The Reserve Bank of Australia (RBA) shocked economists by holding the official cash rate (OCR) at 3.85% at its latest monetary policy meeting.

The decision caught financial markets off guard, which had assigned a near 100% probability of a rate cut.

The decision was a close call, with the board voting 6-3 in favour of holding.

Alex Joiner, chief economist at IFM Investors, said that the decision “speaks to a patient RBA that isn’t in any rush to move into accomodative territory”.

The minutes of the board meeting were released on Tuesday, which explains the RBA’s reasoning for keeping the OCR on hold.

The members “believed that lowering the cash rate a third time within the space of four meetings would be unlikely to be consistent with the strategy of easing monetary policy in a cautious and gradual manner to achieve the Board’s inflation and full employment objectives”.

The board also noted that they “would receive important information before the next meeting, including another quarterly inflation report and additional information on the labour market and how the world economy is evolving, along with a revised set of staff forecasts”.

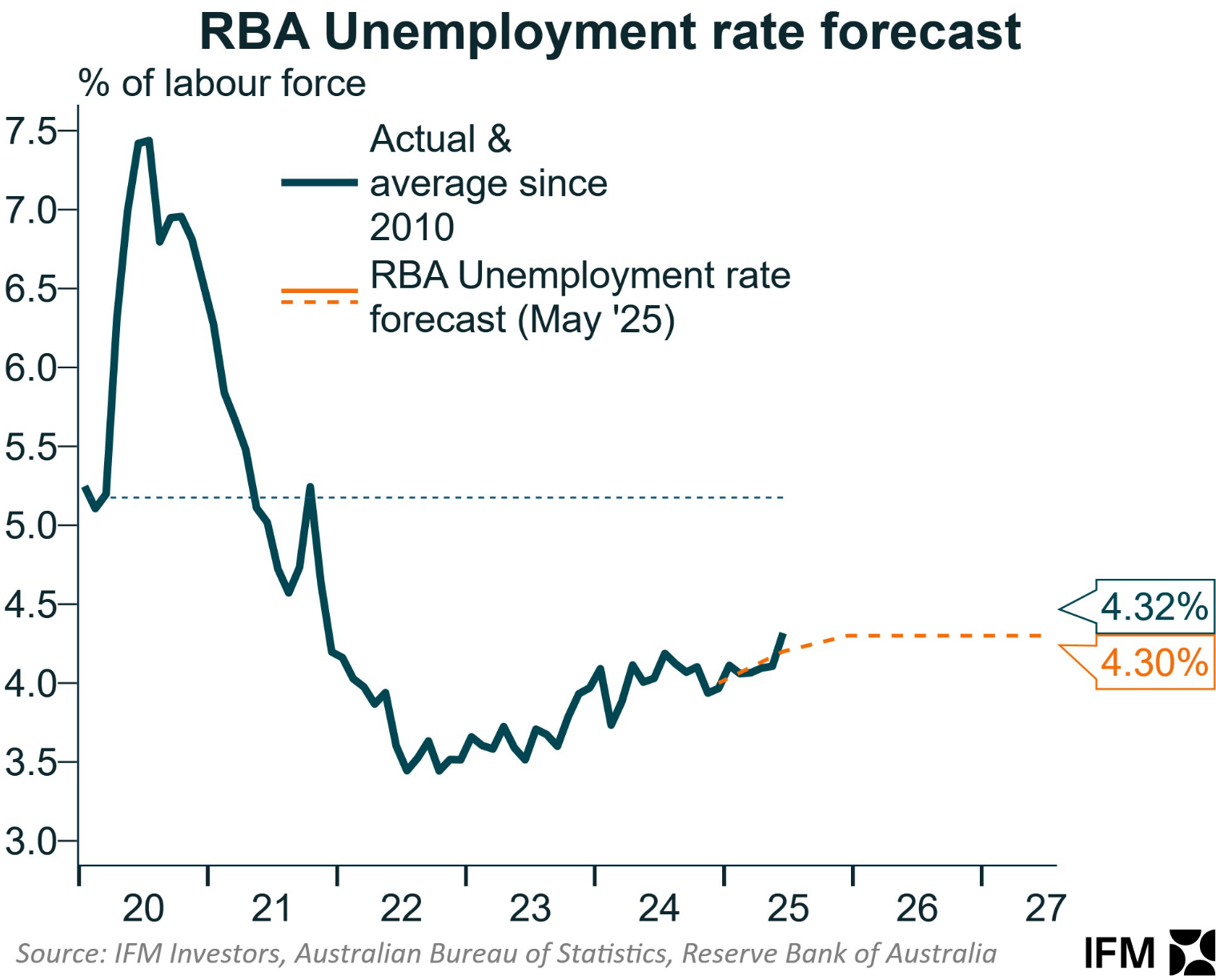

Last week, we received the June labour force data from the Australian Bureau of Statistics (ABS), which suggested that the labour market is deteriorating faster than the RBA’s forecasts.

In particular, the unemployment rate of 4.31% in June was above the RBA’s peak for the cycle.

Given that this was one of the key pieces of data that the RBA was awaiting, it strongly raises the probability of a rate cut at its August meeting.

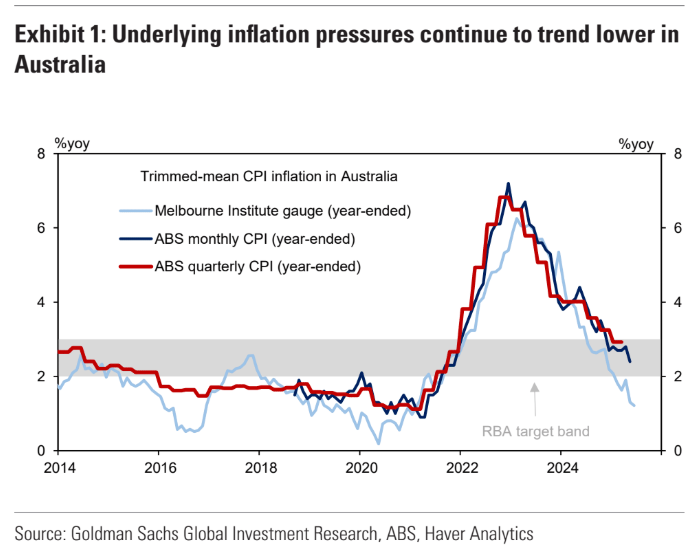

The one thing that could prevent a rate cut is if the Q2 2025 CPI inflation print comes in much stronger than expected. This seems highly unlikely given the various leading monthly indicators of underlying inflation trended lower in Q2.

Financial markets have placed a high probability on a 25 bp rate cut and expect two additional rate cuts over the next 12 months.

Lock it in, I say.