The federal government’s proposal to tax the unrealised capital gains of superannuation funds was a key focus of the first question time session in the new parliament.

Treasurer Jim Chalmers criticised the Coalition for attacking a policy that he claims would affect about 0.5% of people with a superannuation account, noting that it had opposed a tax cut for 14 million Australians at the recent election.

However, some Labor MPs have expressed reservations about the unrealised capital gains tax (CGT) proposal, but concede that action is needed to boost government revenue.

“I hate the principle of taxing unrealised capital gains”, one senior Labor MP told The Australian. “But there’s a necessity to it, and caucus broadly doesn’t have a problem with what Jim (Chalmers) is doing”.

Another Labor MP noted there was not “unanimous support” in caucus.

Another senior MP said Labor would need to index the threshold in the future to ensure it didn’t impact young people today when they retired. “I do understand the concerns regarding unrealised capital gains. But it’s mostly older people (affected)”, the MP said.

“We need to look at how we support young people. I’m sure it will be indexed in the future”.

The Financial Services Council estimates that without indexation, 500,000 people would end up being caught by the tax.

There is no doubt that Australia’s superannuation concessions should be reformed to make them more equitable and sustainable.

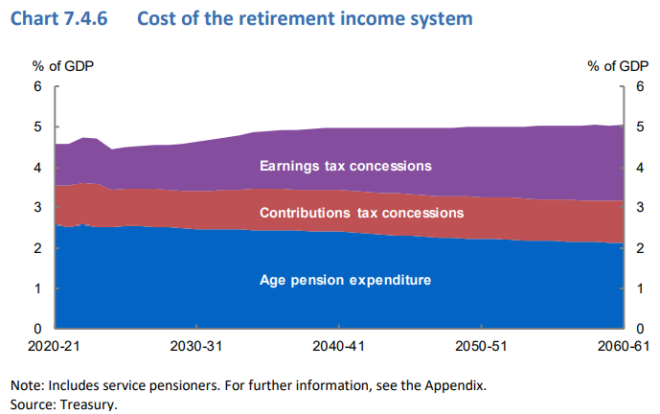

According to the Australian Treasury, superannuation concessions are estimated to have cost the federal budget approximately $60 billion in lost revenue in 2024-25, and this cost is expected to increase substantially.

Concessions on contributions cost the federal government $30,950 million in FY25, rising to $36,750 million in FY28.

Concessions on superannuation earnings were $24,200 million in FY25, rising to $28,250 million in FY28.

Reform should therefore focus on these two areas.

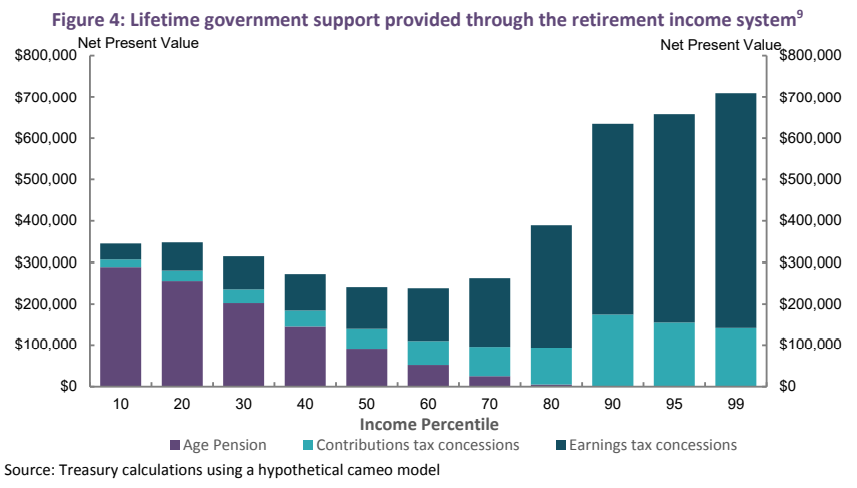

These two superannuation concessions overwhelmingly benefit higher-income earners:

The Australian Treasury also projects that superannuation concessions will cost more than the aged pension.

The Albanese government has announced that it will raise the earnings tax on super balances worth $3 million or more from 15% to 30% without indexation. It would also apply a 30% tax rate to unrealised ‘paper gains’, and these thresholds would not be indexed to account for inflation and wage growth.

The taxing of unrealised gains is opposed by the Coalition and most teal independents, business leaders, the superannuation industry, eminent economists such as former Treasury Secretary Ken Henry (lead author of the 2010 Henry Tax Review) and former Reserve Bank of Australia governor Phil Lowe, and even former ACTU secretary Bill Kelty, who was one of the architects of Australia’s compulsory super system.

Below are three superior alternatives to taxing unrealised capital gains.

Option 1: Lower the threshold to $2 million and apply a 30% tax to only realised gains.

As noted above, in FY25, the Australian Treasury valued superannuation earnings concessions at $24.2 billion, which will rise to $28.25 billion in FY28.

These concessions primarily benefit high-income earners.

The government should lower the $2 million threshold for large superannuation accounts, link it to salary growth, and increase the tax rate on actual (realised) profits from 15% to 30%.

The second 15% of tax would be determined in the same manner as the first, making the reform simple to execute. It would also make superannuation concessions more equitable while generating billions of dollars for the government budget.

Option 2: Tax realised earnings during retirement at 15%:

People over the age of 60 with less than $2 million in retirement accounts currently pay no tax on their earnings, whereas Australian workers pay the full marginal tax rate.

“This is arguably more scandalous than the 15% rate faced by super savers with more than $3 million, who are at least contributing some tax and Chalmers wants to tax more, including on unrealised capital gains”, noted The AFR’s John Kehoe last month.

The standard 15% superannuation tax should be extended to realised earnings on superannuation accounts in the retirement phase.

This would generate significant revenue for the federal budget while also making superannuation concessions more equitable and consistent.

Option 3: Change the 15% flat tax on superannuation contributions to a 15% deduction:

The Australian Treasury estimated that concessions on superannuation contributions will total $30.95 billion in FY25, rising to $36.75 billion in FY28.

To minimise this cost while increasing their equity, the government should substitute the 15% flat tax with a 15% deduction from one’s marginal tax rate.

This simple change would make superannuation concessions on contributions progressive, mirroring one’s marginal tax rate less 15%.

If a superannuant earned $220,000, they would be taxed at their marginal tax rate (47%) minus 15%, for a 32% superannuation contributions tax.

If a superannuant earning $30,000 contributed, they would be taxed at their marginal tax rate (18%) less 15%, for a superannuation contribution tax of only 3%.

These three reform suggestions would improve the equity and sustainability of the superannuation system, resulting in billions of dollars in additional revenue for the federal budget.

They would also remove the complications and pitfalls associated with taxing unrealised ‘paper’ profits.