DXY is trying to rally as EUR falls.

AUD is doing OK, but I am increasingly concerned it will top out here.

That said, the big short is relentless support.

Lead boots have stalled.

Gold a bit better. BTC has broken out.

Metal flamed out.

The big mining bear has room to rally and remain intact.

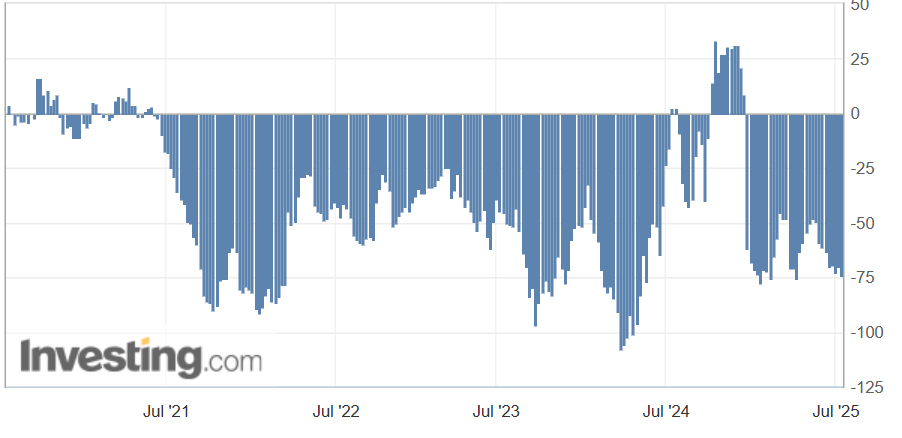

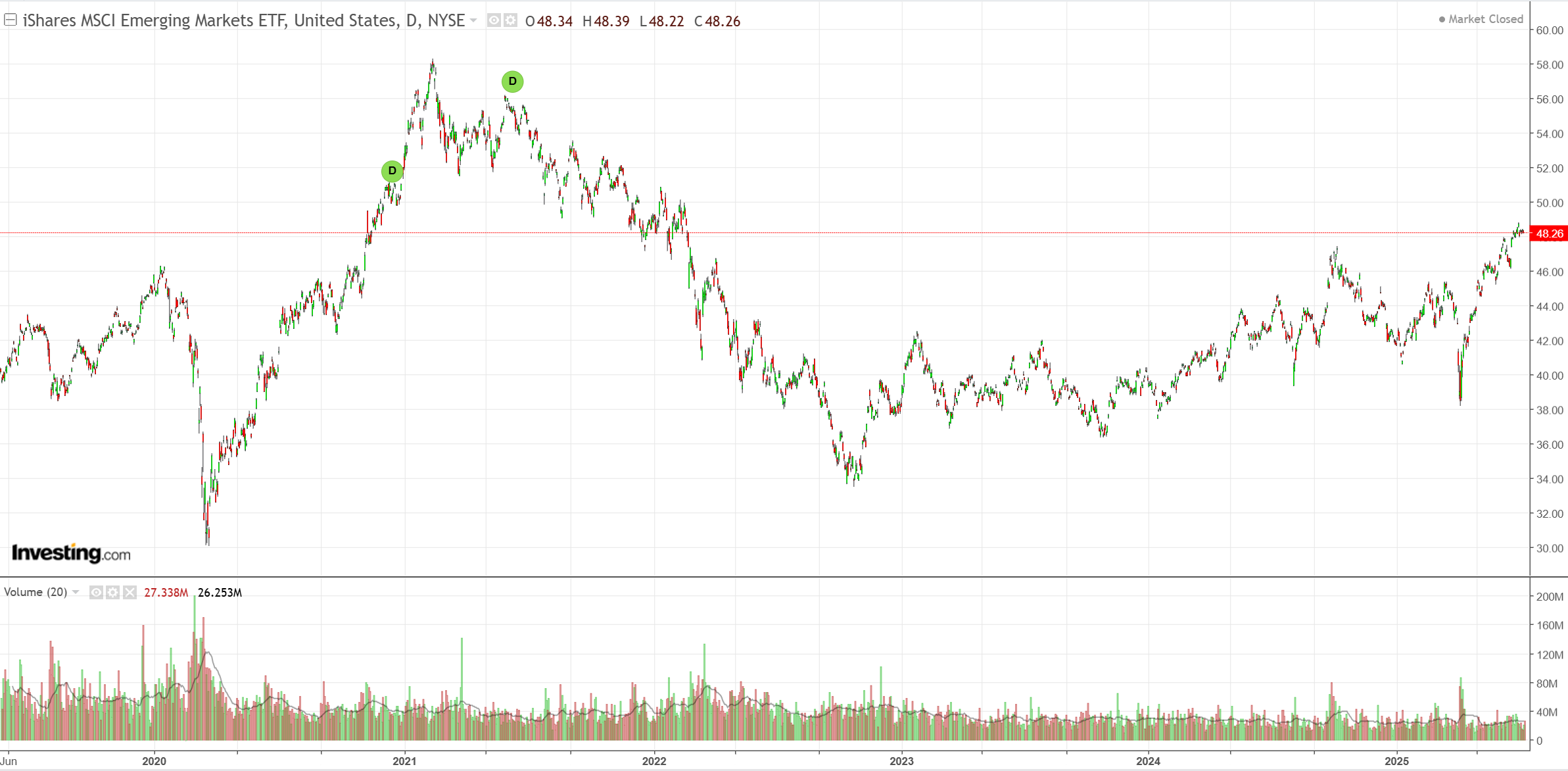

EM meh.

Junk meh.

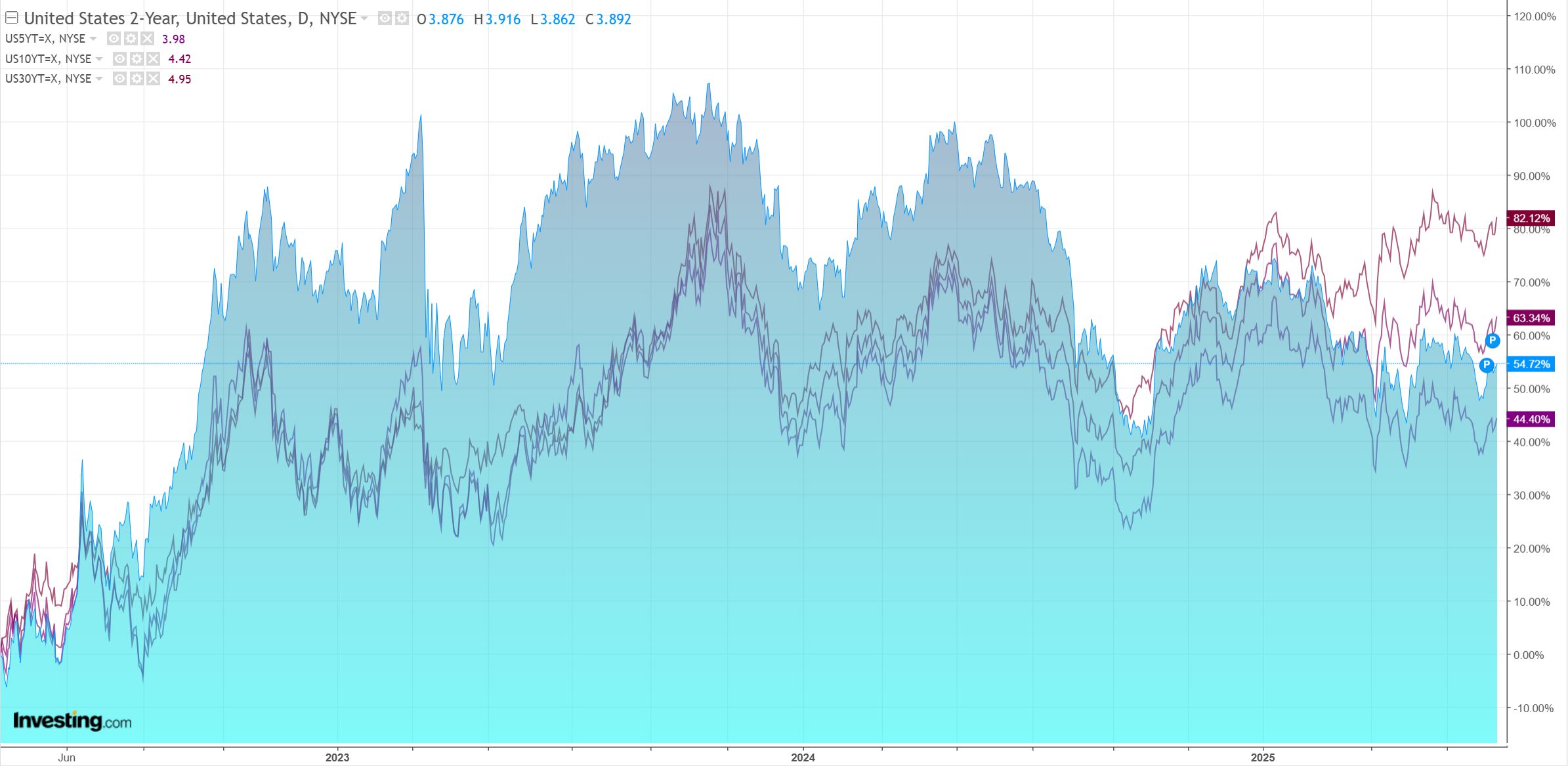

Tariffs are not helping bonds as the curve steepens again.

Stocks look toppy.

Markets have been rallying on expected China yawnulus and the Trump TACO.

The former is coming in the next week or so. The latter has outsmarted itself, with Trump now free to renew his tariff attack as markets price the opposite.

Meanwhile, global macro is still weak or weakening. Goldman.

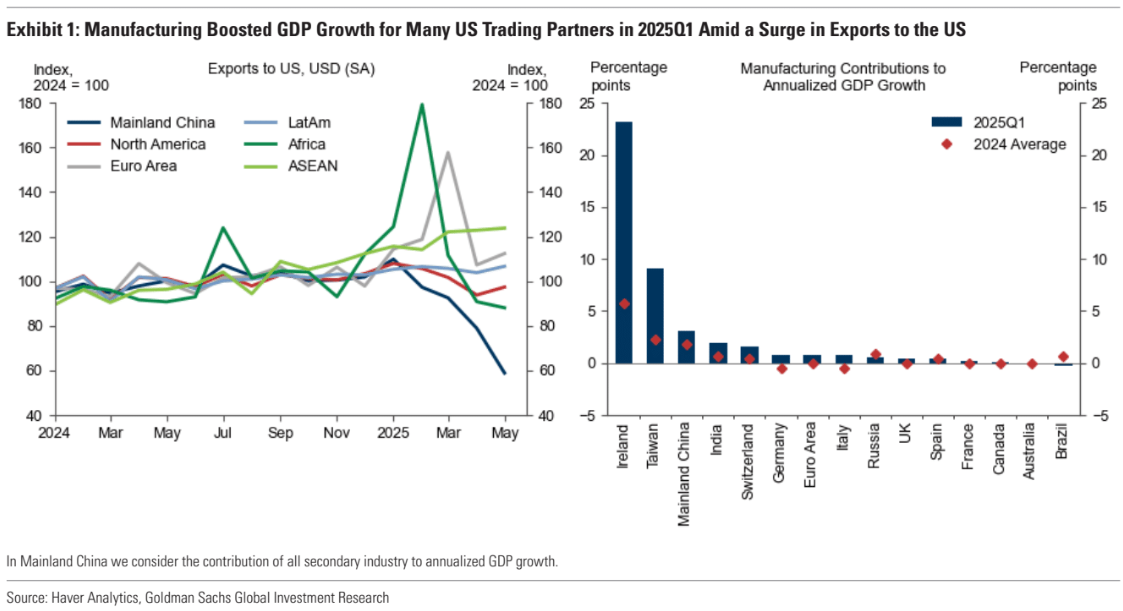

Exports to the US surged in Q1, providing a notable boost to manufacturing activity and GDP for US trading partners.

But two of the tailwinds that drove this surge—the frontloading of exports to the US and a boost to export demand following Dollar appreciation in 2024Q4—are turning to headwinds, and the implementation of tariffs should further dampen foreign export growth in the coming months.

Estimating the impact from each channel implies that frontloading should fully reverse within the next 3 months, that the recent USD depreciation will lower total real exports by 3%, and that the implementation of tariffs will lower total exports by 3%.

Combined, these drags imply a 4-15% hit to overall exports in major economies.

The trade pullback is likely to spill over to broader activity, and the historical relationship between trade and activity suggests that trade headwinds could lower industrial production by 1-5% and manufacturing PMIs by 1-4pts in the coming months.

These patterns are consistent with our forecasts for a downturn in global ex US GDP growth for the rest of 2025.

Slowing global growth is not the stuff of ongoing DXY depreciation.

AUD is gathering headwinds.