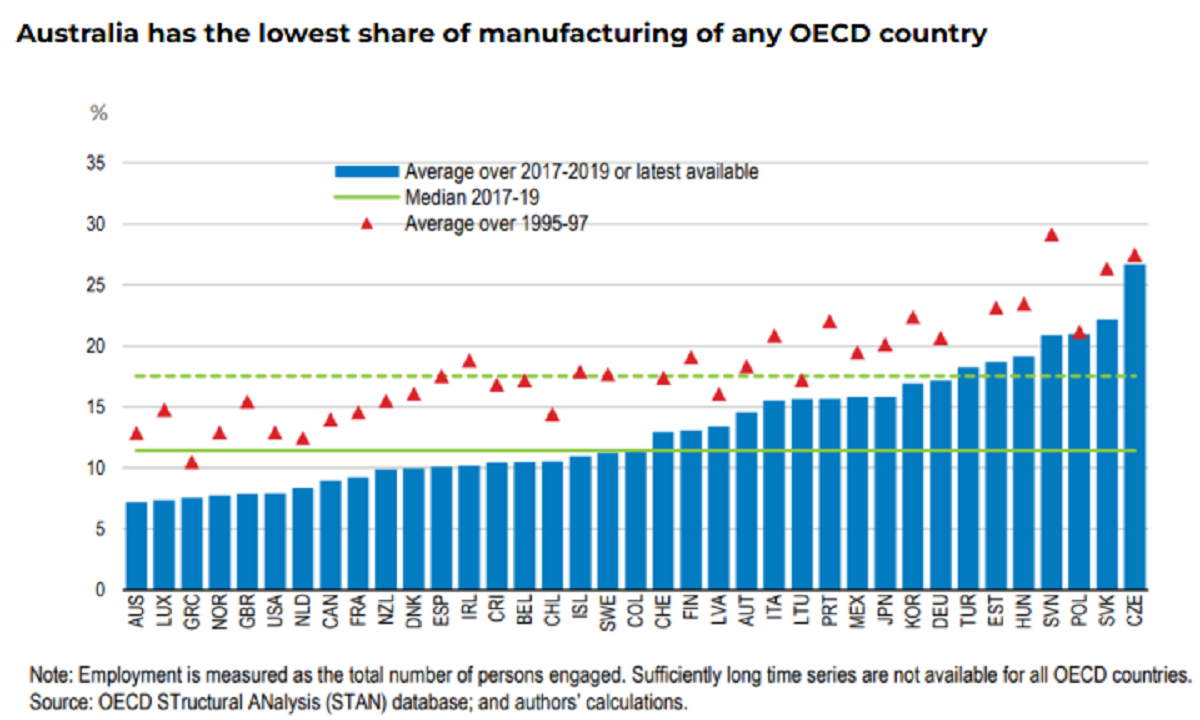

However, Australia fails to tax its resource exports appropriately. It charges its residents exorbitant costs for their use (e.g., East Coast gas), driving up inflation and the cost of living while decimating its manufacturing base.

Australia also intentionally distributes its mineral wealth among more people by operating one of the world’s largest immigration programs, making residents poorer per capita and undermining living standards through higher housing costs, congested infrastructure and services.

As a result, Australia now has a low-productivity economy that is struggling to fund infrastructure and services for its rapidly growing population.

From an economic perspective, Australians are like frogs being slowly boiled, with falling living standards.

The first action Jim Chalmers should take is to stop digging a deeper hole. Put an end to mass immigration’s ‘stupid growth’ model. Then, undertake fundamental tax reform based on the Henry Tax Review, with resource taxation at the forefront.

If in doubt, try to mimic Norway, which has become one of the world’s richest and well-functioning countries by correctly taxing its resource wealth and firmly managing its borders.