DXY and EUR have swapped places.

AUD follows EUR.

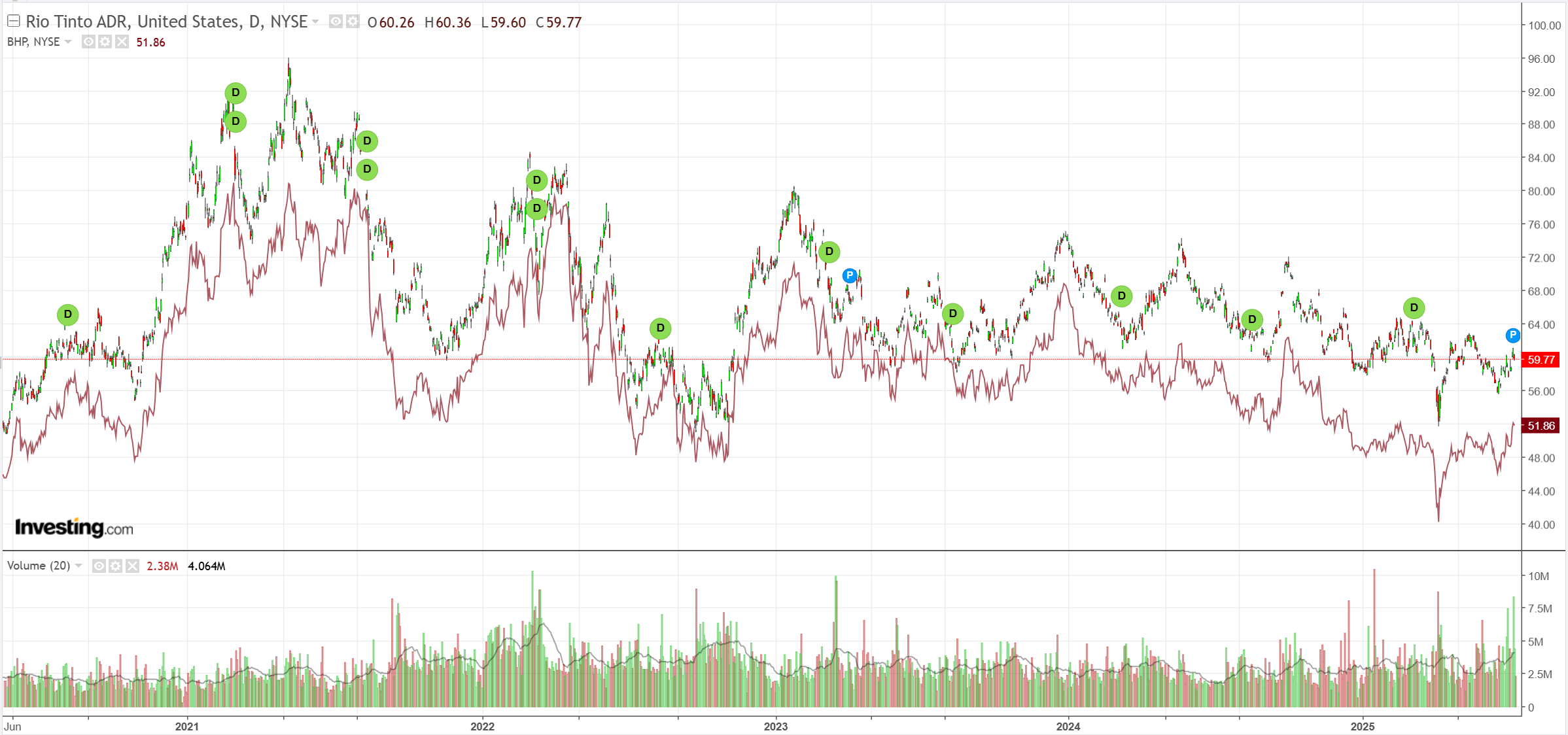

Lead boots plod on.

Gold meh. Oil delusional.

Metals reflation over.

Big mining bear intact.

EM meh.

Junk no bueno.

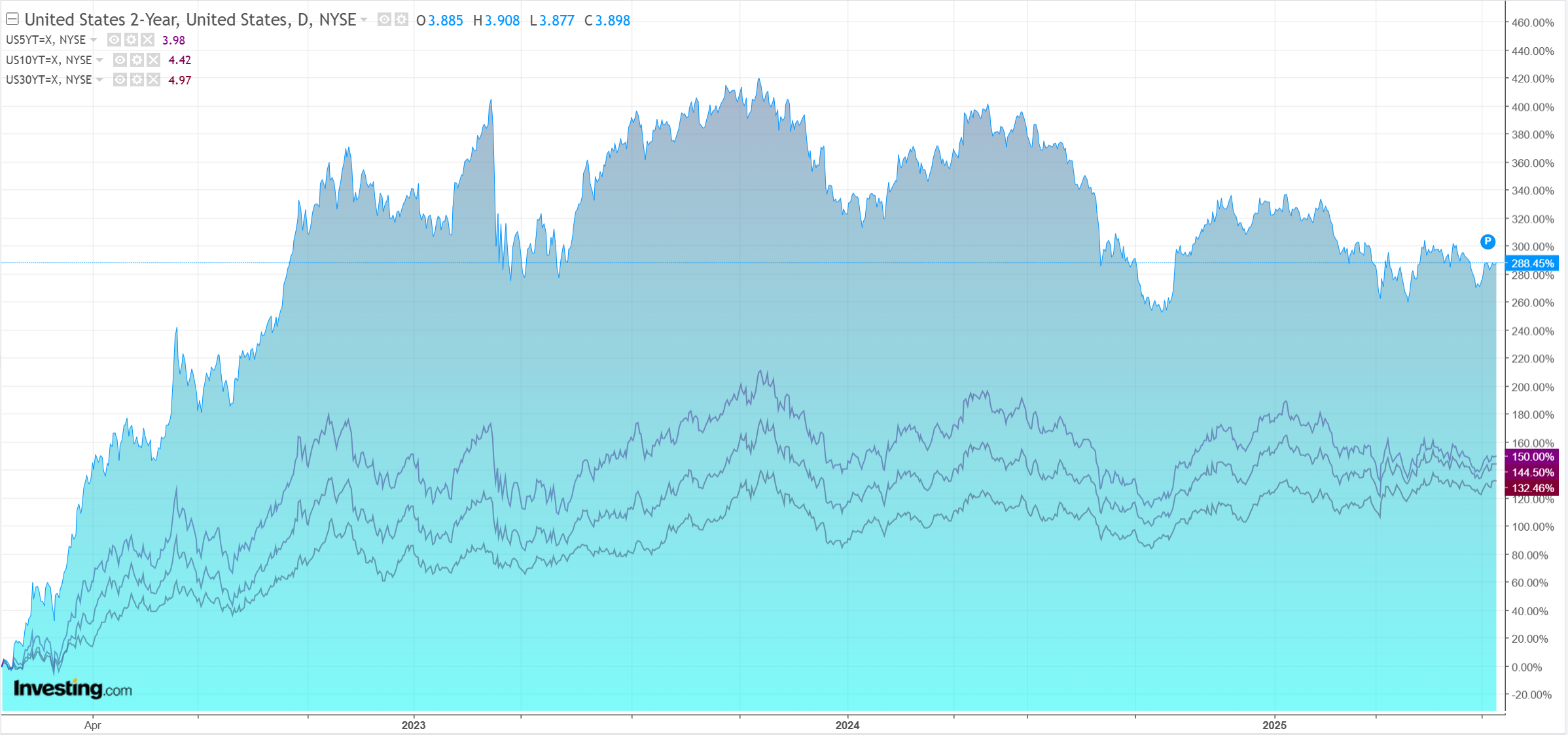

Curve steepening continues.

Stocks hold on.

We await some very powerful and very contradictory outcomes. Tonight, in the US inflation report, which may or may not indicate tariff pass-through to consumers, with big implicatios for assets.

This tips into a broader and even more powerful possibility. Deutsche.

A very senior member of the Trump administration a few days ago sent a letter to Fed Chair Jerome Powell asking whether he misrepresented facts to Congress with regards to the costly renovation of the Federal Reserve head quarters.

Some are arguing that this is opening up a legal avenue for President Trump to remove Chair Powell for cause.

…So how large would we expect the market reaction to be?

The empirical and academic evidence on the impact of a loss of central bank independence is fairly clear: in extreme cases, both the currency and the bond market can collapse as inflation expectations move higher, real yields drop and broader risk premia increase on the back of institutional erosion.

Interestingly, the impact on equities has been far more ambivalent given they are ultimately a claim on real assets.

We would point to the example of rallying equities in Turkey during the unconventional monetary policy period of the CBT.

I think the reaction would be negative for all assets initially. Stocks may fare better before long, but not before the new Fed chair is forced into QE.

More importantly for this discussion, the FX impact is clear. DXY would take another material leg down, and AUD a leg up.

My only addition to this is that the White House narcissist does what he has to stay in the headlines, and he has the added incentive of being crapto.

There’s not a lot of sense in the BTC breakout right now unless you think this is what Trump will do next.

AUD will follow if it happens.