It is amusing to watch some interest rate forecasters stick to tiny indicators. ANZ is one.

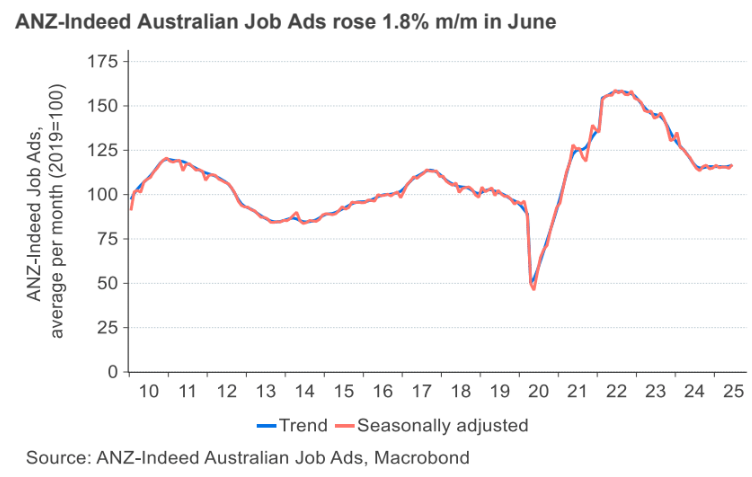

After two consecutive months of decline, the ANZ-Indeed Australian Job Ads series has bounced back, from 114.8 in May to 116.9 in June.

The unemployment rate and the hours-based underutilisation rate (a broader measure of spare capacity) have been broadly moving sideways since mid-2024.

Given the ongoing tightness in Australia’s labour market and the overall resilience in its economy, we maintain our expectation that this easing cycle will be relatively shallow.

We expect the RBA to cut the cash rate by 25bp in its July and August meetings.

I might agree, but there is no such thing as the “Australian labour market”. There is the Australindian labor market, which together combines for roughly 50m unemployed.

This pushes the Australian unemployment rate to 357%.

Wages will not break out, no matter what the RBA does, as mass immigration from India has no end.

Add to this the ongoing and intensifying terms of trade bust. This will get much worse next year as iron ore, coking and thermal coal, and LNG all tumble as supply responses crash into falling Chinese consumption.

Not to mention a global tariff shock that will be displacing goods cheaply to anybody not putting up barriers.

What we have is a near-perfect repeat of the post-2015 low-inflation period in Australia.

I do not expect interest rates to fall as far as they did in the last cycle, only because Labor governments will spend more, and regulate higher wages, than the Coalition did.

But inflation is finished, and the RBA will have to keep cutting as the immigration-led labour market expansion economic model enters another national income shock.

A 2-handle for the cash rate is about as certain as anything in Australian macro this cycle, and it could easily be a 1-handle before we are done.