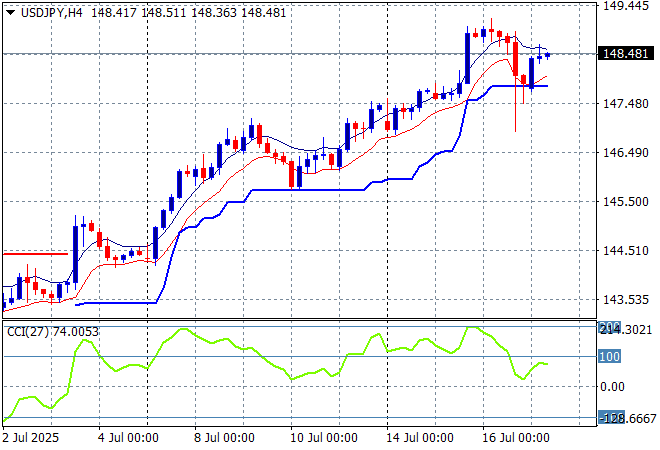

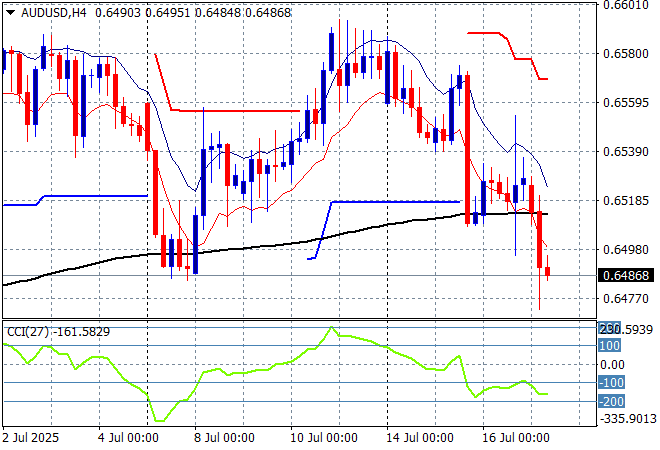

Currency markets pivoted to Asian releases today with the jump in local unemployment and a fall in Japanese exports hitting both the Australian dollar and Yen respectively. The Trump regime’s trade war is continues with “framework deals” for India and Europe the next hand-waving “framework” that is being floated while actual free trade deals outside the US are being done. Last night’s slightly soft US PPI was overshadowed by the sword over Fed Chair Powell that eventually saw Wall Street recover but tonight’s initial jobless claims may upset risk again.

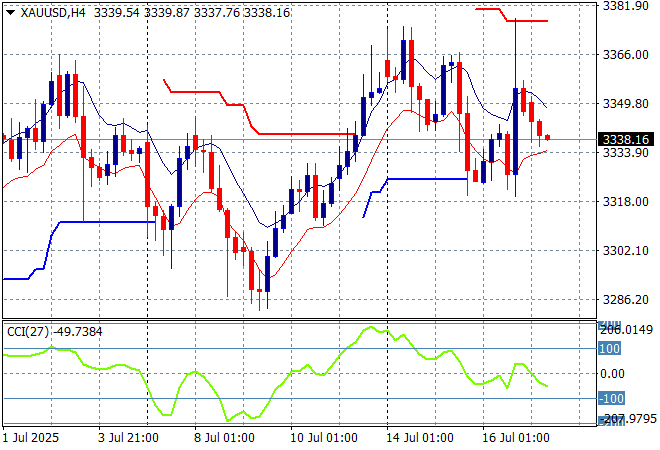

Oil markets are drifting slightly lower with Brent crude still trading below the $69USD per barrel level while gold is pulling back again after failing to make a comeback as it sits just above the $3300USD per ounce level:

Mainland Chinese share markets are steady with the Shanghai Composite just above the 3500 point level going into the afternoon session while the Hang Seng is lifting slightly to stay just above the 24000 point level. Meanwhile Japanese stock markets are up higher despite the poor export figures with the Nikkei 225 up 0.3% to just below the 40000 point barrier as the USDPY pair holds at the mid 148 level:

Australian stocks are really happy about the chance of a rate cut from the RBA given the poor employment print with the ASX200 up nearly 0.9% to get back above the 8600 point level while the Australian dollar is at a two week low as it cracked below the 65 cent level against USD:

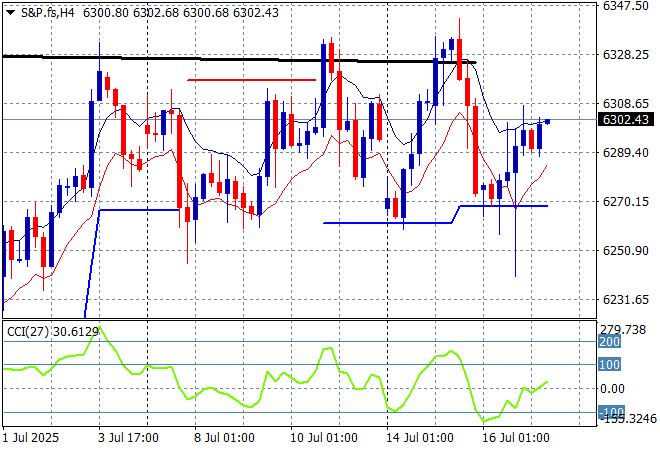

S&P and Eurostoxx futures are up slightly going into the London session with the S&P500 daily chart showing the market coming back from it recent record high but lacking confidence under the 6300 point level:

The economic calendar ramps up with the latest UK unemployment figures, then US retails sales and initial jobless claims.