While north Atlantic share markets remain buoyant due to solid earnings on Wall Street and the implied stability of the new US/EU trade deal “framework”, Asian share markets are weaker nearly across the board as peripheral nations – including India and Brazil – await the self imposed tariff deadline tomorrow set by the Trump regime. The USD is holding on to against the majors after the Federal Reserve held interest rates overnight although the Australian dollar is trying to get back above the 65 cent level with a solid retail sales print today.

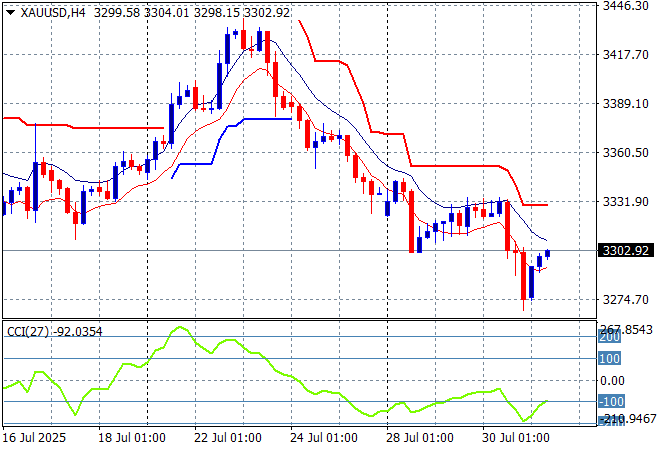

Oil markets are holding on to their recent breakout with Brent crude still above the $72USD per barrel level while gold is trying to get back on track after being pushed below the $3300USD per ounce level but is struggling:

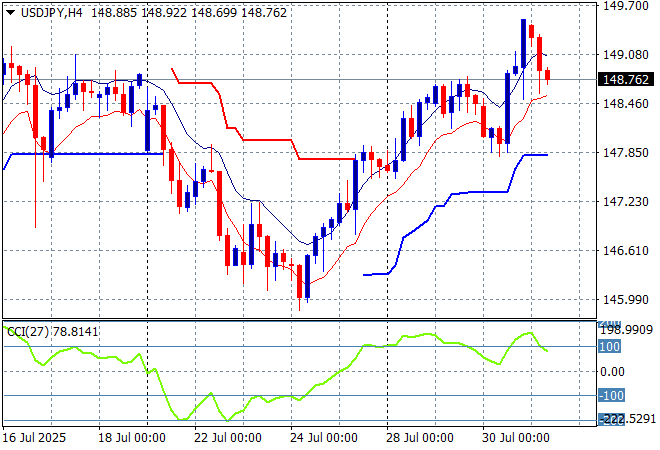

Mainland Chinese share markets are down sharply going into the close with the Shanghai Composite losing more than 1.3% to retrace back below the 3600 point level while the Hang Seng Index has lost a similar amount to retreat below the 25000 point level. Japanese stock markets are the odd ones out with the Nikkei 225 pushed more than 1% higher as it closes at 41100 points while the the USDPY pair has pulled back after getting way ahead of itself overnight to retrace just below the 149 level:

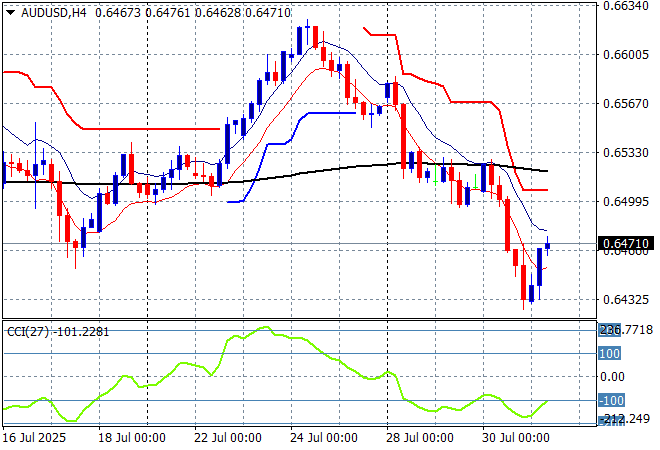

Australian stocks were unable to climb due to domestic releases with the ASX200 closing nearly 0.2% lower to remain above the 8700 point level while the Australian dollar is trying to get back to the 65 cent level against USD after the Fed held fire recently:

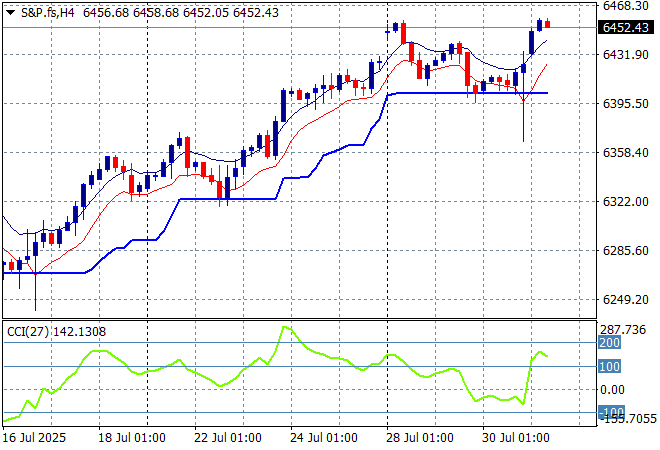

S&P and Eurostoxx futures are up slightly going into the London session with the S&P500 four hourly chart showing the market still wanting to make more new record highs despite being considerably overbought:

The economic calendar includes the German inflation and EU wide unemployment prints then the latest US PCE release.