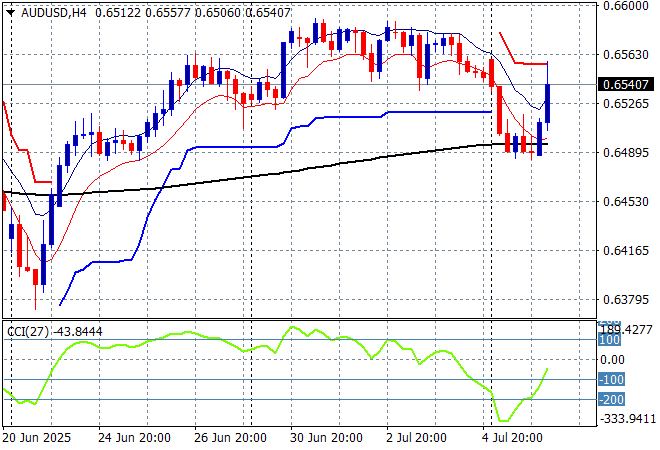

The big surprise in the newsflow is not the Epstein list no longer exists its that the RBA actually held interest rates steady in today’s meeting, launching the Australian dollar higher. The RBA is highlighting the uncertainty of the Trump regime’s tariff tirade as one reason but also domestic concerns play a big point. The TACO in chief is pushing the “deadline” around like a cold hamburger on his plate with the August 1st date no longer a certainty nor are the letter demands sent out earlier in the week.

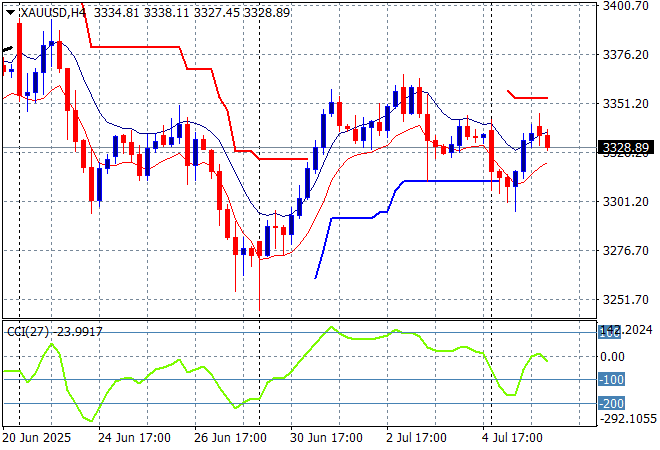

Oil markets are stabilising following the bigger than expected OPEC+ production increases with Brent crude trading just above the $69USD per barrel level while gold is failing to make a comeback as it sits just below the $3300USD per ounce level:

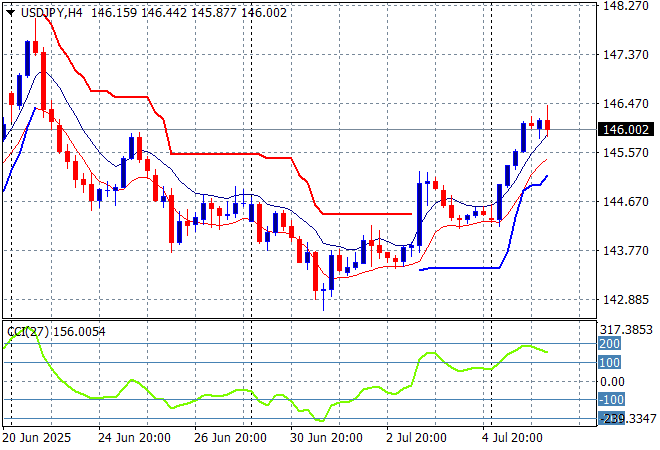

Mainland Chinese share markets are up slightly with the Shanghai Composite pushing 0.4% higher to extend well above the 3400 point level while the Hang Seng is pushing more than 0.8% higher to get back above the 24000 point level. Meanwhile Japanese stock markets are also somewhat positive although the Nikkei 225 remains below the 40000 point barrier with the USDPY pair finding some strength to settle at the 146 level despite the lack of any progress on trade talks with the US:

Australian stocks were doing well but have lost their gains on the RBA hike as the ASX200 slips more than 0.2% lower while the Australian dollar has spiked back above the 65 cent level against USD on the surprise hold decision by the boffins at Martin Place, although this looks like a one off amid the tariff threat:

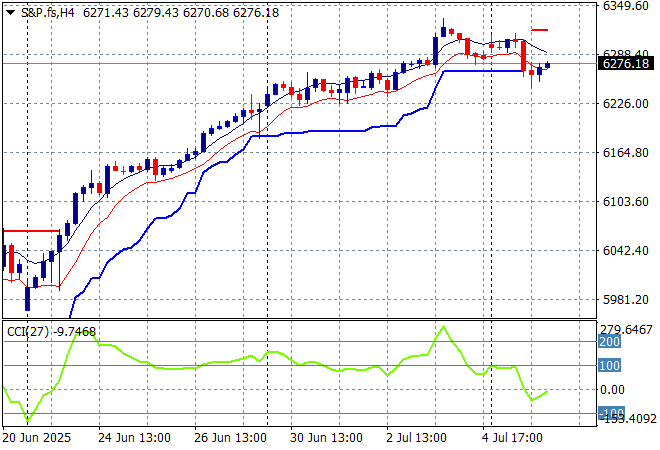

S&P and Eurostoxx futures are up slightly going into the London session with the S&P500 daily chart showing the market clearly overextended but still turning any news into positive returns after breaking right through the 6300 point level:

The economic calendar is relatively quiet tonight with German balance of trade and US Treasury auctions.