DXY eased lower.

AUD higher.

Lead boots too.

Will gold have another crack?

Metals paused.

EM meh.

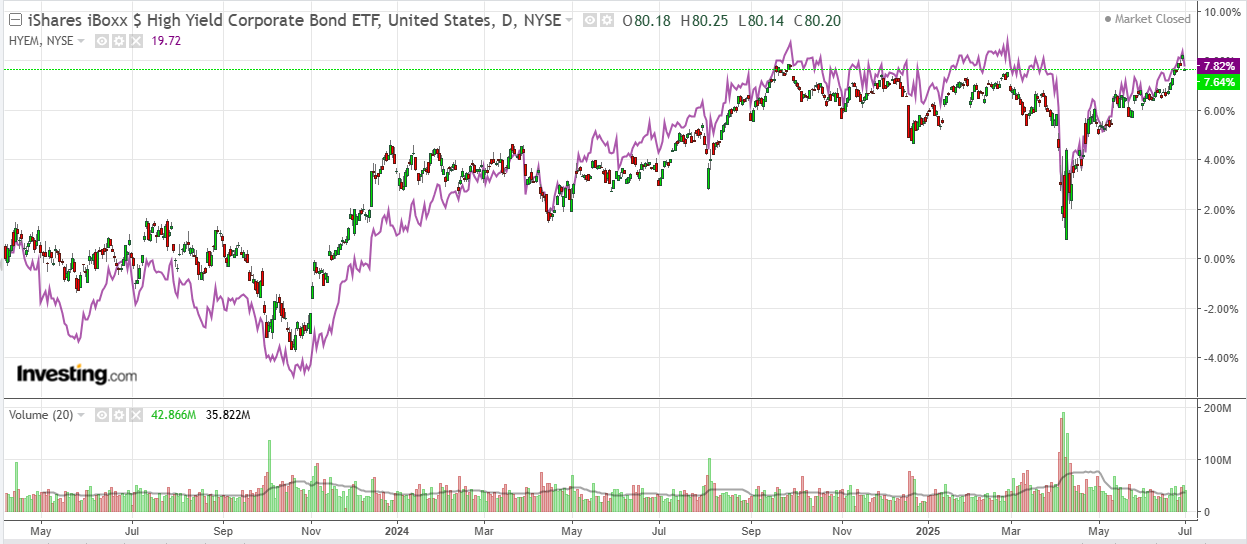

Junk rejection.

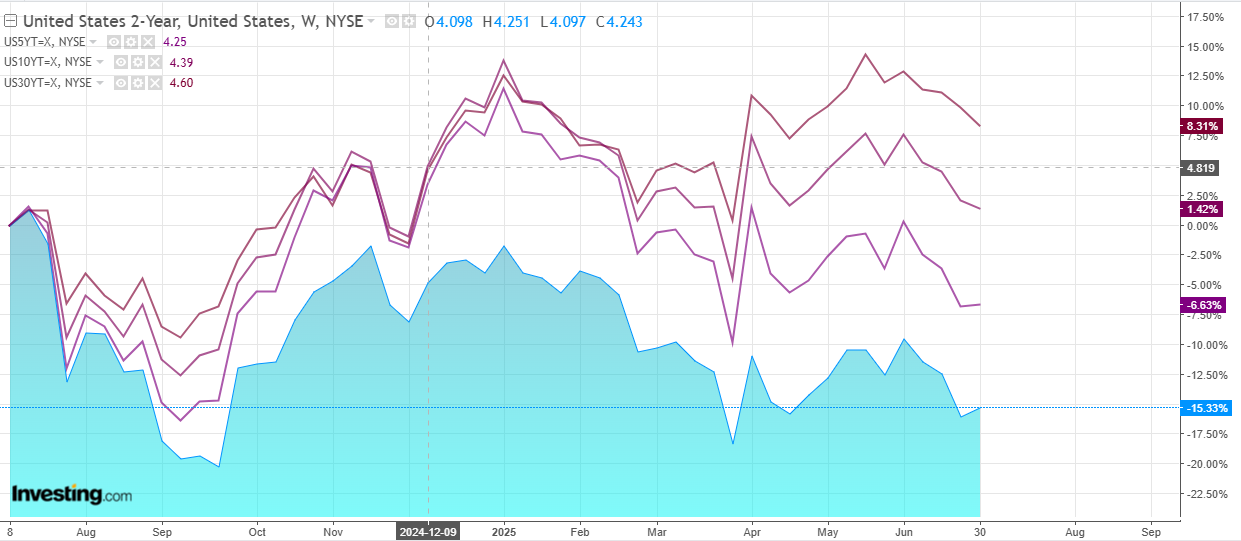

Short end sold on the passage of Trump Big Beautifil Bill.

Stocks sold in EOFY.

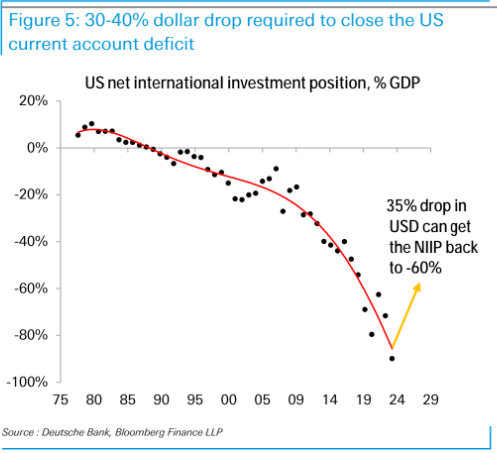

Deutsche says the hiccup in US capital flows is very large indeed.

The US trade numbers have been very volatile in recent months due to tariff front-loading effects.

But now we have fresh data for May which helps smooth out the noise. Remarkably the US trade balance shows little snapback following the large front-loading of imports in Q1, merely returning to the pre-trade war run-rate (chart 3).

Current tariff policy therefore seems to be having little impact on the US external deficit which we estimate to be running somewhere in the 4-5% range.

…Let us assume that the US needs to return to a -60% GDP NIIP, which would be inline with prior historical norms. To get there, the dollar would have to weaken by a further 30-35% from current levels (chart 5).

Remarkably, this is bang in line with our estimates of how much dollar weakness is required to get the current account deficit back in to balance. To be sure, these numbers are extreme, but that’s the point: they highlight just how extreme the current US flow problem is.

Is Trump derangement syndrome enough to put the full Us CAD in play? Not yet. The Trump TACO has seen to that.

Moreover, US assets have been outperforming since May, which may be a counter-trend rally, but it’s not evidence of structural shift to market worrying about the US CAD in the age of liquidity.

I suspect this will be another false alarm about US assets unless or until something more serious impairs its superior profits.

This is why I see the current leg down in DXY, which may well be substantial, as the last, before the Fed arrives and US leads off again.

AUD likely has more to rise.