Advertisement

In the past week, New Zealand’s financial markets have been primarily influenced by global events, with little guidance provided by local data.

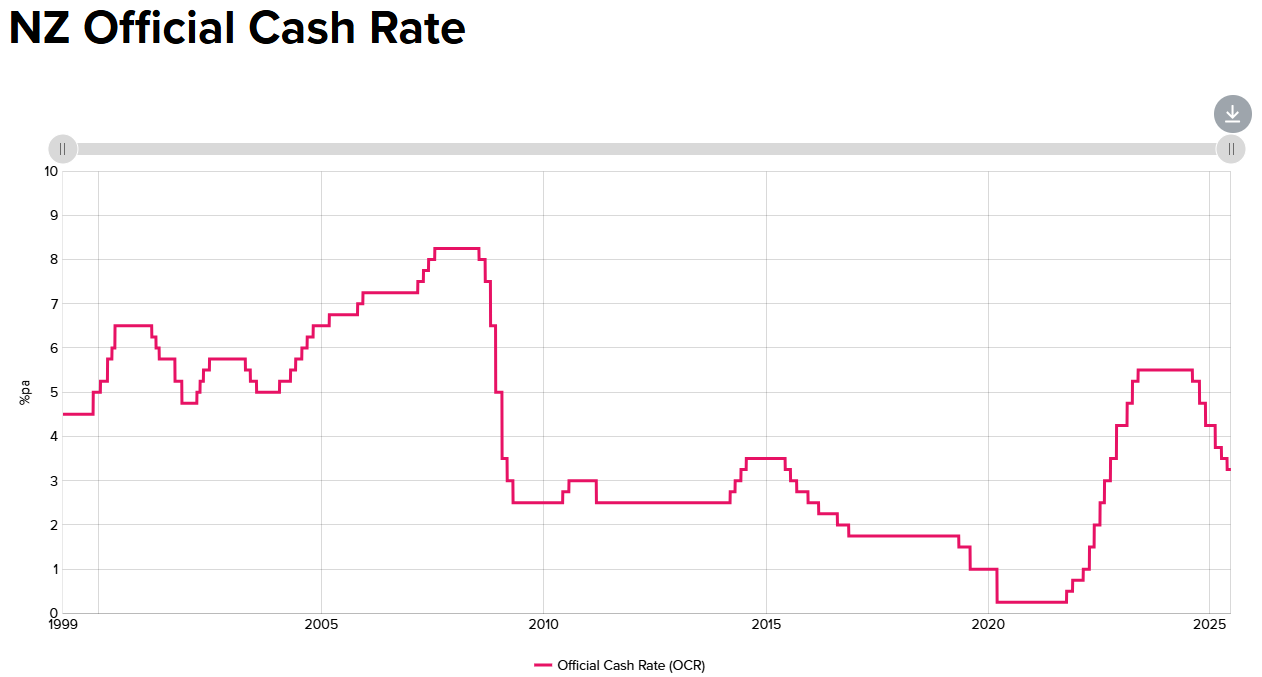

Markets continue to anticipate that the Reserve Bank of New Zealand will skip a cut at the next meeting on July 9 and then cut rates again in August.

The RBNZ has already aggressively slashed the cash rate by 2.25%.

Advertisement

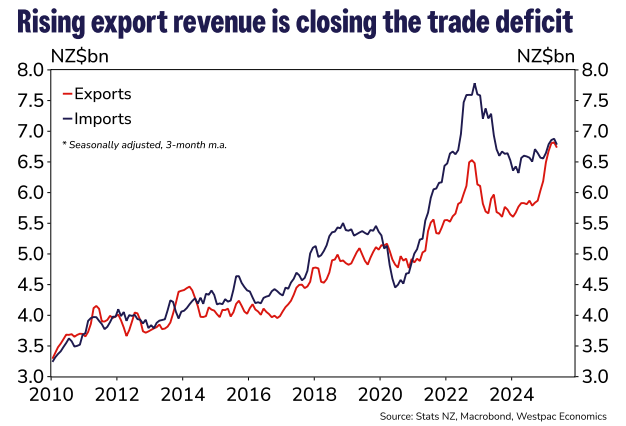

However, growth remains weak, with Q1’s strong performance largely driven by net exports.

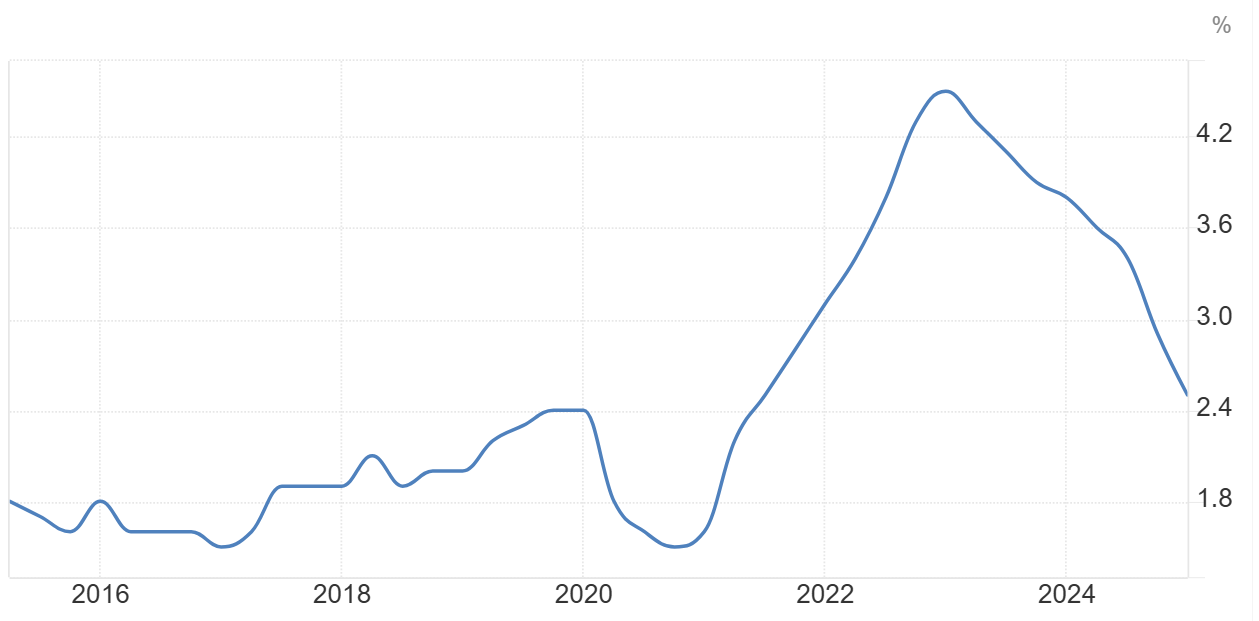

Inflation has been demolished.

Advertisement

Along with wage growth, which will continue to be crushed by strong immigration of cheap foreign labour.

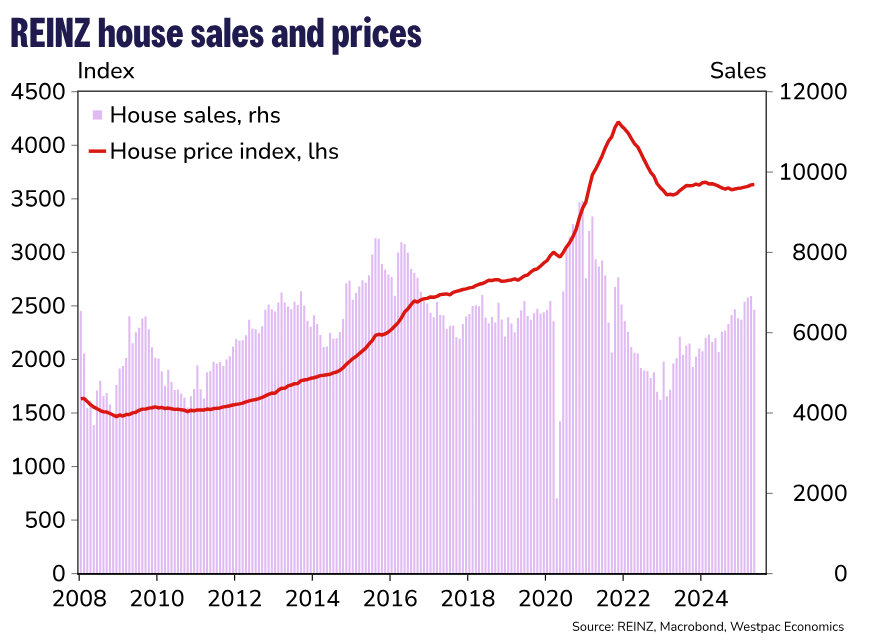

I can’t see why the RBNZ should not cut again, notably so given house prices have barely gotten off the canvas.

Advertisement

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.