Australia’s superannuation concessions require reform to make them fairer and more sustainable.

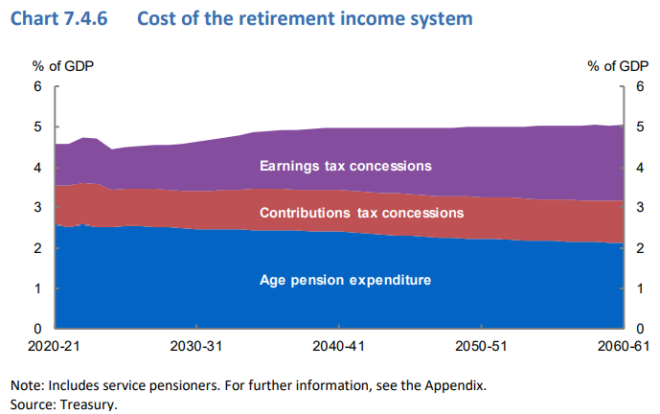

The Australian Treasury estimates that superannuation concessions will cost the federal budget approximately $60 billion in lost revenue in 2024–25, and this cost is expected to increase significantly.

In FY25, concessions on superannuation contributions were estimated to be $30,950 million. By FY28, that number is projected to grow to $36,750 million.

In FY25, concessions on superannuation earnings were estimated at $24,200 million. By FY28, they are projected to grow to $28,250 million.

Logically, any reform to superannuation concessions should focus on these two areas.

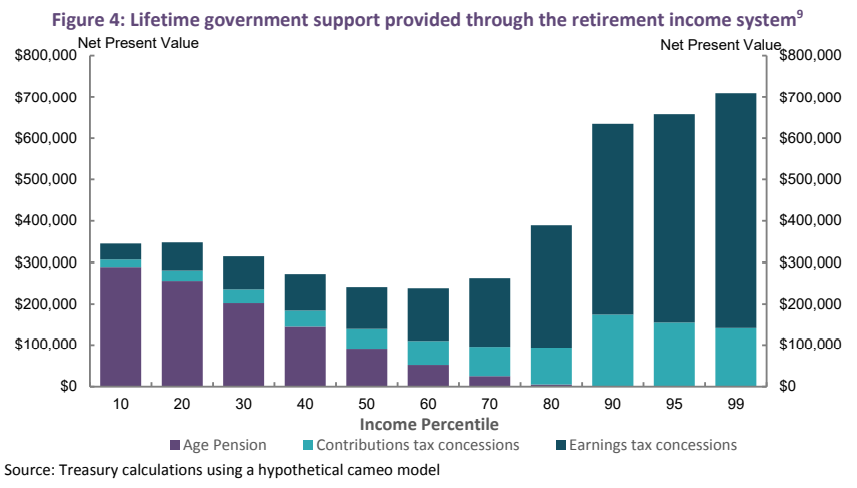

As illustrated below by the Australian Treasury, these two superannuation concessions flow overwhelmingly to people with higher incomes:

The Australian Treasury also estimates that superannuation concessions will eventually cost more than the aged pension.

The Albanese government has said that it will raise the income tax on super balances of $3 million or more from 15% to 30%. It would also begin taxing “paper gains” that haven’t been realised at a rate of 30%. These thresholds would not be adjusted for inflation or wage growth.

The Coalition, most teal independents, business leaders, the superannuation industry, renowned economists like Ken Henry (the main author of the 2010 Henry Tax Review) and Phil Lowe (the former governor of the Reserve Bank of Australia), and even Bill Kelty, the former secretary of the ACTU and one of the people who helped create Australia’s compulsory super system, are against taxing unrealised gains.

Last week, I proposed three alternatives for taxing unrealised super gains, which I argued would be simpler, more efficient, and more equitable.

Option 1: Lower the threshold to $2 million and only tax realised gains at 30%.

I propose that the government should lower the $2 million threshold for large superannuation accounts, tie it to salary growth, and raise the tax rate on actual (realised) profits from 15% to 30%.

The second 15% of tax would be set in the same way as the first, which would make the reform easy to implement. It would also make superannuation tax breaks fairer and bring in billions of dollars of additional budget revenue.

Option 2: Tax 15% of earnings made during retirement:

People over 60 who have less than $2 million in retirement accounts currently don’t have to pay taxes on their earnings, whereas Australian workers have to pay full marginal tax rates.

Last month, John Kehoe of The AFR said, “This is arguably more scandalous than the 15% rate faced by super savers with more than $3 million, who are at least contributing some tax and Chalmers wants to tax more, including on unrealised capital gains”

The standard 15% superannuation tax should be extended to realised earnings on superannuation accounts in the retirement phase.

This would make superannuation concessions fairer and more consistent and also raise additional budget revenue.

Option 3: Instead of a 15% flat tax on superannuation contributions, make it a 15% deduction:

The government should replace the 15% flat tax with a 15% deduction from one’s marginal tax rate.

This small change would make superannuation concessions on contributions progressive.

If a superannuant made $220,000, they would pay 32% in taxes on their superannuation contributions, which is 15% less than their marginal tax rate of 47%.

If a superannuant making $30,000 contributed, they would only have to pay 3% in taxes on their contribution because their marginal tax rate is 18% minus 15%.

Last week, Wilson Asset Management lodged its submission to the Economic Reform Roundtable, whereby it outlined “a logical approach to superannuation tax reform that is budget positive, supports long-term investment, and avoids the taxing of unrealised gains”.

Wilson’s proposal introduces a Progressive Super Surcharge, which is an additional tax applied only to realised gains on superannuation balances above $3 million, namely:

- Balances of $3 million – $6 million: an additional 15% tax on realised gains;

- Balances of $6 million – $10 million: an additional 17.5% tax on realised gains;

- Balances of $10 million – $20 million: an additional 20% tax on realised gains; and

- Balances more than $20 million: an additional 25% tax on realised gains.

Personally, I believe this is a sound proposal, although the progressive tax rates should kick in at balances above $2 million, indexed to inflation or wage growth.

Regardless, the types of proposals outlined above are far superior to taxing unrealised gains and would improve the equity and sustainability of the system.