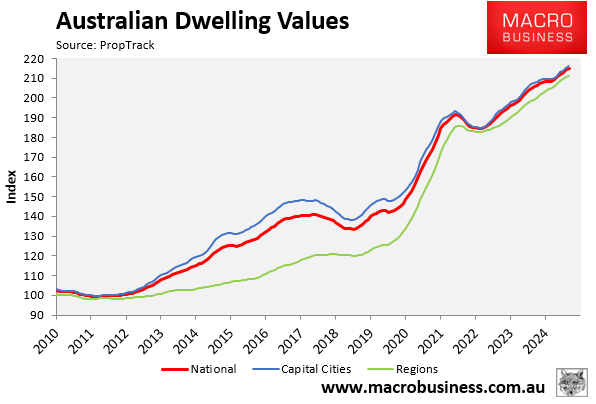

Australian home values reached a new record high in June and are expected to continue growing.

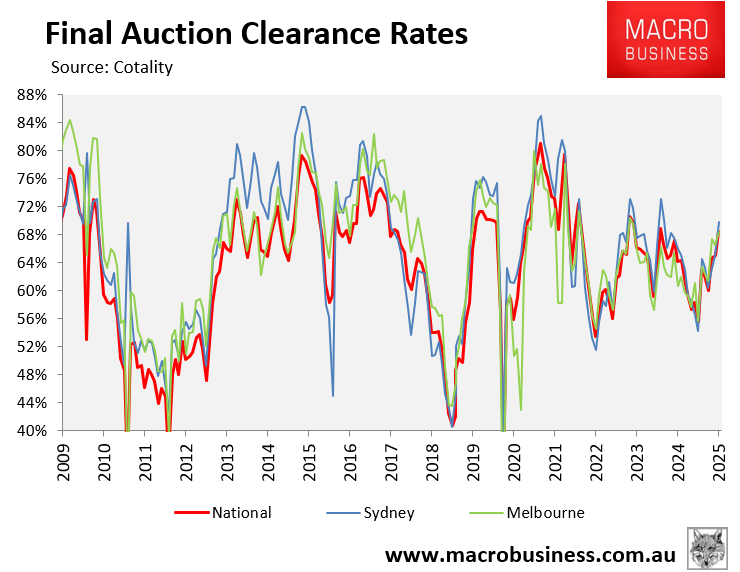

The single-best leading indicator of price growth—auction clearance rates—has bounced, suggesting buyer demand is increasing.

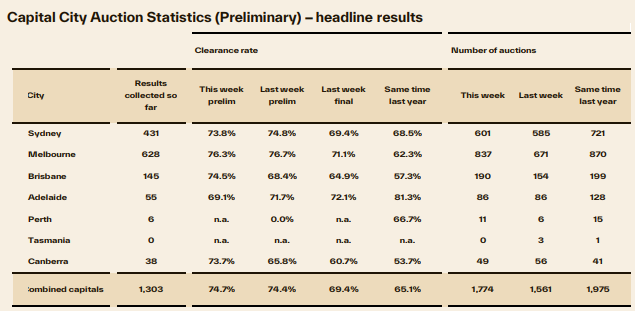

As illustrated below, final auction clearance rates are tracking at their highest levels in more than a year across Sydney, Melbourne, and the combined capital cities.

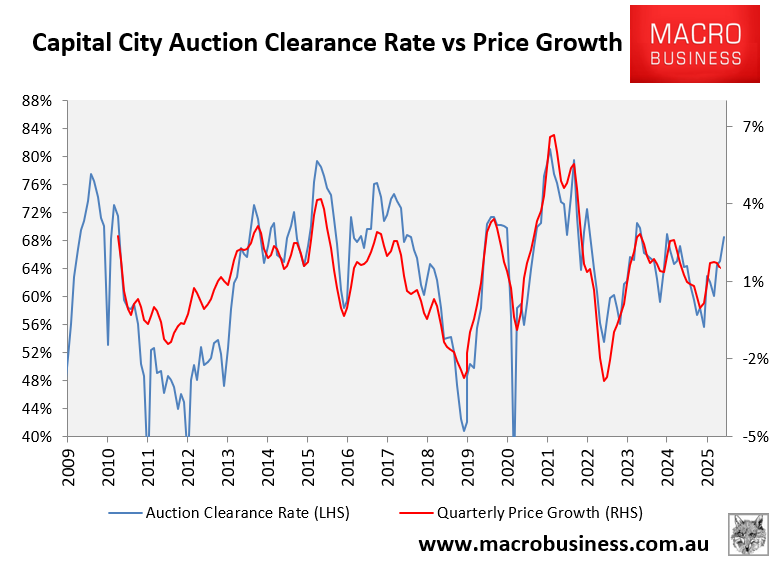

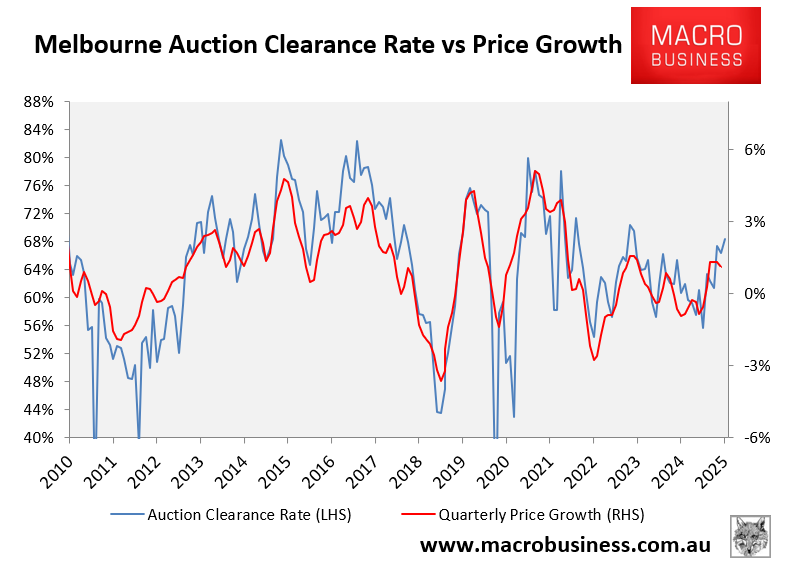

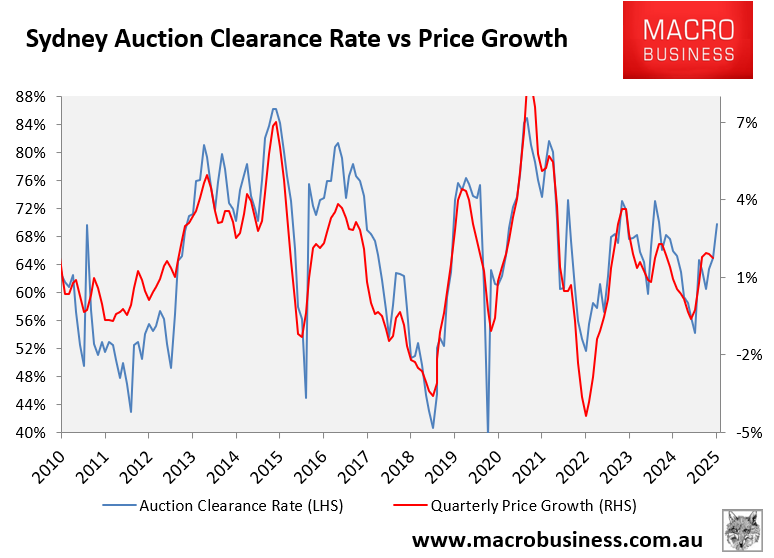

Historically, rising auction clearance rates have corresponded with rising home price growth.

This is true not only at the capital city level but also for the two major auction markets—Melbourne and Sydney.

The following chart plots Melbourne’s monthly average final auction clearance rate against dwelling value growth.

The next chart does the same for Sydney.

Both charts are telling the same story—the surge in clearance rates suggests that home prices will rise in the period ahead.

This weekend’s preliminary auction results from Cotality suggested that buyer demand has continued to increase, with the national preliminary auction clearance rate hitting its highest weekly level since July 2024 at 74.7%.

Source: Cotality

Melbourne’s preliminary clearance rate held firm from last week’s two-year high, slipping slightly from 76.7% to 76.3%. This represented the fifth time in six weeks that Melbourne’s preliminary clearance rate was above 75% and the 13th straight month of 70%-plus preliminary clearance rates.

At 73.8%, Sydney recorded the seventh consecutive month of 70%-plus preliminary clearance rates. However, this week’s fell one percentage point from the week prior (74.8%).

With the Reserve Bank of Australia (RBA) certain to cut the official cash rate further, and stimulatory demand-side housing policies yet to come into effect, buyer demand and home prices are certain to rise further.

Financial markets expect three 0.25% rate cuts over the next 12 months, which would lower the official cash rate to 3.10%.

Recent announced policies will also stimulate demand and home prices, including:

- Labor’s 5% deposit scheme for FHBs (effective 1 January, 2026)

- Exclusion of student debts from loan serviceability calculations.

- Expansion of the Help-to-Buy shared equity scheme.

- Queensland’s announced shared equity scheme.

Various lenders have also announced new stimulatory mortgage products, including:

- 40-year mortgage terms.

- 10-year interest-only mortgage terms without reassessment.

The above measures will inevitably boost borrowing capacity, mortgage demand, and prices.