Cotality’s latest Housing Chart Pack valued Australia’s total residential housing stock at $11.5 trillion as of June 2025, comprising 11.3 million dwellings.

This means that the average value of an Australian home was $1,018,000 in June 2025, a remarkable figure that ranks Australian housing among the most expensive in the world.

Aussie YouTuber Biko Konstantinos posted the following chart on Twitter (X) showing the divergence between home prices and household incomes in the United States:

Konstantinos asked followers whether a similar chart existed for Australia.

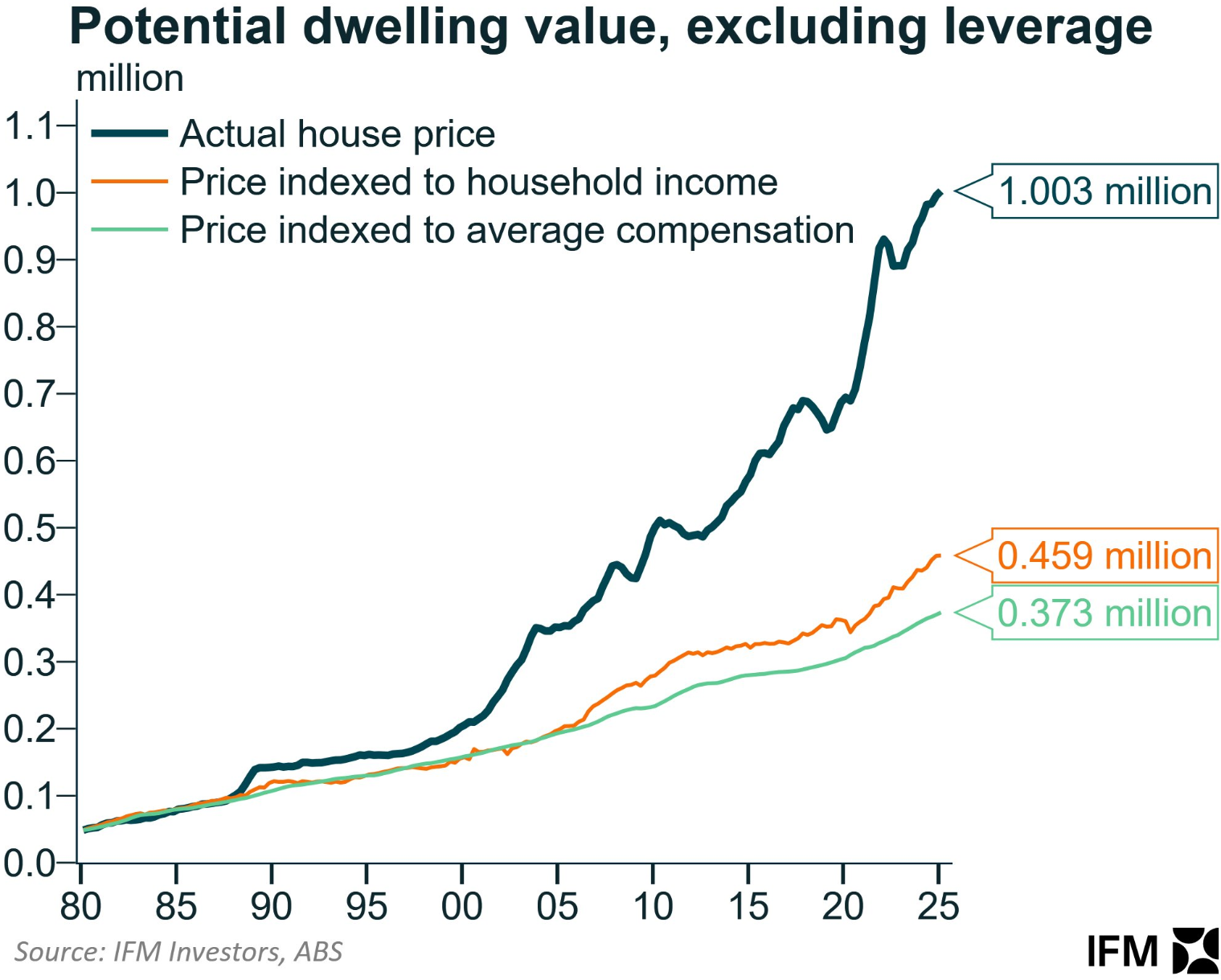

Alex Joiner, chief economist at IFM Investors, obliged with the following chart for Australia:

Joiner shows that if home prices were linked to household income growth, the median house price in Australia would currently be around $460,000, rather than $1 million.

“It was a poor situation leading into COVID, and then house prices rose sharply due to zero interest rates through that period”, Joiner explained via Twitter (X).

“This is one of the seemingly unspoken costs of the pandemic, at least for those who aspire to homeownership. It also makes the point that the household income definition has evolved from a one-income household to two in most cases”.

“It is very well-known, of course, that the median income cannot buy the median house”.

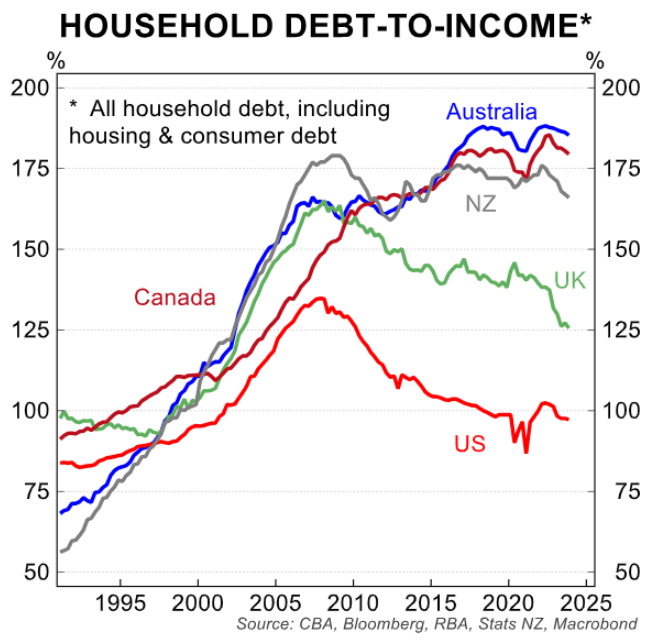

Last year, Alex Joiner published the following chart showing how Australian house prices have been ‘chased upwards’ by rising mortgage sizes.

This expansion of mortgage debt is the primary reason why Australian households are now among the most indebted in the world.

Sadly, the house price and debt situation is set to deteriorate in Australia for multiple reasons.

First, the Reserve Bank of Australia (RBA) is set to cut interest rates, which will increase borrowing capacity and mortgage demand, driving up home prices and debt.

Financial markets are tipping another 75 bp of rate cuts over the coming year, which should stimulate buyer demand.

There have also been a slew of recent policy announcements by state and federal governments aimed at stimulating home prices. These include:

- The Albanese government’s 5% deposit scheme for FHBs (effective 1 January 2026).

- The Albanese government’s exclusion of student debts from loan servability calculations.

- The Albanese government’s expansion of its Help-to-Buy shared equity scheme.

- The Queensland government’s generous shared equity scheme, announced in the latest state budget.

Some lenders have also announced new stimulatory mortgage products, including:

- 40-year mortgage terms.

- 10-year interest-only terms (AMP) without reassessment.

The above drivers will inevitably pour fuel on Australia’s housing bonfire by boosting borrowing capacity, demand, and prices.