After shocking economists and holding rates steady at last month’s monetary policy meeting, the Reserve Bank of Australia (RBA) stated that it was awaiting two key pieces of data before lowering rates: the June labour force report and the Q2 CPI inflation print.

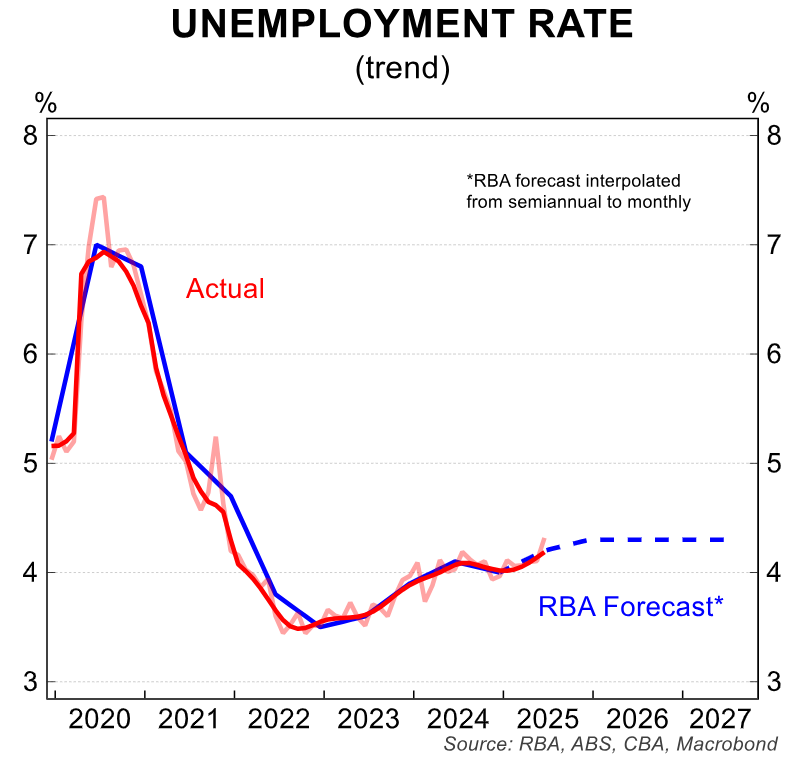

The June labour force report from the Australian Bureau of Statistics (ABS) came in far weaker than expected, with the headline unemployment rate jumping to 4.31%—above the RBA’s latest projection.

Full-time jobs also fell sharply, and the underemployment rate and hours worked also rose.

This week, we will receive the other piece of the data puzzle with the release of the Q2 CPI. Barring an unexpectedly large print, the RBA is almost certain to cut the official cash rate at its August meeting.

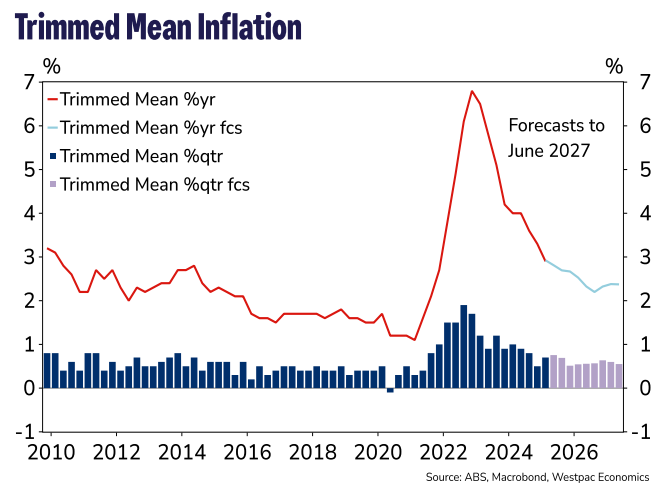

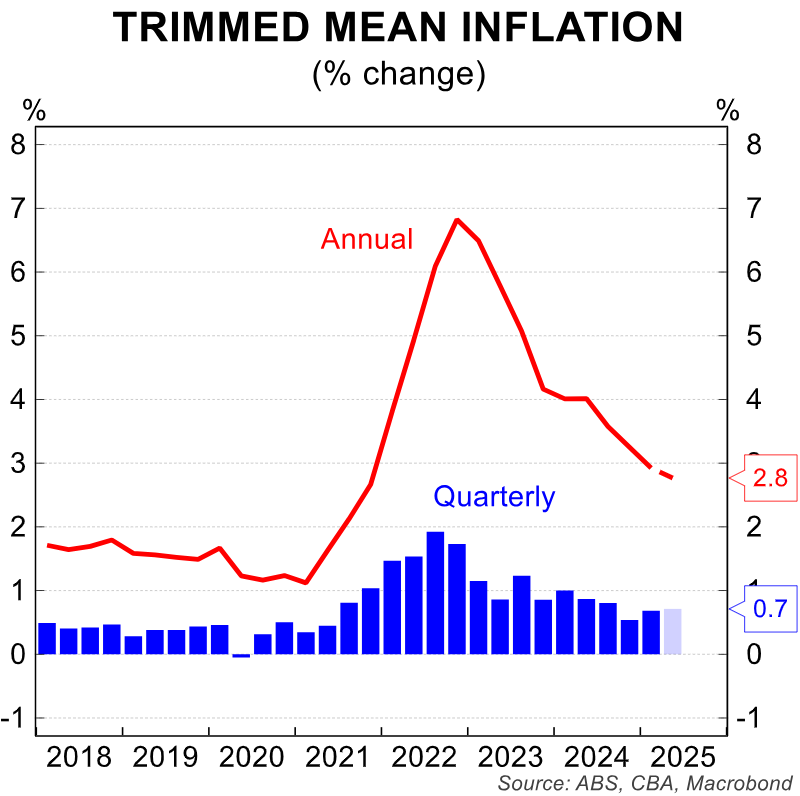

Westpac senior economist Justin Smirk believes that the policy-relevant trimmed mean inflation will print at 0.7% for the quarter, with the annual pace dropping from 2.9% to 2.7%.

“The RBA is forecasting a Trimmed Mean annual pace of 2.6%yr, which suggests a June quarter increase of 0.55% which we don’t see as enough to prevent the RBA from cutting rates at its August meeting”, Smirk wrote.

“We also think the risk to our Trimmed Mean estimate lies to the downside. At two decimal places, our Trimmed Mean estimate is 0.66% which suggests there is greater risk of a 0.6% print than a 0.8% print”.

Harry Ottley, economist at CBA, believes that trimmed mean CPI will increase by 0.7% over the quarter, “which would see the annual rate dip only marginally to 2.8%/yr–but rounding could easily see a 0.7%/qtr and 2.7% configuration”.

“If our forecasts are correct, we still expect the Board to cut the cash rate in August. But communicating the decision will need to be nuanced given the current cautious approach as well as broader concerns about the neutral rate, productivity and a labour market they still view as tight”, Ottley added.

“Our read of the communication is that the bar not to cut is high. Provided trimmed mean CPI continues to decline in year-ended terms, the Board should be confident enough to remove a bit more restrictiveness”.

“The risk in our view is for a lower outcome on the annual figure and would make that decision more straight forward”.

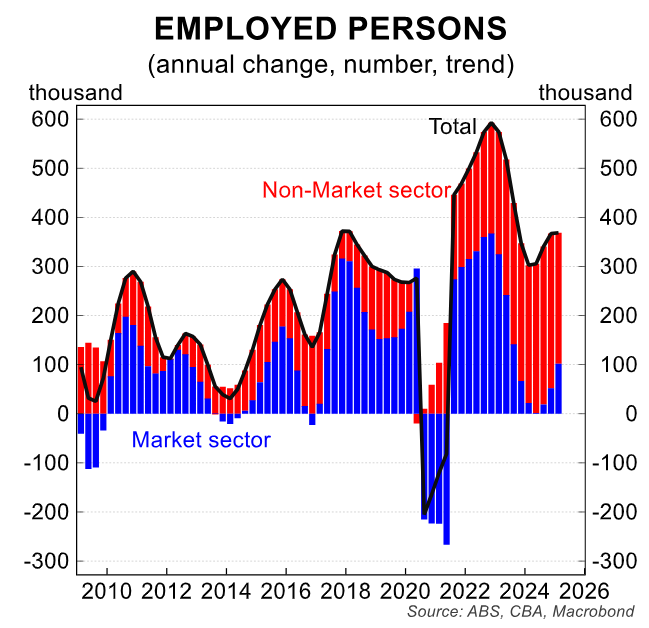

“Given the over-reliance of the non-market sector for recent jobs growth, risks to the labour market are skewed to the downside. This provides further comfort that a reduction in the cash rate is warranted even if the inflation data is a touch higher than expected next week”, Ottley said.

Financial markets are tipping the RBA to cut in August, followed by two additional 25 bps cuts by mid-2026.

If anything, risks are skewed to the downside.