Some charts from Westpac make the point.

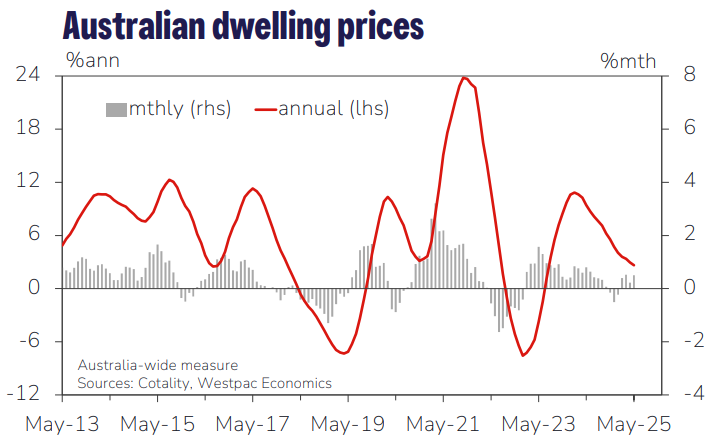

After increasing by 0.6% in May, the Cotality house value index increased by 0.6% in June. The current price increase is 2.3% since January, after a minor 0.8% drop at the beginning of the year.

At 2.7% annually, growth was somewhat stable.

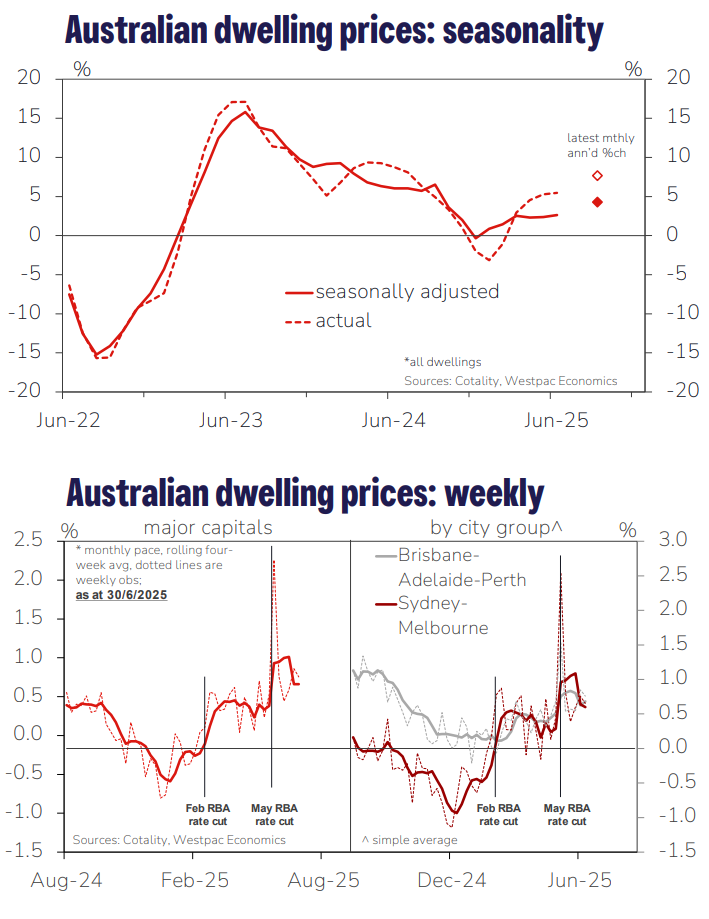

Similar increases were seen in all of the major capital cities, with Melbourne and Adelaide recording 0.5%, Sydney 0.6%, Brisbane 0.7%, and Perth 0.8%.

Monthly price improvements continue to appear to be somewhat flattering due to regular seasonal changes.

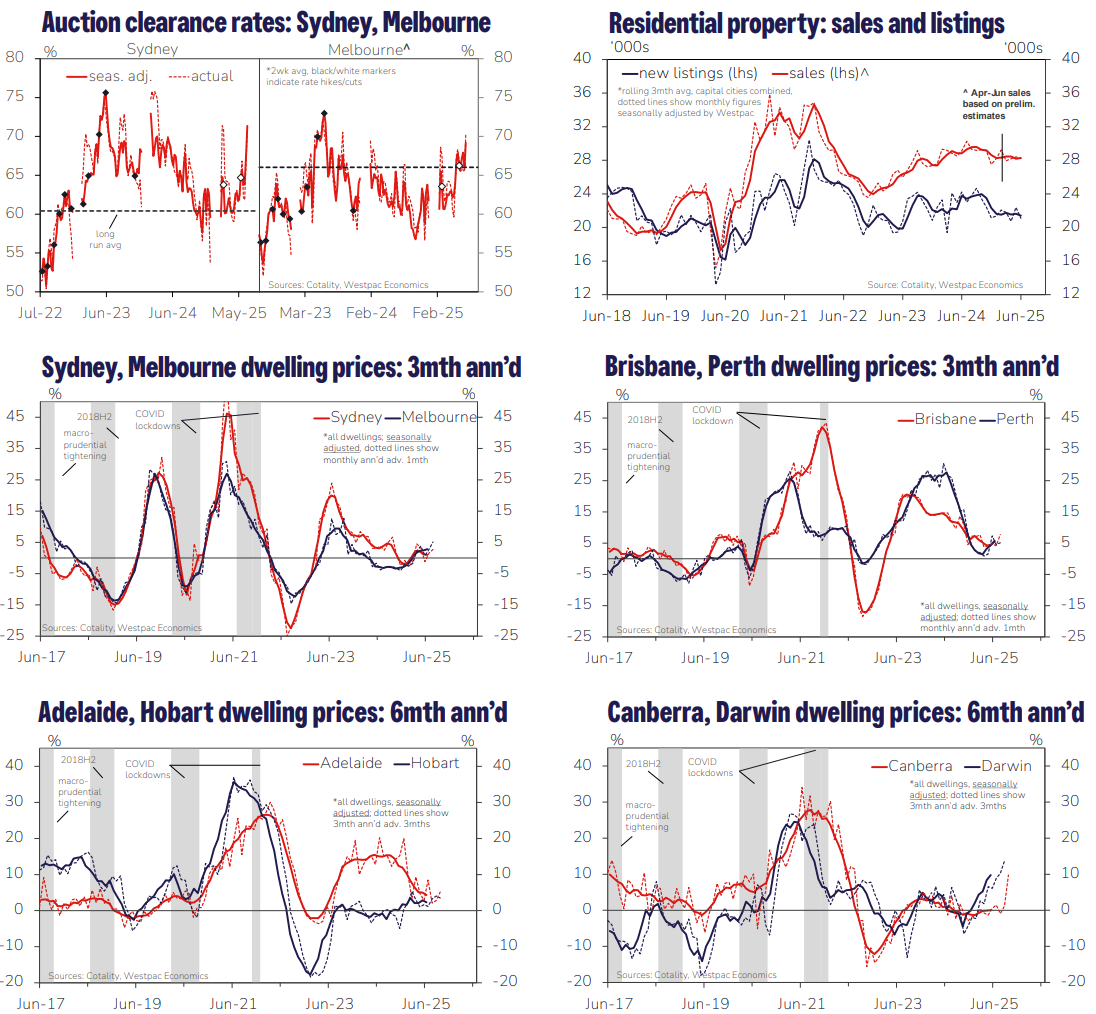

Nevertheless, the upturn appears to be well-established at this point, as evidenced by the most recent auction clearance rates.

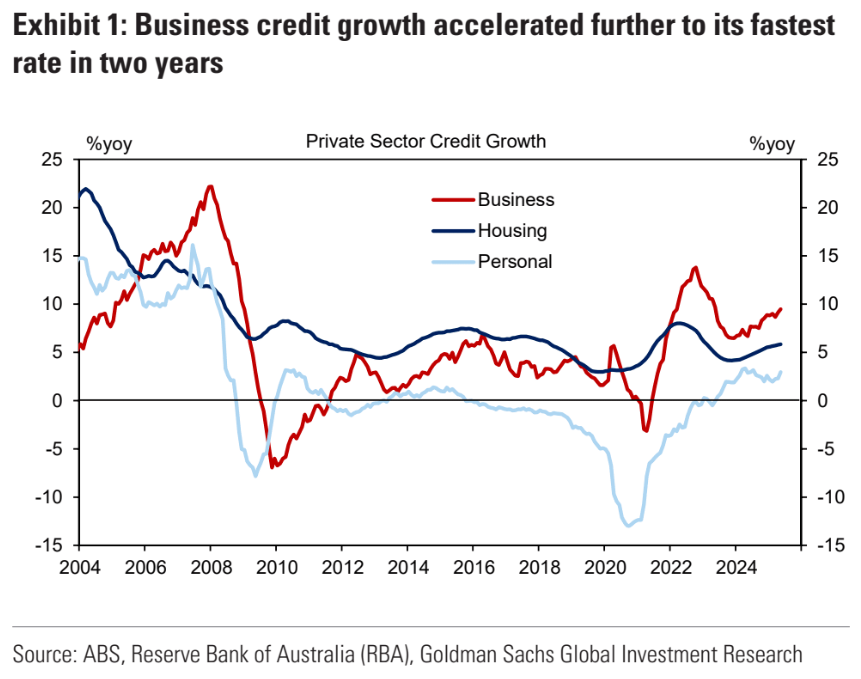

Credit growth is in an upswing as well.

In May, total private-sector credit growth slowed by 20 basis points to 0.5% monthly.

Nevertheless, the year-end rate increased to 6.9% year-over-year, marking its sharpest growth rate since February 2023.

Compositionally, the increase of housing credit remained constant at 0.5%mom, with investor credit growth easing to 0.5%mom and owner-occupier credit growth being constant at 0.5%mom.

Although the year-end rate increased to 9.5%yoy, its strongest growth rate in two years, business credit growth slowed to 0.8%mom.

Growth in personal credit reached 0.5% on average.

As the great terms of trade crash accelerates in the next two years, the RBA will be forced to pump house prices hard as the only alternative for growth.