Falling housing inflation clears path for RBA

Justin Fabo from Antipodean Macro and Alex Joiner from IFM Investors published superb sets of charts on Wednesday’s Q2 CPI inflation report from the Australian Bureau of Statistics (ABS), which all but guarantees a 25 bp rate cut at next month’s Reserve Bank of Australia (RBA) monetary policy meeting.

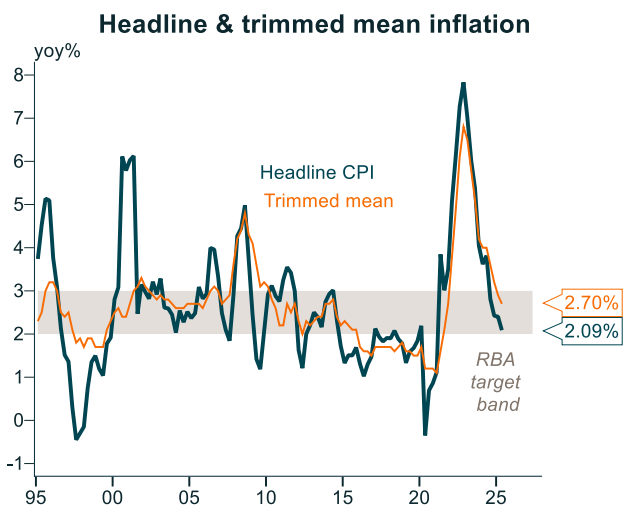

As illustrated below by Alex Joiner, both headline CPI (2.1%) and trimmed mean CPI (2.7%) have fallen within the RBA’s target band of 2% to 3%:

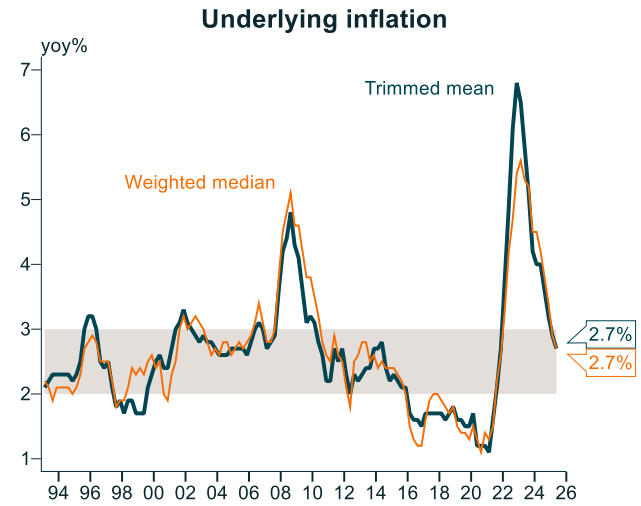

Both measures of underlying inflation—the trimmed mean and weighted median—printed at 2.7%:

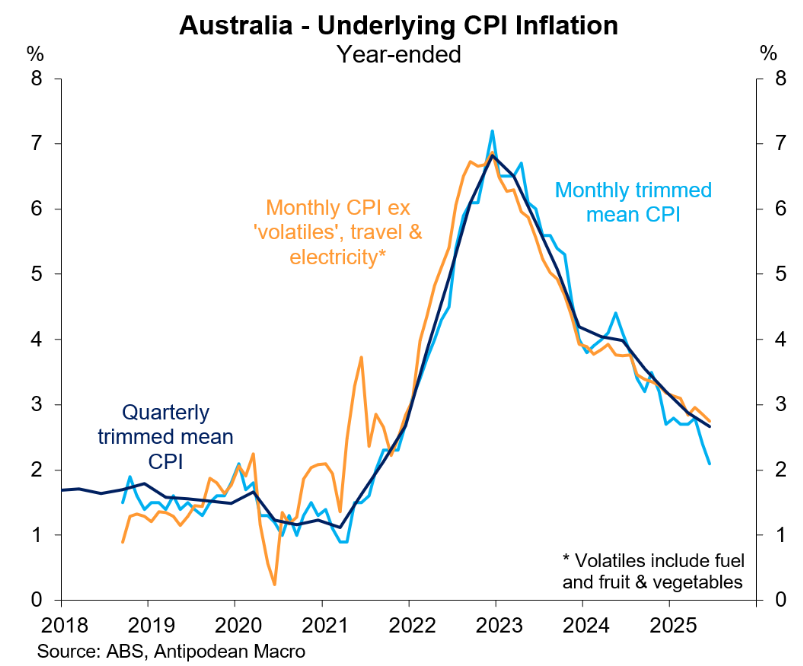

As shown by Justin Fabo, the monthly trimmed mean inflation also fell to just 2.1%:

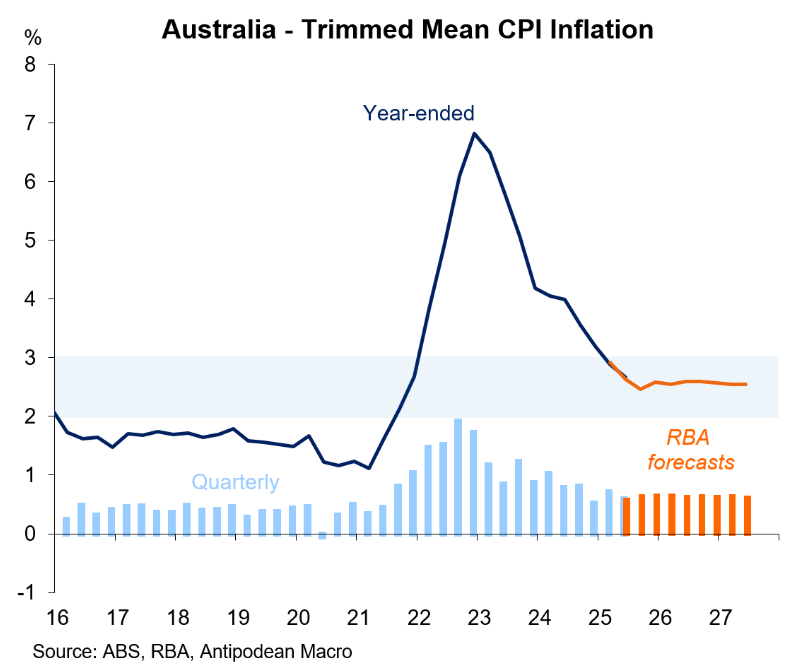

Importantly, the policy-relevant trimmed mean inflation of 2.7% was also tracking in line with the RBA’s forecast:

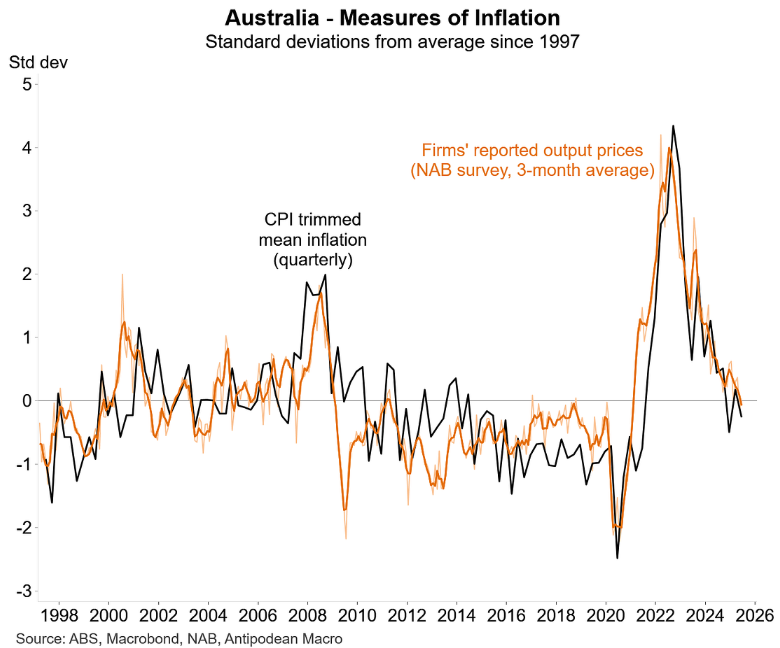

Broader measures of inflation, such as from the NAB business Survey, has also shown disinflation:

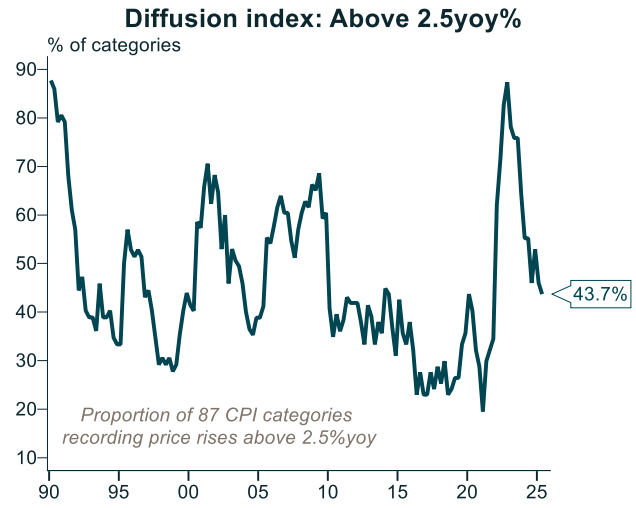

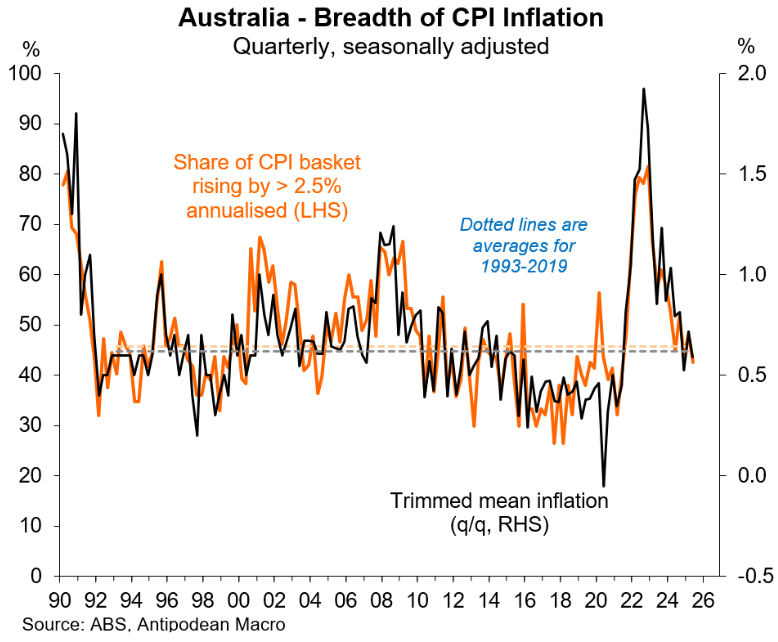

Joiner shows below that the breadth of inflation has also fallen, with around 44% of the 87 CPI categories recording price rises above 2.5%—the midpoint of the RBA’s target range:

Justin Fabo shows below that this was a little below the long-run average:

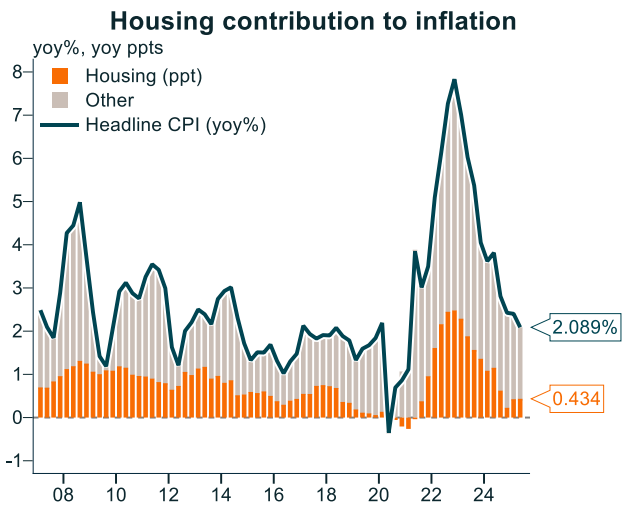

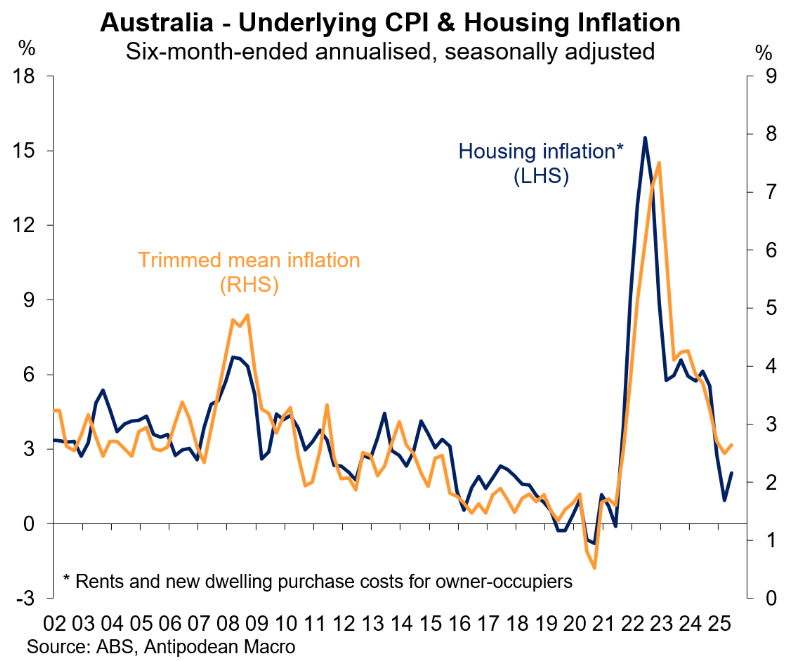

As Alex Joiner shows below, housing—one of the largest components of the CPI (21% weight)—has turned from being a key driver of inflation to a key detractor:

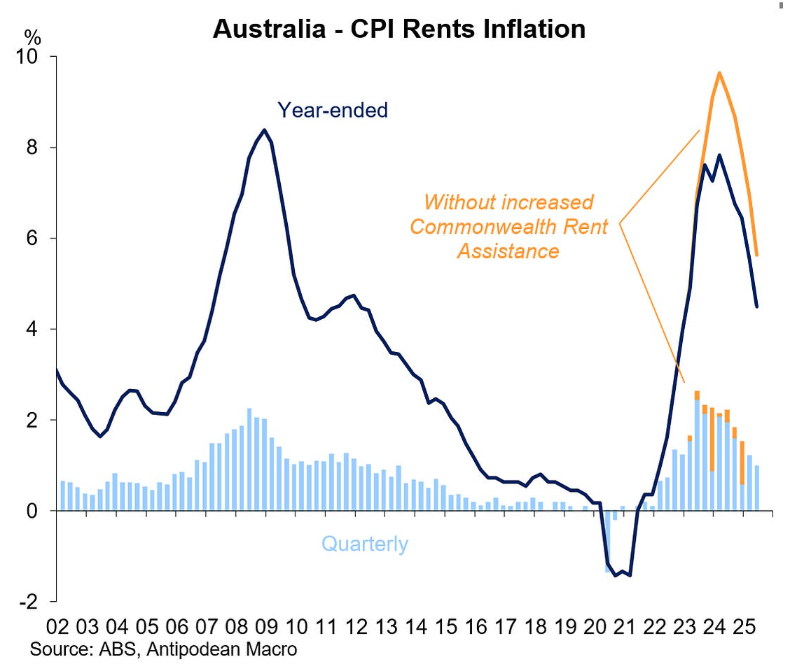

As Justin Fabo illustrates below, rent inflation has fallen significantly, partly due to subsidies:

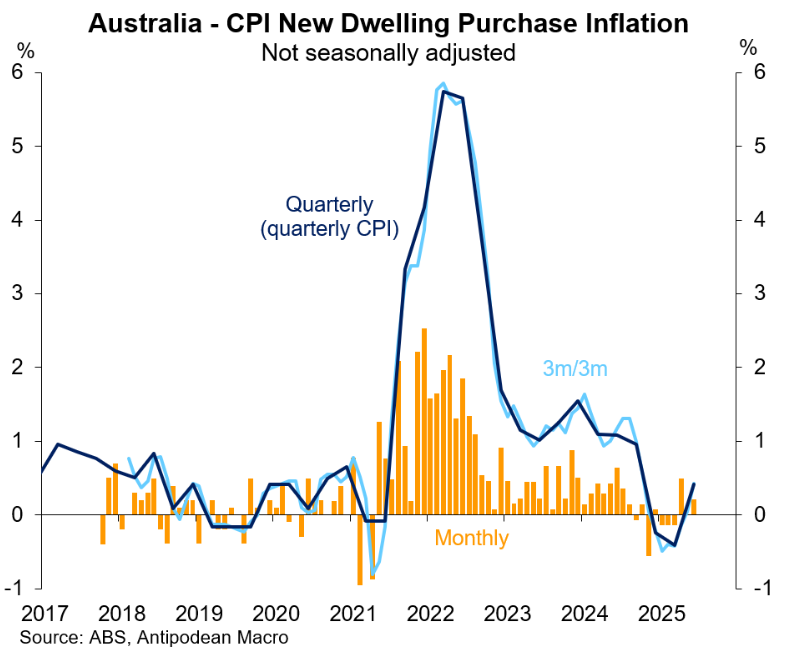

New dwelling prices have also collapsed:

Together, the decline in housing inflation has helped pull trimmed mean inflation lower:

However, Justin Fabo warns that “we might not be able squeeze more out of this source of disinflation”, with housing inflation ticking higher in Q2.

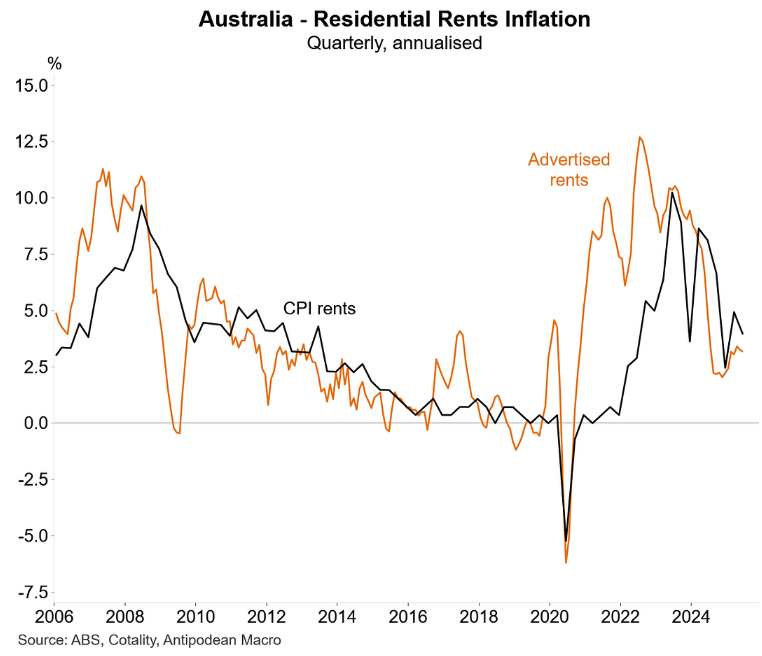

Indeed, Fabo notes that “a lot of the disinflation in CPI rents has already occurred”, with advertised and CPI rents ticking higher recently:

He also warns that “the pick-up in residential building approvals (and new house sales) may suggest that new dwelling purchase inflation will start to pick-up from here”.

Regardless, a 25 bp cut in the official cash rate next month is now a lock. But further rate cuts will depend on how the data evolves.