By Harry Ottley, economist at CBA

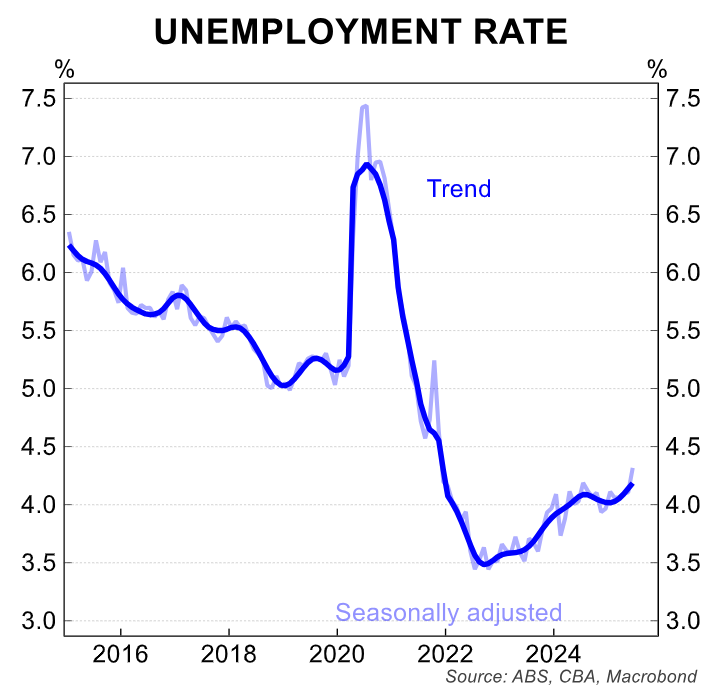

- The unemployment rate rose to 4.3% in an otherwise quiet week locally.

- Next week is quiet again. The RBA minutes and a speech from RBA Governor Bullock will garner the most attention.

- The calendar offshore is also extremely light, with CPI in NZ and the ECB policy decision the only events of significance.

The local data flow was light on this week in Australia. The labour force survey on Thursday was the clear highlight. It proved another soft report, with employment broadly flat and the unemployment rate ticking up 0.2ppts to 4.3%—the highest level since November 2021.

The survey can be volatile, but the unemployment rate has been trending broadly sideways for a year or so. A shift higher in the unemployment rate therefore means it has caught the attention of analysts and financial markets. Given the inherit volatility in the survey and some quirks in the rotation groups, we are not confident yet that the loosening in the labour market has materially picked up steam. But the survey has now been weak for two consecutive months.

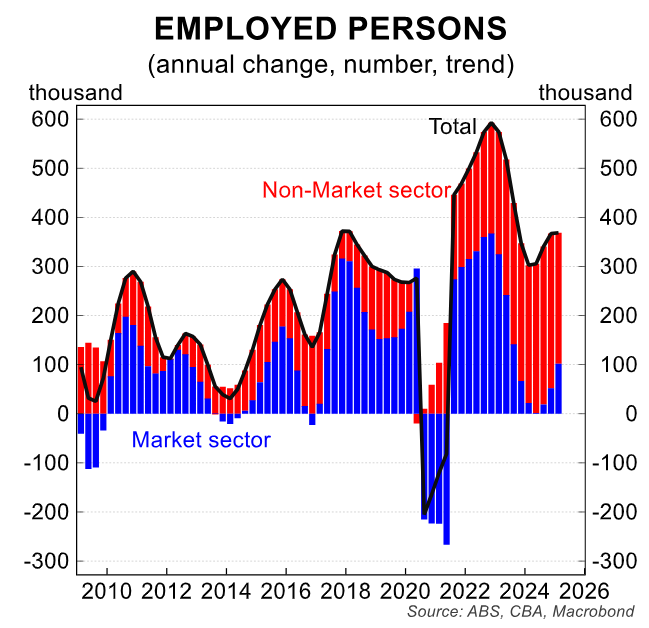

The RBA will be watching the next few months of data extremely closely. And as we have noted, there are downside risks to the labour market stemming from an over reliance on employment from the non-market sector and rising global growth concerns.

The data provides further impetus for the RBA to continue easing monetary policy in August. Indeed, it will now take an even more material upside surprise to the Q2 25 trimmed mean CPI (due 30/07) for another on-hold decision to come into play.

Next week is quiet again on the local data front. The preliminary July S&P Global PMI’s are due. But RBA communication will be in greater focus. The minutes of the July Monetary Policy Board meeting on Tuesday will be closely scrutinised given the surprise the decision gave to markets and economists.

While there will likely not be much novel information given the detail provided by the Governor’s press conference, the way the minutes address (if at all) the fact the decision was split one at 6-3 will be of interest.

Governor Michele Bullock will then deliver a speech on Thursday. There is no title currently available but the Q&A will no doubt be one to watch given the July surprise, the soft labour market data this week, and the interest in how RBA officials will communicate with the market in this new era for the RBA.

Offshore, the calendar is looking just as bare. Q2 CPI in NZ is the lone economic data point of note. Our colleagues at ASB expect headline CPI to rise by 0.6%/qtr and 2.8%/yr. This is a bit higher than the RBNZ had expected but given the broader weakness in the NZ economy, ASB expect a 25bp cut to 3.0% in August—with further cuts a clear possibility.

The European Central Bank (ECB) will meet next week. Our international economics team expects the key policy rates will be left unchanged. President Lagarde is on the record saying policy is well positioned to return inflation to target. But we see downside risks to the Euro economy in large part due to the US led trade war.

For this reason, we expect two further cuts later this year will be required.