After years of failure, the RBA has given up entirely on forecasting and is driving through the rearview mirror. Goldman.

In her post-meeting press conference Governor Bullock stressed that the decision to pause the easing cycle was “about timing rather than direction” with the RBA just “looking for further confirmation we are on the forecast path”.

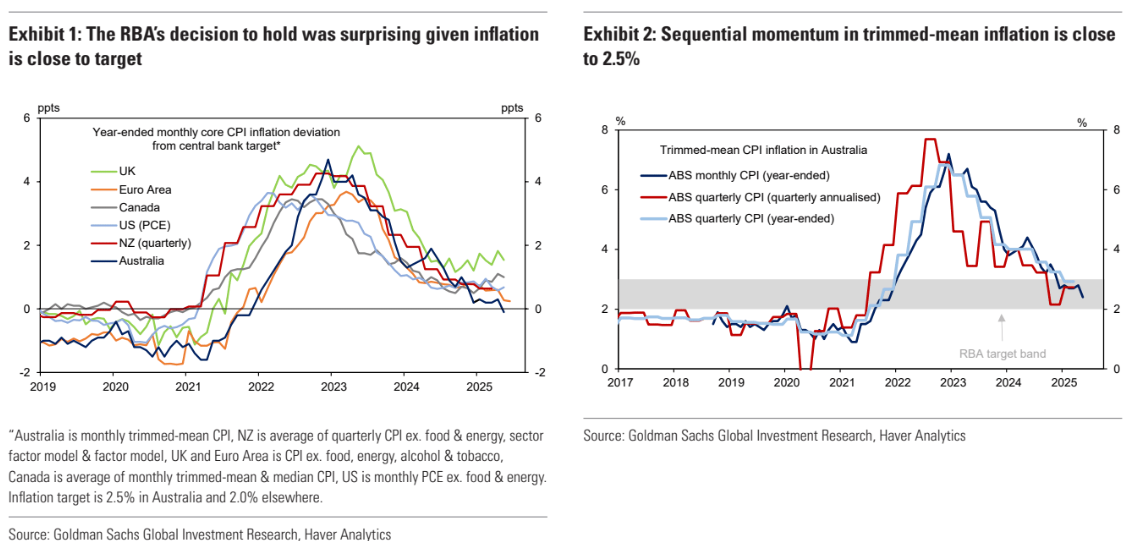

The Governor reasoned a “cautious approach” was warranted because year-over-year growth in the quarterly trimmed mean inflation had only just returned to the 2-3% target band (2.9%yoy), the labour market remained resilient, and also due to elevated global uncertainty.

From our perspective, today’s decision highlights continued volatility in the RBA’s reaction function and particularly given a 50bp cut was considered when the RBA cut 25bp in May and the fact that private consumption surprised to the downside again in the 6 weeks since then.

We were also surprised to see the publication of Board votes today as these were not accompanied by an updated Statement on the Conduct of Monetary Policy (SOCOM).

The existing SOCOM required unattributed votes to be published in April and May, after the new Board commenced, but was seemingly ignored.

For now, absent a global shock, it appears the RBA has a strong bias to only adjust policy gradually at meetings following the comprehensive quarterly CPI report and RBA forecast rounds.

We now forecast 25bp cuts in Aug, Nov and Feb to a terminal rate of 3.1% (prior: July, Aug, Nov to 3.1%).

However, we see the balance of risks to our central scenario as skewed towards a deeper easing cycle if the RBA’s focus on year-over-year changes in the quarterly CPI data potentially proves to be too backward looking and risks “falling behind the curve”.

In particular, we note sequential measures of quarterly trimmed mean inflation that have already retreated to the lower half of the target band (6mth annualized: +2.46%) and also clear disinflationary signals across the more timely monthly measures (May trimmed-mean: +2.4%yoy).

A few months ago, I labelled Governor Bullock a ditherer. It is worse than that.

What is the purpose of an RBA that is too gutless to forecast? Zero. Anybody or anything can adjust the cash rate based on backward-looking data.

The RBA costs taxpayers $501m to run. Abolish it and use a $300 second-hand desktop to adjust rates instead.

No need for an AI. It can be done via a few macros in Excel, calculating last quarter’s inputs. Give the $500m to the poor.

The RBA has become nothing more than a vested interest of overpaid and fattened economists who are too afraid to do their job.

Abolish it.