The Reserve Bank of New Zealand released CPI inflation data today, which showed that New Zealand inflation lifted further in Q2 to 2.7%.

Major bank ASB noted that while the result wasn’t a surprise, “it is an unwelcome development after NZ endured years of high interest rates to tame rampant inflation”.

“The last thing New Zealanders (and the RBNZ) need right now is the prospect of inflation re-invigorating and crimping the extent to which the RBNZ can cut interest rates and stimulate the fledgling economic recovery”.

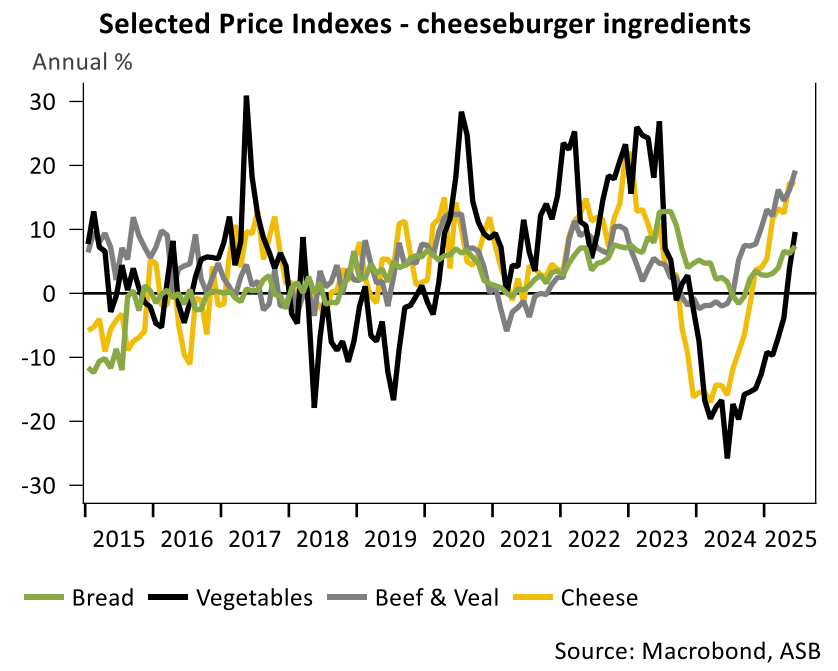

As illustrated below by ASB, rising food costs were partly responsible for the lift in CPI.

“Every major burger ingredient has shot up in price (the inclusion of vegetables in the ingredients list is slightly aspirational). The reasons for the price increases are varied and follow a period when food prices were falling back after their post-COVID jump”, ASB noted.

Household energy costs have also “risen sharply, in part through higher transmission line charges”, whereas “construction costs dropped over the quarter and fuel prices eased back further”.

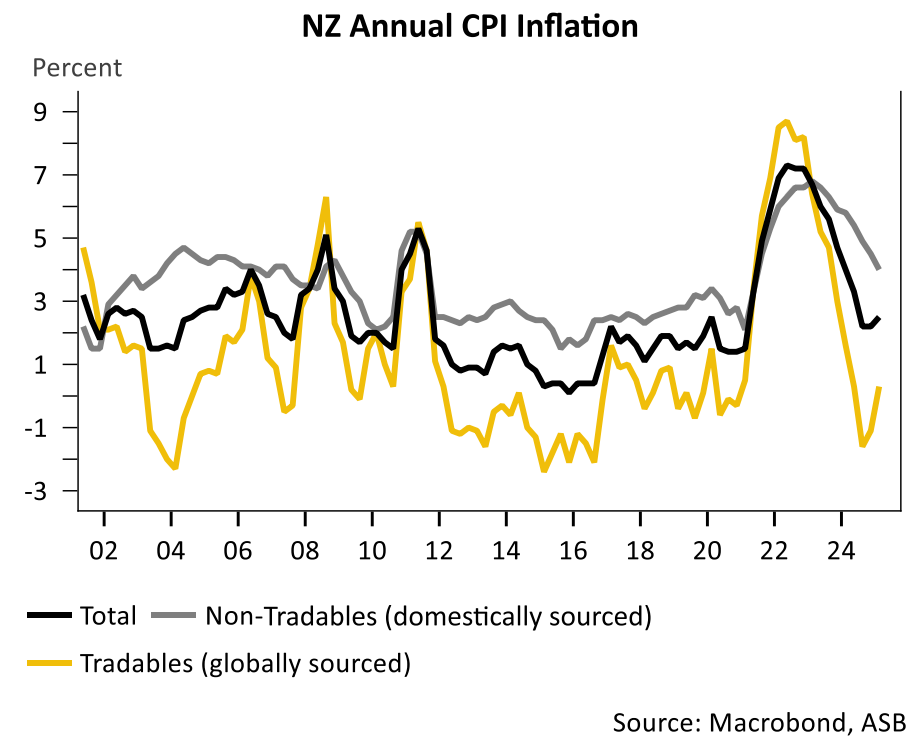

More broadly, “tradable inflation has rebounded into positive territory after a period of falling prices that did much to drag overall inflation down from its 7+% peak”.

“The return to a more normal pace of modest but positive tradable price inflation means still-high non-tradable inflation is no longer being offset”, ASB wrote.

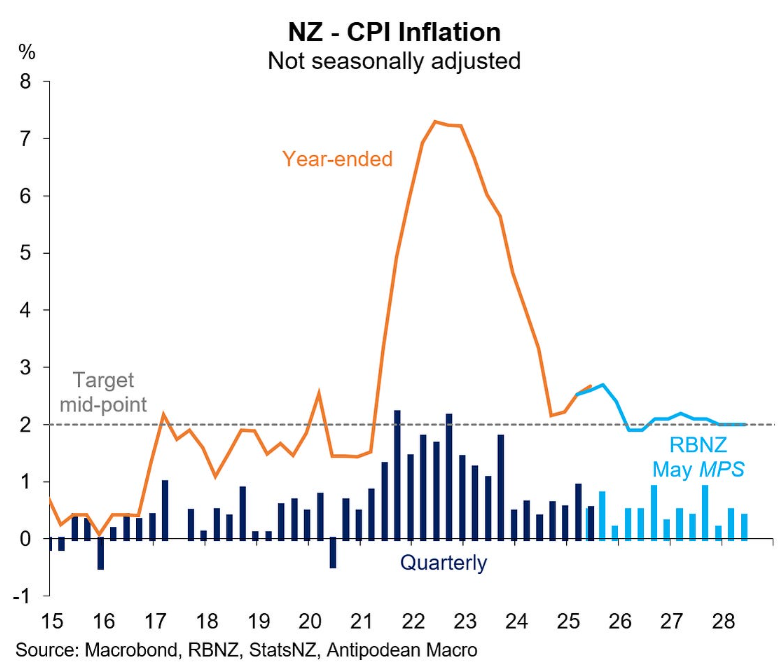

Justin Fabo from Antipodean Macro created the following chart showing that CPI inflation is already at the peak the Reserve Bank had forecast in its May monetary policy statement.

Therefore, the Reserve Bank’s decision to hold the official cash rate earlier this month seems justified, despite the weakening economic conditions.

ASB still expects the Reserve Bank to cut the official cash rate in August by 25 bp, owing to the weak economy and growing spare capacity.

That said, the official cash rate outlook remains “in a push-me pull-me state: risks of spillover from the current inflation spike against the risk of weaker inflation pressures from any short-term stalling in economic recovery or tariff impacts”.