The economy must suffer, and workers in particular, because the Reserve Bank of Australia will not, under any circumstances, mention immigration.

And so, it carries on like a pork chop about the risk of rising wages; when it is not fighting 620k unemployed, it is fighting 50 million unemployed in India, or 350% unemployment.

There is zero risk of an Australian wage growth breakout. The one chance of it was COVID, with closed borders, yet even then, we were all so browbeaten that it didn’t happen.

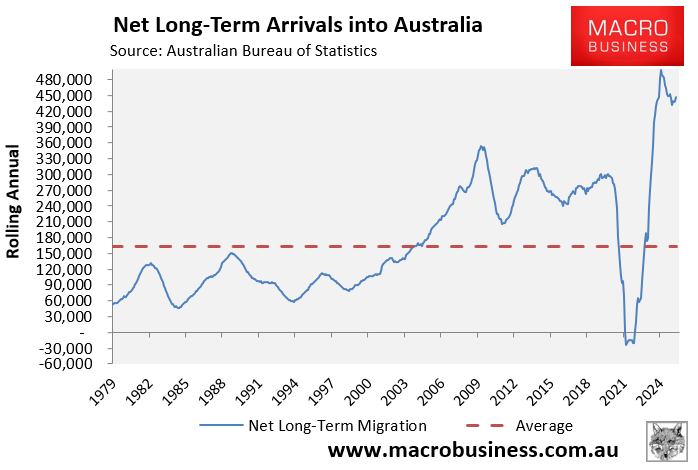

The real risks are all the reverse: a wage growth collapse, as Albo pumps in the cheap foreign labour at astonishing speed.

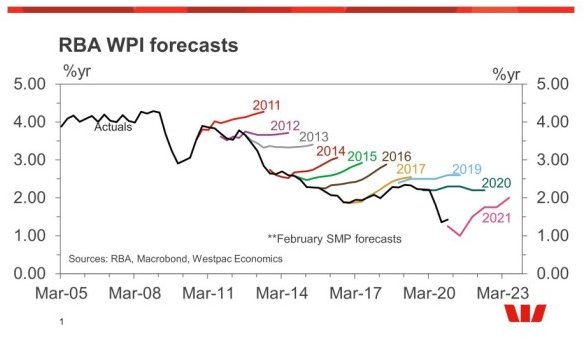

Equally astonishing is that it was this very error that gave rise to Labour’s proposed central bank reforms from the opposition after a decade of the RBA’s wages forecasting failure.

Yet, Treasurer Jim “chicken” Chalmers has engineered an even more woke and wage-dumb new RBA.

To wit, the fowl is coming home to roost. Goldman.

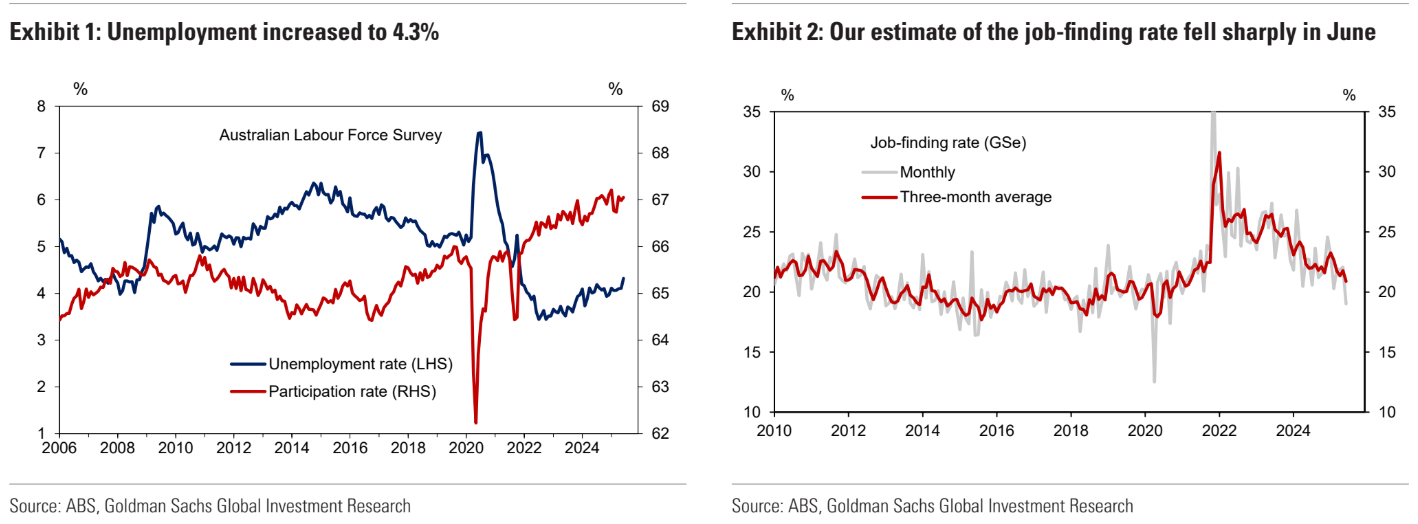

Australia’s unemployment rate increased 20bps to 4.3% in June,against expectations for a stable outcome (GSe/BBG: 4.1%) and marking a new cycle high.

The details of the report were soft, with full-time employment (-38.2k)and hours worked (-0.9%mom) both contracting in the month despite an increase in the participation rate.

Our estimate of the job-finding rate, which is our preferred lead indicator of wages growth, also fell to its lowest level since September 2020.

In terms of policy implications, we continue to expect the RBA to cut 25bp at its next meeting August after its surprisingly hawkish ‘on hold’ decision last week.

The data also support our view that Australia’s labour market is no longer ‘tight’ and should not be a barrier for further cuts.

Yes, you read that right. In forward-looking indicators, we are already back to wage and consumer price growth of the low-inflation period.

Even more astonishing, the freshly blindfolded RBA has decided that, because it can’t mention immigration and therefore can’t forecast, it will now wait for data that is four months old before making any decisions about the future.

Hence, it can lurch from signalling a 50 bps cut in May to not cutting at all in July.

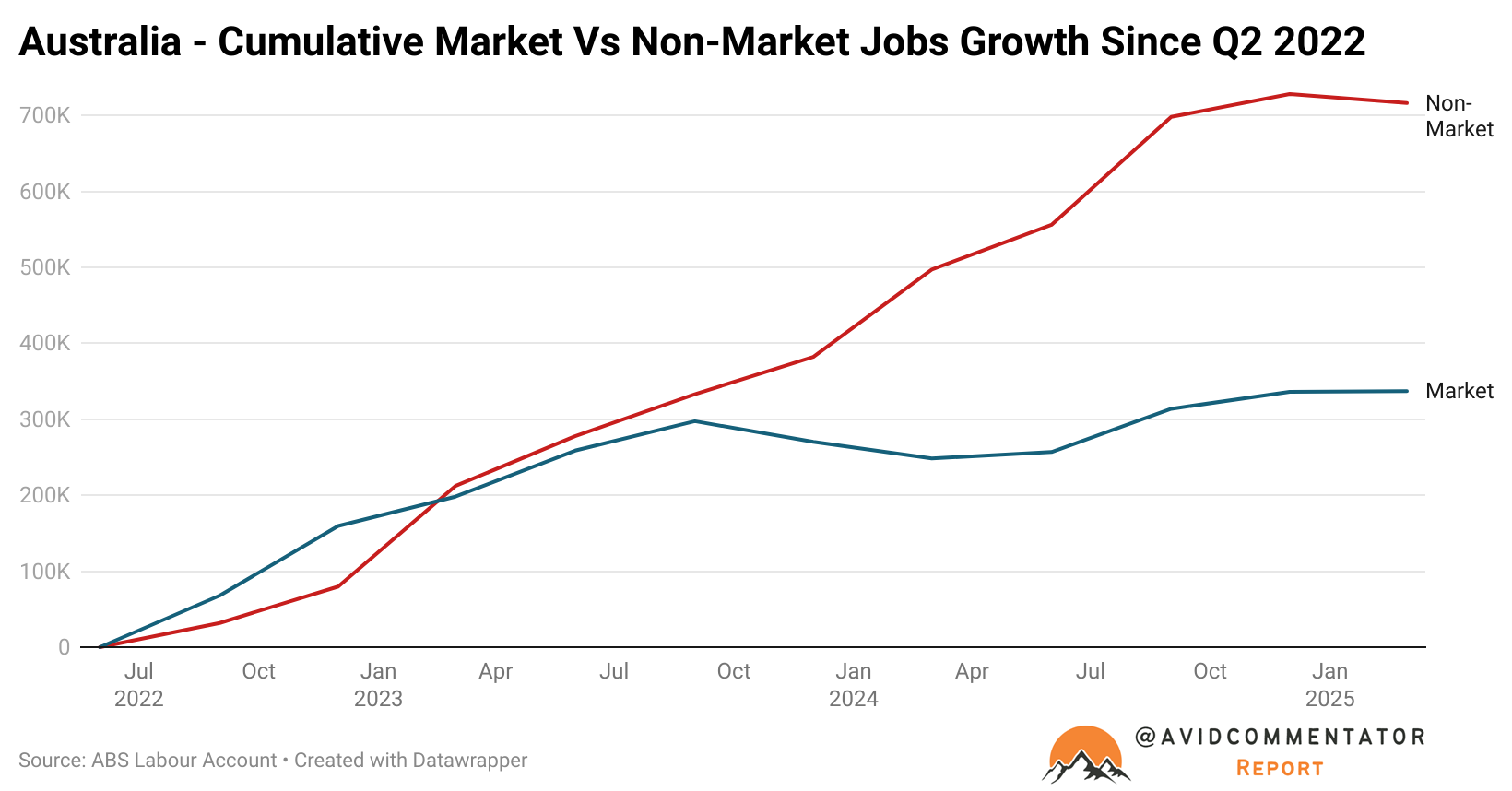

Moreover, because it can’t forecast, it can’t see that there is supposed to be a handoff from public spending to private spending underway for the jobs market, requiring a much lower cash rate.

Finally, because the RBA can’t mention immigration and therefore can’t forecast, it has driven the economy into a ditch just as we head into a rerun of the 2015 great commodity crash, as all bulk commodities head into huge oversupply by year-end.

This ensures that as national income tanks, wage growth and inflation will be punished lower.

The Bullock RBA is already an utter failure. Along with the Chalmers reforms, which have achieved the precise opposite of their intended purpose.