Most Asian share markets are lifting higher despite a very weak lead from Wall Street, while local stocks are taking a double whammy due to the expected rate cut from the RBA turning into a hold and then the Trump regime’s bullying tariffs on pharmaceuticals. There’s more tariff announcements and letter printing on the way, plus the huuge copper tariffs, but of course we await the TACO trade. The RBNZ announced a hold today as well while the latest Chinese inflation data is being absorbed well by onshore share markets.

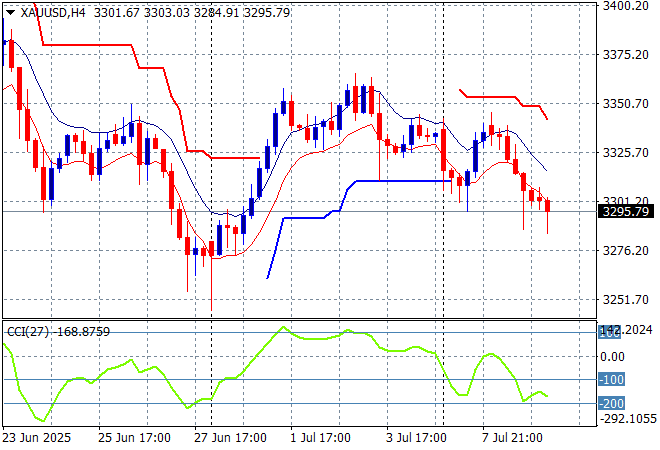

Oil markets are stabilising following the bigger than expected OPEC+ production increases and surprise private US oil data with Brent crude trading just above the $70USD per barrel level while gold is failing to make a comeback as it retreats just below the $3300USD per ounce level:

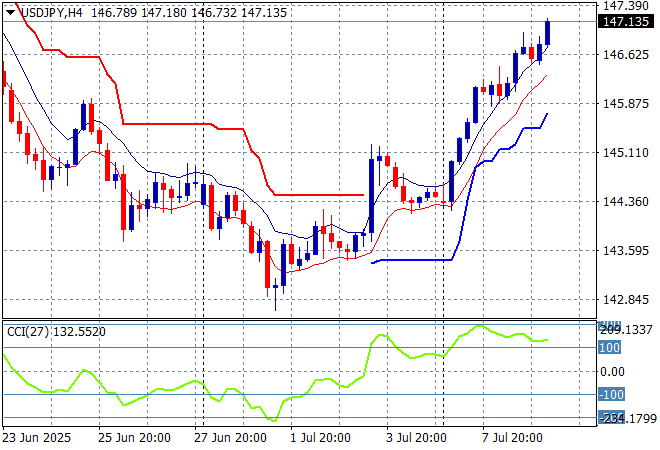

Mainland Chinese share markets are up slightly with the Shanghai Composite pushing above the 3500 point level while the Hang Seng is taking back its recent gains to just slip back below the 24000 point level. Meanwhile Japanese stock markets are somewhat positive although the Nikkei 225 remains below the 40000 point barrier with the USDPY pair finding further strength to push above the 147 level despite the lack of any progress on trade talks with the US:

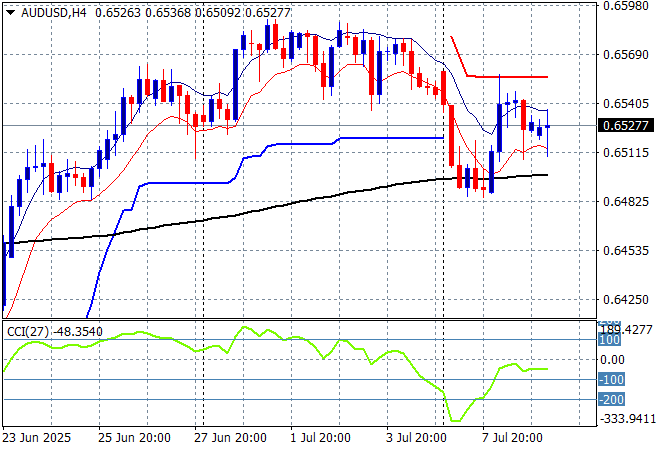

Australian stocks are the odd ones out due to Bully Boy Trump threatening the pharmaceutical industry with more tariffs with the ASX200 slipping more than 0.4% lower while the Australian dollar has held on above the 65 cent level against USD following the surprise hold decision by the RBA:

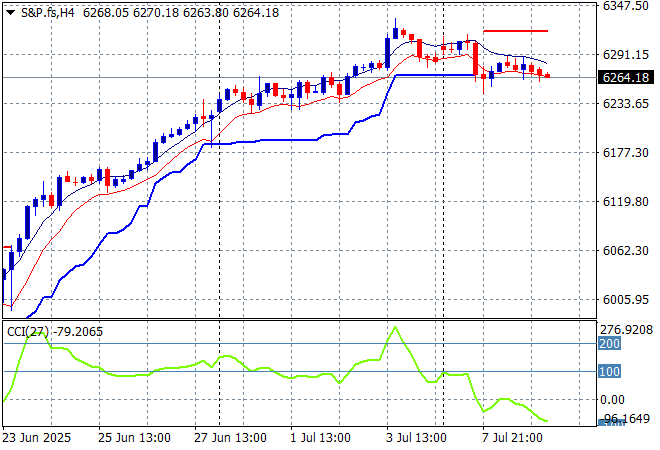

S&P and Eurostoxx futures are down slightly going into the London session with the S&P500 daily chart showing the market clearly overextended but now rolling over after breaching the 6300 point level:

The economic calendar is relatively quiet tonight with the release of the official US oil data, some Treasury auctions then the release of the latest FOMC minutes.