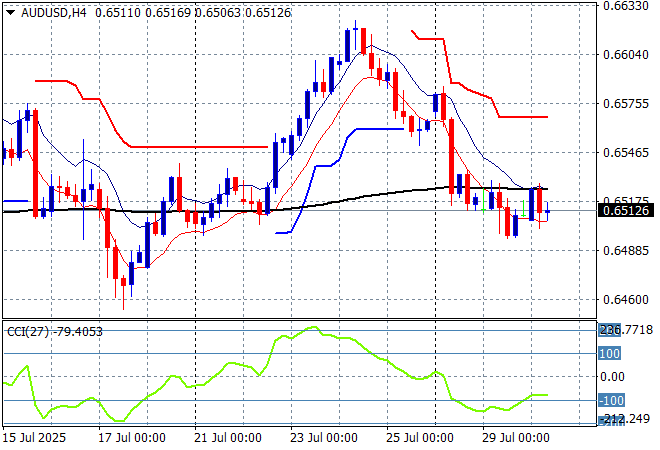

Asian share markets are generally weaker across the board as risk markets try to absorb the impact of the latest trade “deal” from the Trump regime while also anticipating some pretty big macro and economic releases in the coming session. Wall Street is the only light of hope for the bubble boys although we have the FOMC meeting and NFP print looming. Meanwhile the USD is holding on to against the majors as the Australian dollar maintains weakness at just above the 65 cent level despite the soft CPI print today.

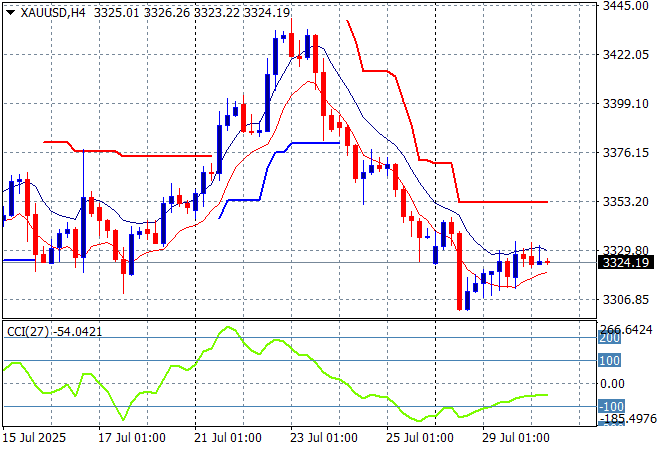

Oil markets are holding on to their overnight breakout with Brent crude now above the $71USD per barrel level while gold is trying to get back on track after almost pushed below the $3300USD per ounce level but remains flat:

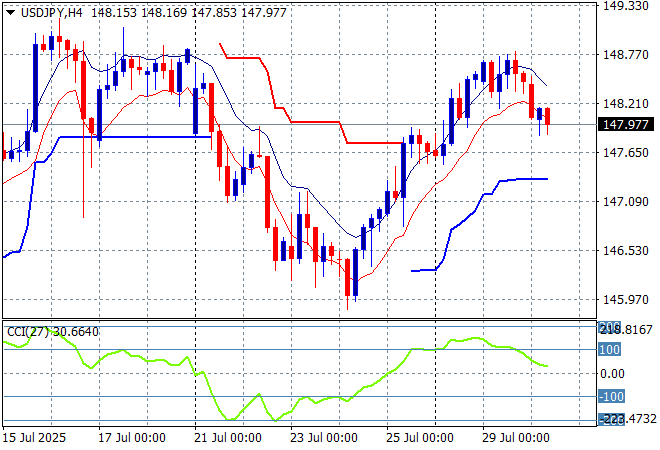

Mainland Chinese share markets are up slightly going into the close with the Shanghai Composite just above the 3600 point level while the Hang Seng Index has lost more than 1% to retreat to just above the 25000 point level. Japanese stock markets remain in the doldrums with the Nikkei 225 pushed 0.2% lower as it falls back below the 41000 point level while the USDPY pair has rolled over after its recent uptrend to retrace below the 148 level:

Australian stocks were the best performing in the region with the ASX200 closing nearly 0.6% higher to extend above the 8700 point level while the Australian dollar is barely holding on to the 65 cent level against USD in the wake of the CPI print:

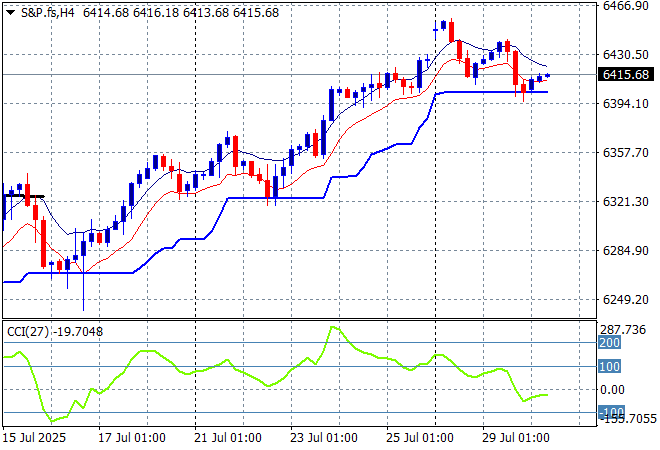

S&P and Eurostoxx futures are up slightly going into the London session with the S&P500 four hourly chart showing the market still wanting to make more new record highs despite being overbought:

The economic calendar includes the latest US private jobs data then the Bank of Canada interest rate meeting.