The Reserve Bank of New Zealand paused following the RBA this week.

The decision was expected. ANZ sees it as temporary.

Our view on today’s decision was that the recent soft data justified another 25bp OCR cut, but that lingering concerns about upside inflation risks would on balance see the Committee decide to hold the OCR unchanged awaiting more CPI and inflation expectations data (as well as more evidence on whether the recovery is losing steam or just hit a pothole).

That’s pretty much how it unfolded.

Although the decision was consensus, it’s clear from the Summary Record of Meeting that it wasn’t straightforward.

We continue to expect that the data will assuage inflation concerns sufficiently to see the RBNZ deliver a 25bp cut in August.

But the RBNZ remains in data-watch mode, as do we.

We do see some upside risk to the RBNZ’s May forecast for non-tradable inflation in Q2, but over coming months we are forecasting lower consumption, a cooler housing market and softer medium-term inflation, and thus more OCR cuts to come.

Goldman is similar.

The statement also flagged a clear easing bias, noting that “subject to medium-term inflation pressures continuing to ease in line with the Committee’s central projections, the Committee expects to lower the Official Cash Rate further.”

Overall, the outcome was in line with our expectations and our base case remains for 25bp cuts in August, November and February to a terminal rate of 2.5%.

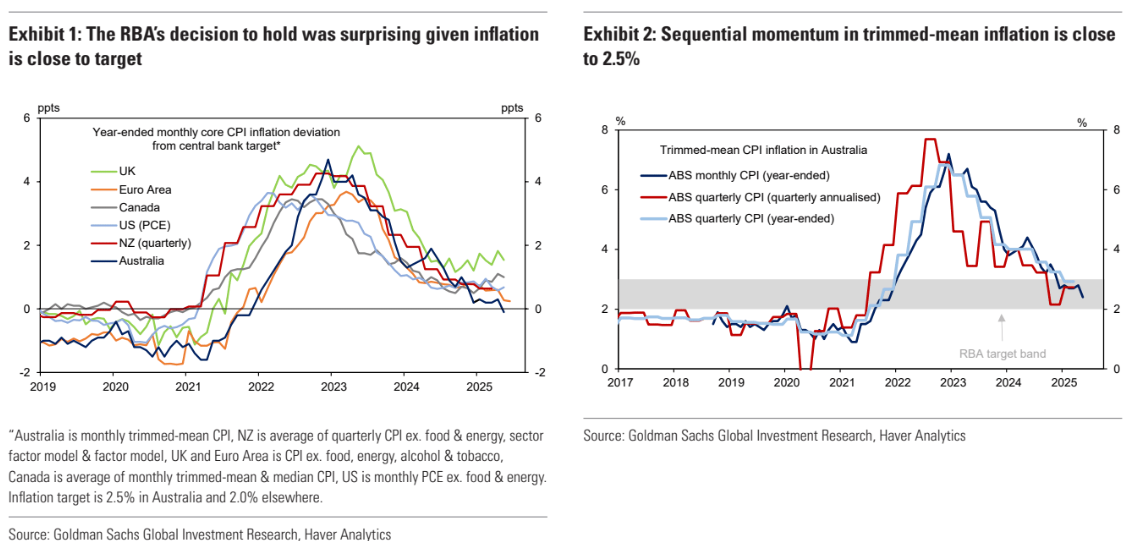

It is interesting to note that relative to the target, Australian inflation has dramatically undershot NZ.

Yet the RBNZ has slashed rates by 225bps versus the RBA’s paltry 50 bps.

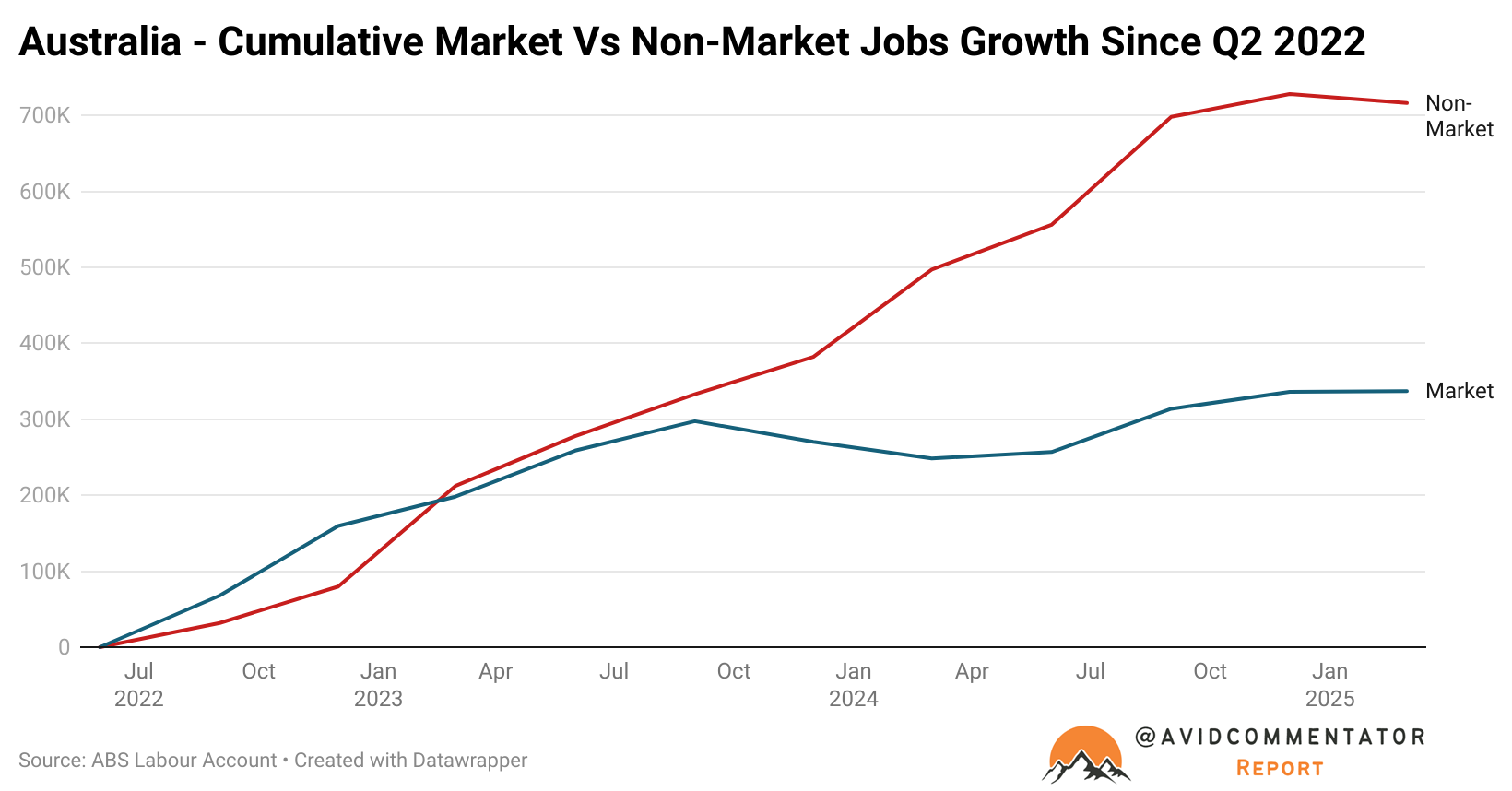

The key difference is wage growth, but leading indicators suggest Aussie wages will soften again in H2. Quite apart from the obvious pressures of the ongoing immigration labour market supply shock.

Notably, as the bedpan economy spills onto the floor.

Without further easing from the RBA, the handoff to private sector jobs will be bumpy and present further dosnide risk to wages.

As for the RBNZ, there is no reason for it to pause at all.