So says Deutsche.

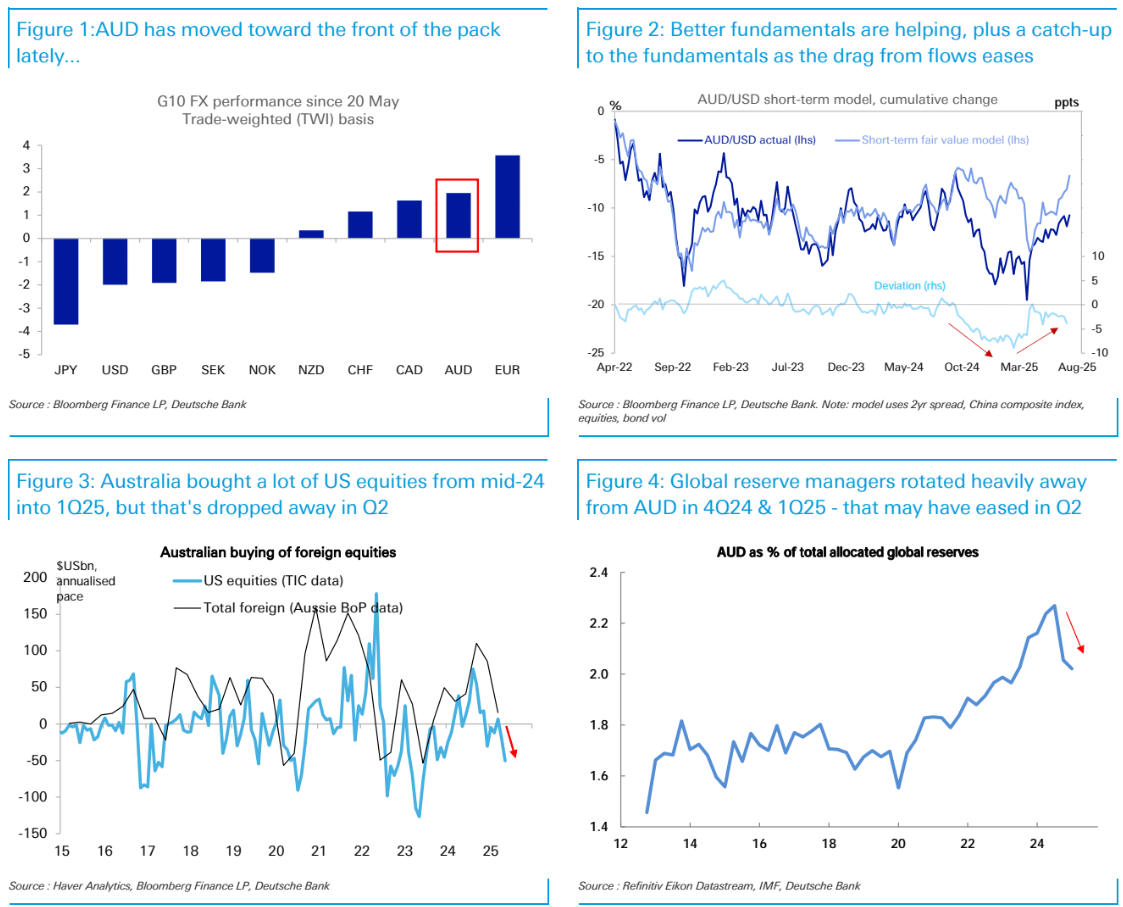

AUD has risen to be the second-best performer in the G10 on a trade-weighted basis since we turned long in the May Blueprint(Figure1).

Our more upbeat view has reflected two key factors.

1.Fundamental support was finally turning: the worst had passed for China and broader risk sentiment, and the domestic Australian economy looked sound, with some fresh green shoots.

2.The AUD would have room to catch up to the fundamentals as the drag from key flows (e.g. super funds’ buying of offshore assets) could moderate.

That seems to be playing out, helping some moderate catch-up already (Figure2).

Super funds bought foreign equities quite aggressively from mid-2024 onwards.

Elsewhere, global reserve managers cut back heavily on AUD exposure around the turn of the year, unwinding a good chunk of the build-up in preceding years (Figure4).

That’s hard to understand, but potentially related to perceived risk sensitivity as the world approached a more turbulent period.

But since then it seems possible that AUD exposure has looked more attractive in a world looking for dollar alternatives, given the strong credit rating, reasonable yields and good liquidity.

At least on the private institutional side, there has been media reports suggesting strong offshore inflows for blue-chip equities and real-estate.

Lastly, it’s not just flows in underlying asset that may be less of a drag on AUD, but the hedging of them.

Super funds’ hedge ratio on offshore equities dropped further in Q1, and at a minimum it’s hard to imagine that falling further recently given the drop in the dollar.

I agree the outlook is still AUD bullish. However, the reasons are wrong.

The market is very short AUD, so that is a support that makes any global ‘risk-on’ circumstance attractive.

However, the local economy remains weak, the interest rate outlook is dovish, a fiscal slowdown is underway, and the bulk commodity accident is coming as the Chinese depression rolls on forever.

This is why the AUD rally has held a relatively flat trajectory versus history, and in 2026, I expect it to reverse.