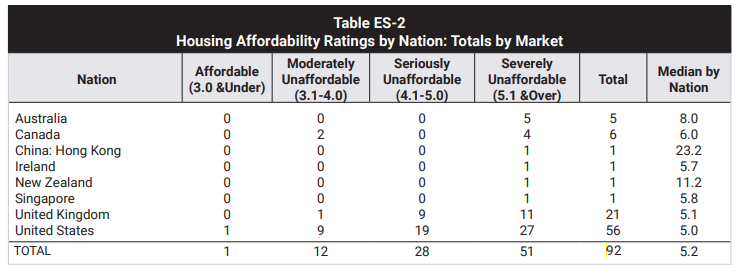

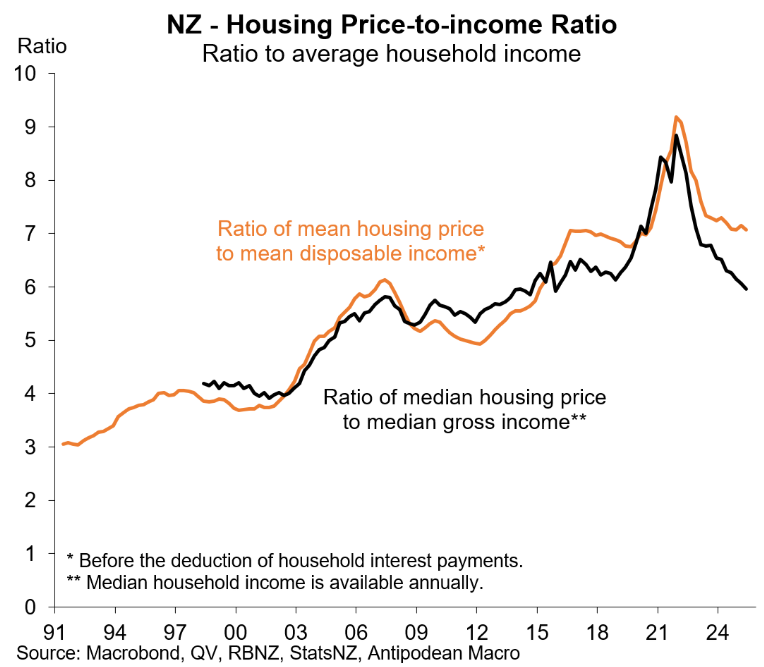

During the Covid-19 pandemic, New Zealand experienced one of the world’s largest house price booms, which pushed median home values to a record 11.2 times median household incomes, according to Demographia.

Source: 2022 Demographia Housing Affordability Survey

Since then, New Zealand has experienced one of the world’s biggest housing crashes, which has significantly improved the nation’s housing affordability.

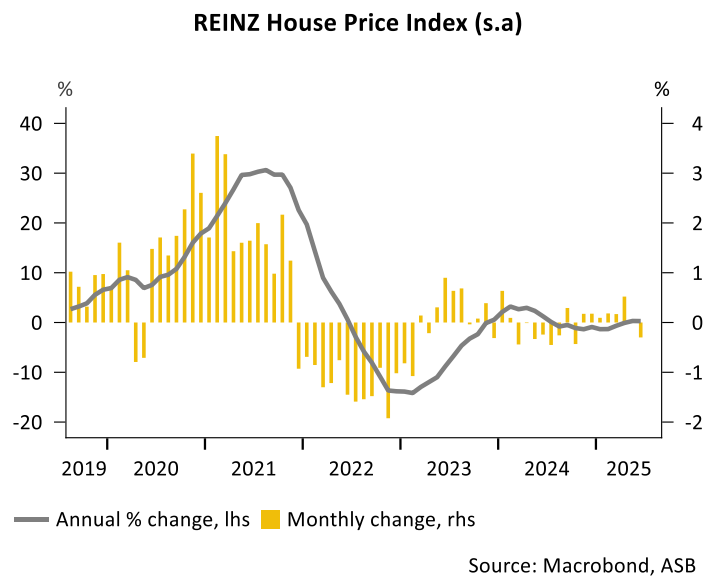

On Tuesday, the Real Estate Institute of New Zealand (REINZ) released its house price index for June, which declined by 0.3% in June:

Home sales turnover has also continued to fall, dropping 4.8% in June (seasonally adjusted), following an upwardly revised 0.8% fall in May.

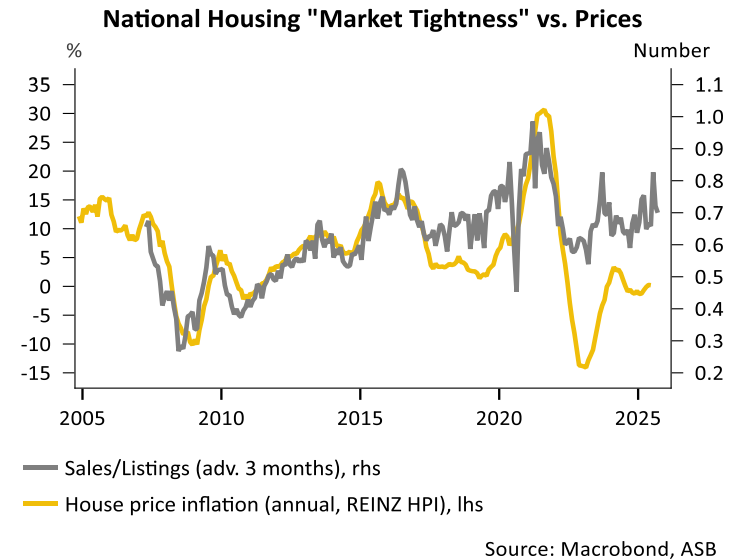

“Overall, these indicators suggest the housing market has shown little movement despite a sizeable reduction in mortgage interest rates”, major bank ASB said.

“The decade-high inventory and no signs of significant cooling in new listings have been widely identified as major factors dampening the recovery of house prices to date. Current inventory is now sitting at 32.7k (seasonally adjusted), about 1.8 times higher than during the last house price boom in November 2021”.

“Our preferred “market tightness” indicator (as shown in the chart below) continued to ease further in the last two months, indicating that house sales turnover has failed to keep up with the increase in new listings, further widening the imbalance between supply and demand”.

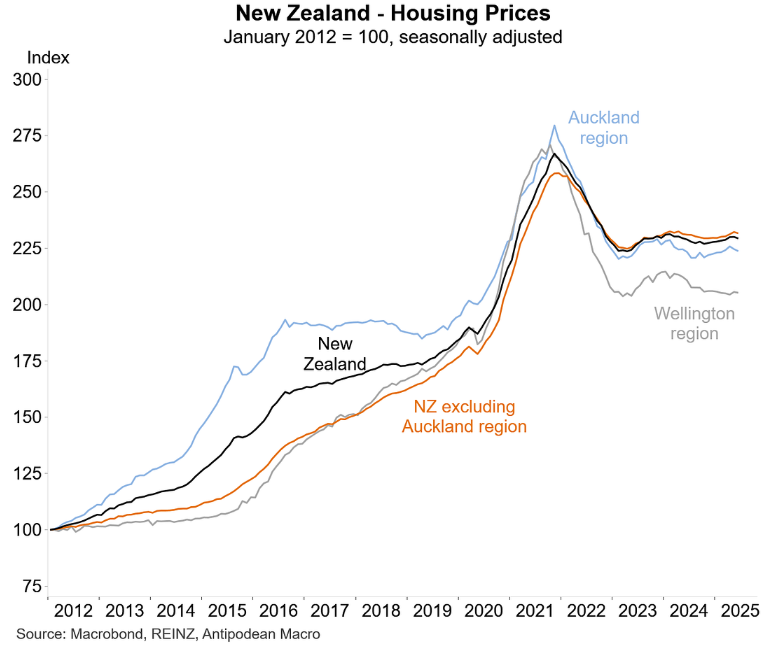

The following chart from Justin Fabo from Antipodean Macro shows that prices have crashed across all major markets in New Zealand.

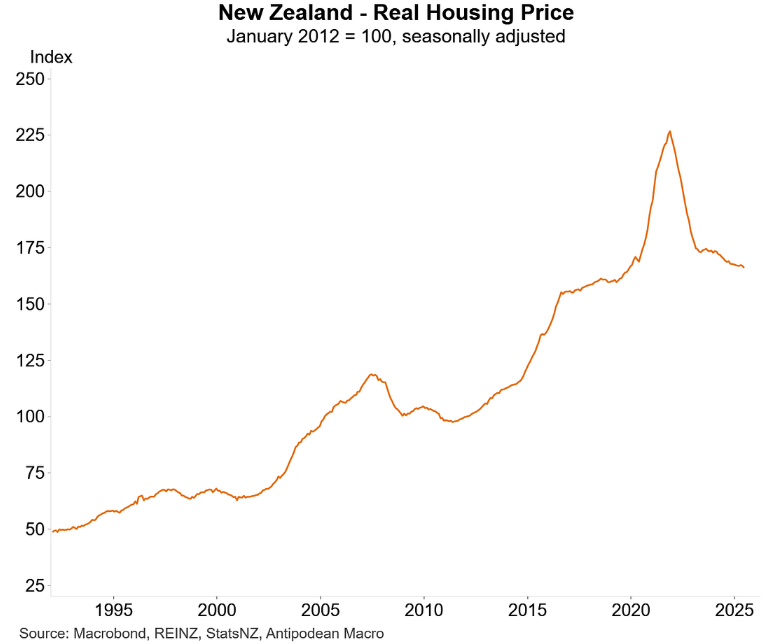

When adjusted for inflation, real house prices have collapsed to pre-pandemic levels:

The ratio of dwelling prices to income in New Zealand has also returned to pre-pandemic levels:

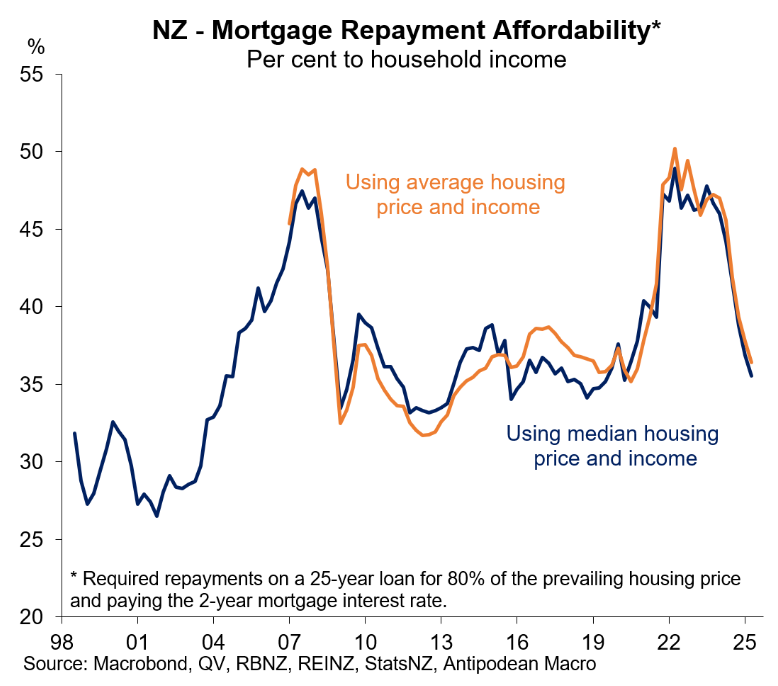

Mortgage repayment affordability has also improved materially, reflecting lower home prices and mortgage rates:

Thus, the sharp decline in prices has dramatically improved housing affordability in New Zealand.

This is in stark contrast to Australia, where politicians have actively stimulated home prices through demand-side stimulatory policies such as the Albanese government’s 5% deposit scheme for first-time home buyers, the expansion of the Help-to-Buy shared equity scheme, changes to lending rules that prohibit banks from including student debts in loan serviceability assessments, and various state government policies.

Australia has actively added demand-side fuel to the housing bonfire, whereas New Zealand has not.