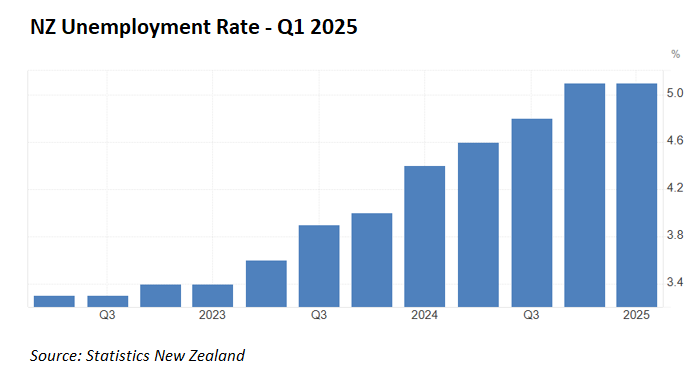

New Zealand has experienced a sharp increase in its unemployment rate, which has risen from 3.4% in Q1 2023 to 5.1% as of Q1 2025.

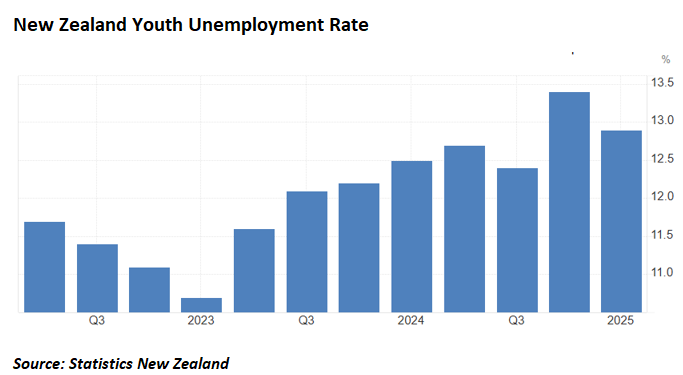

New Zealand’s youth unemployment rate has also risen from 10.7% in Q1 2023 to 12.9% as of Q1 2025. However, youth unemployment did decline by 0.5% between Q4 2024 and Q1 2025.

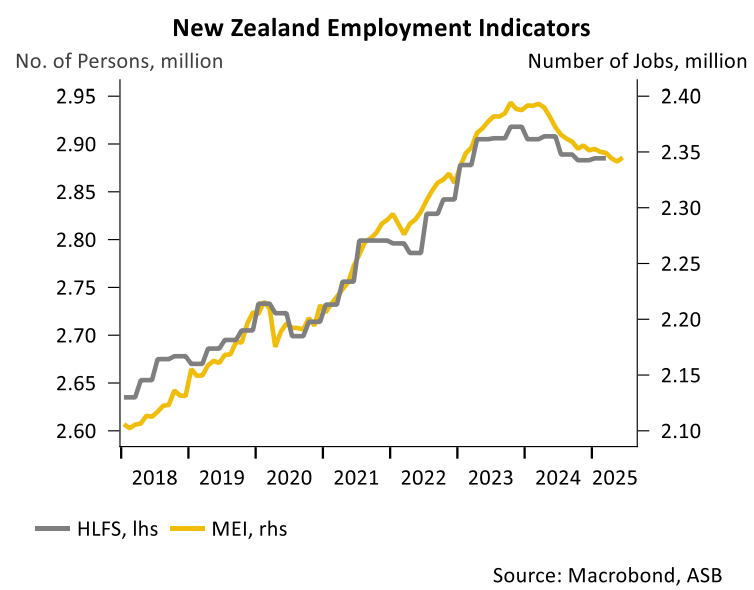

The number of people working in full-time jobs has also fallen sharply, from a peak of 2.37 million in Q4 2023 to 2.31 million as of Q1 2025.

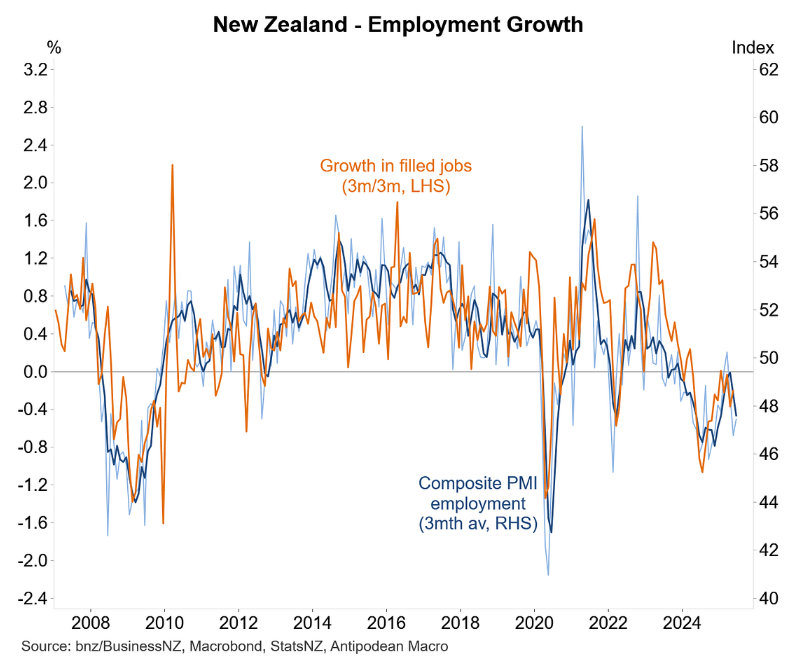

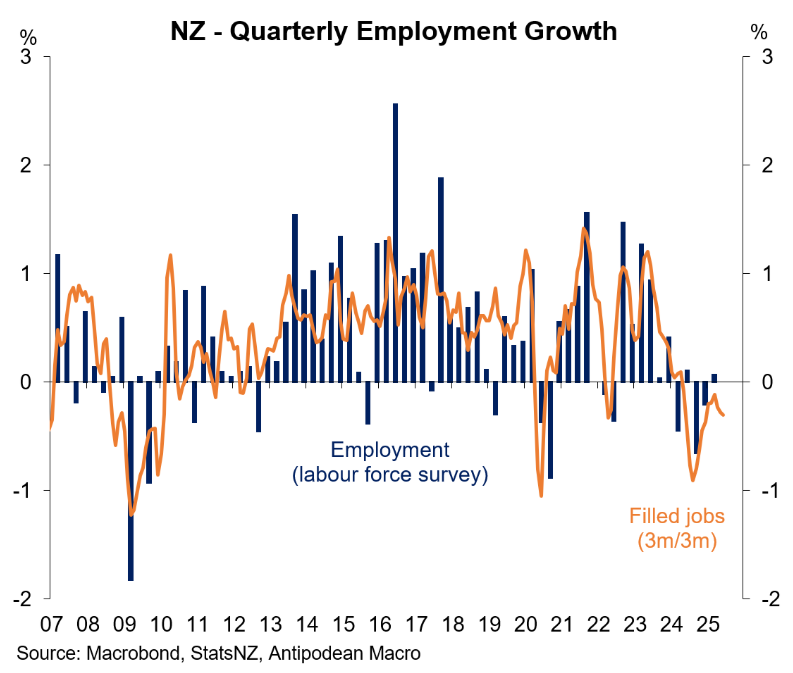

As illustrated below by Justin Fabo from Antipodean Macro, the latest composite PMI employment series is pointing to declining jobs.

On Monday, Statistics New Zealand released filled jobs data for June, which reported a small 0.1% rise in filled jobs in June, with downward historical revisions suggesting further downsizing on hiring.

Major bank ASB noted that the release suggests “a Q2 fall for HLFS employment and a slightly higher unemployment rate than the 5.2% we were expecting”.

ASB also expects the June print to be revised lower “as the downward sequence of revisions shows few signs of abating”.

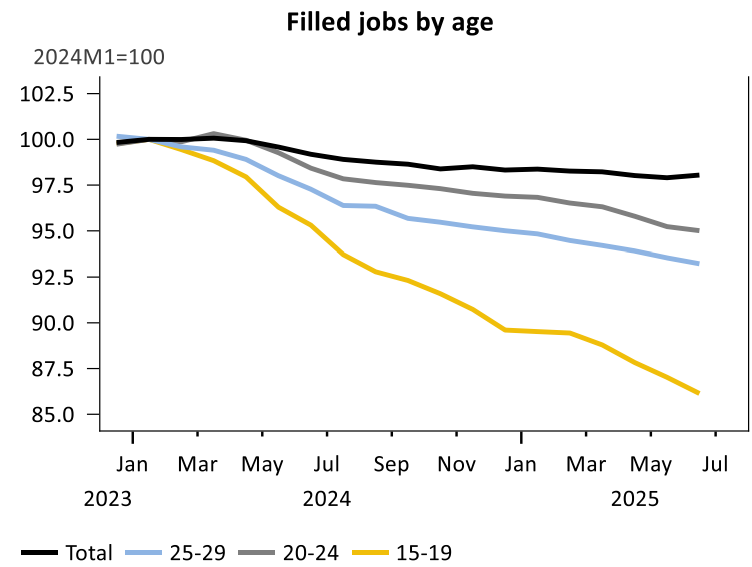

As illustrated below by ASB, New Zealand’s youth continue to bear the brunt of the labour market slowdown.

“Heavy annual falls were evident for the 15-19 age bracket (-9.6% y/y), with hiring down 3.5% y/y for those aged 20-24 and down 4.2% y/y for the 25-29 age group”, ASB noted.

Justin Fabo created the following chart plotting the monthly filled jobs series against the official quarterly labour force series. The 0.3% decline in filled jobs in Q2 does not bode well for the official quarterly data.

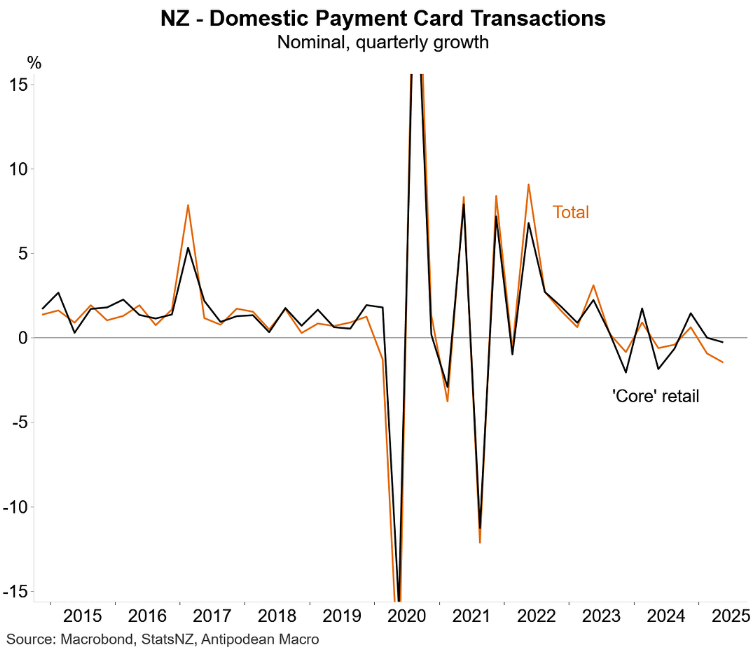

The weak labour force data follows evidence of declining consumer spending.

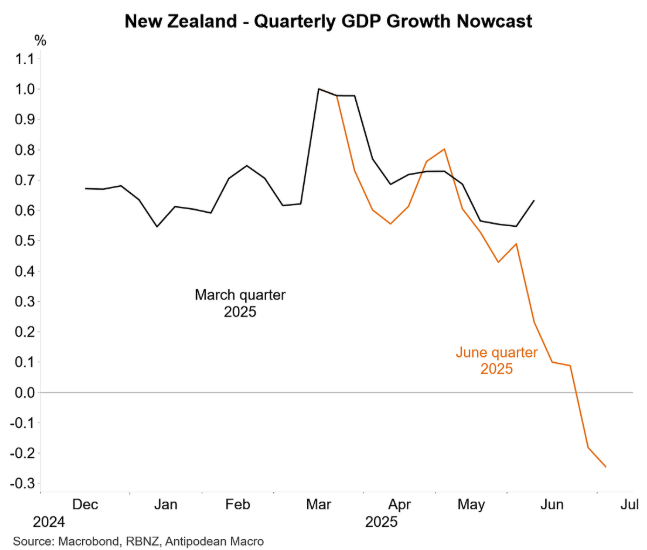

The Reserve Bank’s latest quarterly GDP nowcast has also collapsed into negative territory, falling to -0.25% for Q2 2025.

Accordingly, ASB expects “hiring to remain anaemic over much of 2025, with firms likely to remain gun-shy on expansion plans given the uncertain environment”.

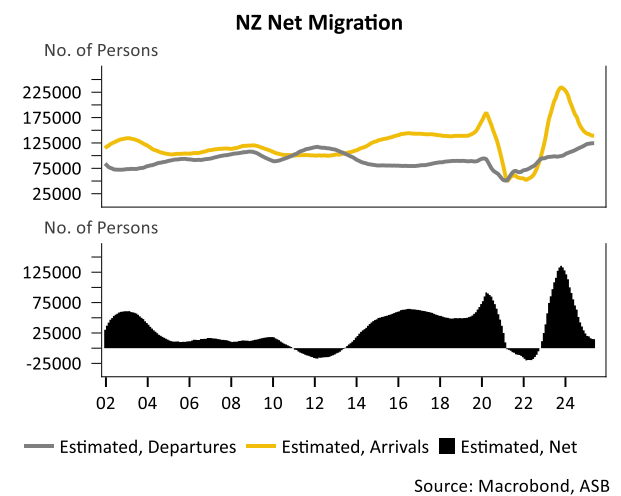

However, with net overseas migration tracking at multi-year lows, “low growth in the labour force is likely to temper the peak in the unemployment rate, which should remain in the low 5’s in the first half of this year”.

The upshot is that the combination of weak GDP growth, rising unemployment, and growing spare capacity is likely to force the Reserve Bank to cut the official cash rate (OCR) to stimulate the economy.

ABS now expects the Reserve Bank to cut the OCR by 25 bp in August, with the possibility of another cut before the end of the year.