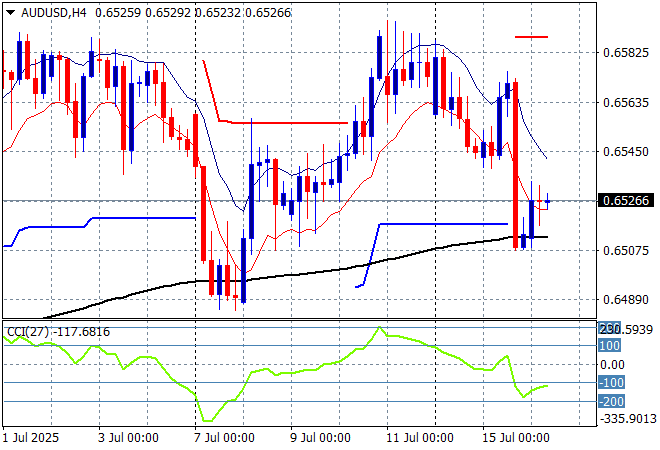

Risk markets continue to weigh up last night’s US CPI print with tariff inflation beginning to hit the US domestic economy, with the Fed likely to hold instead of cut for the rest of the year. More “frameworks” and “thinkings about deals, maybe” are being announced by the Trump regime as US Treasury yields drift higher, with tonight’s PPI print the one to watch for on the calendar. Meanwhile the Australian dollar is trying to clawback its overnight losses as it steadies just above the 65 cent level.

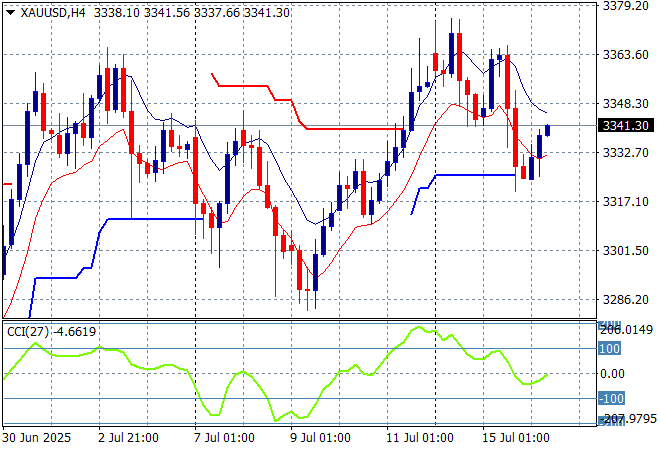

Oil markets are drifting slightly lower with Brent crude trading below the $69USD per barrel level while gold is trying to make a comeback after retreating just below the $3300USD per ounce level last week:

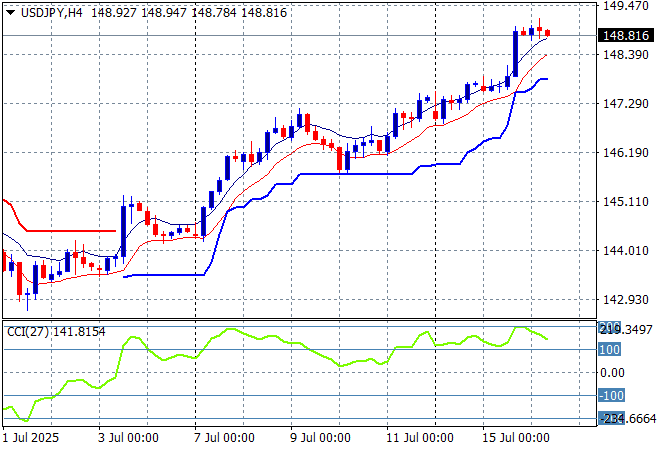

Mainland Chinese share markets are steady with the Shanghai Composite just above the 3500 point level going into the afternoon session while the Hang Seng is also treading water to stay just above the 24000 point level. Meanwhile Japanese stock markets are not moving around much as well with all eyes on the bond market with the Nikkei 225 unchanged just below the 40000 point barrier as the USDPY pair holds fire just below the 149 level:

Australian stocks were the worst in the region with the ASX200 down nearly 0.8% to get back below the 8600 point level while the Australian dollar is holding steady above the 65 cent level against USD after last night’s CPI induced rollover:

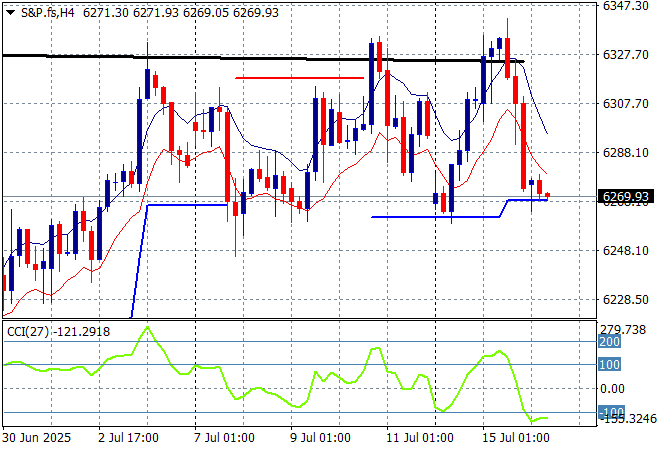

S&P and Eurostoxx futures are down slightly going into the London session with the S&P500 daily chart showing the market coming back from it recent record high but lacking confidence under the 6300 point level:

The economic calendar will shift its focus to the US PPI print and latest industrial production figures tonight.