Victoria’s economy has become a national disaster.

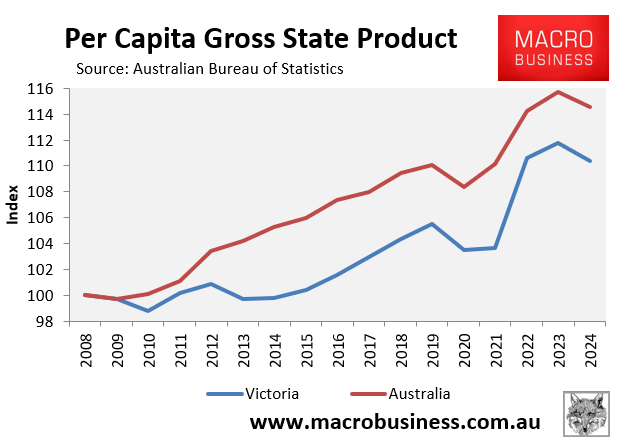

The Australian Bureau of Statistics’ (ABS) annual state accounts for 2023-24 revealed that Victoria’s per capita GDP fell by 1.2% annually and has only increased by 10.4% since the Global Financial Crisis (GFC) in 2008.

Victoria’s growth compares poorly against the 1.0% national decline in per capita GDP in 2023-24 and the 14.5% gain since 2008.

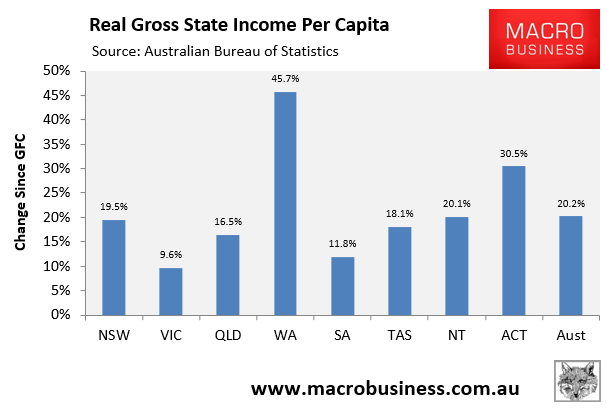

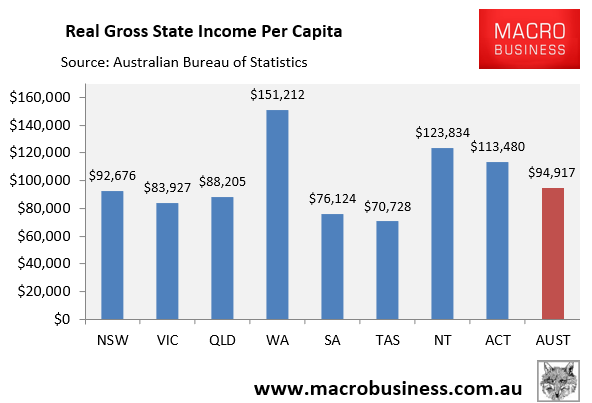

Victoria has likewise experienced the nation’s smallest increase in gross state income per capita since the GFC.

In 2023-24, Victoria had the third-lowest real gross state income in the country, ahead of Tasmania and South Australia.

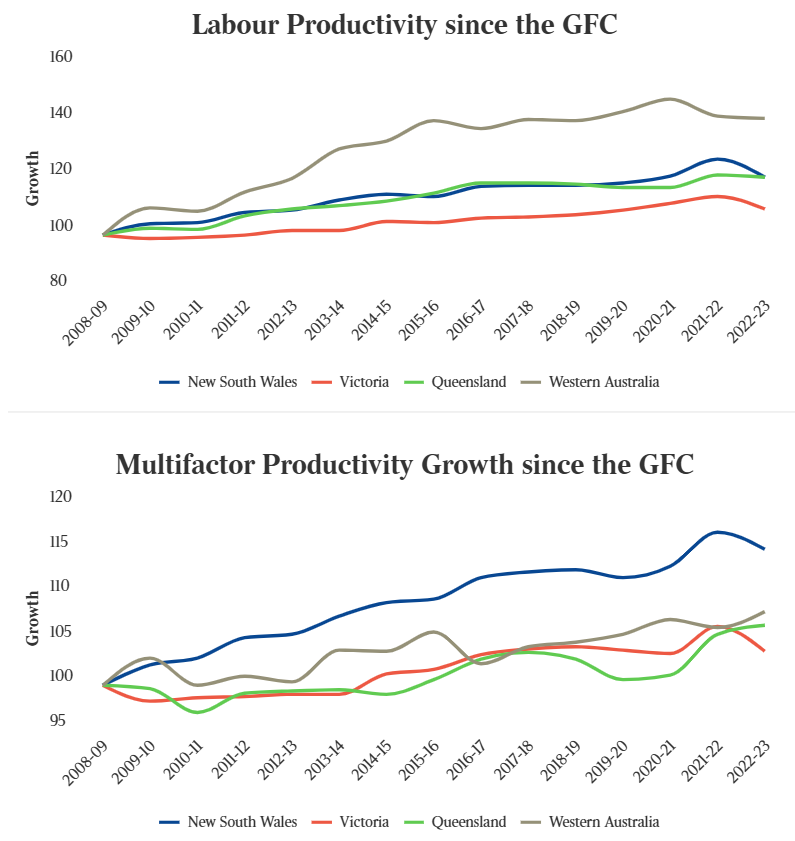

Victoria’s productivity growth rate was equally poor, tracking at less than one-third that of New South Wales.

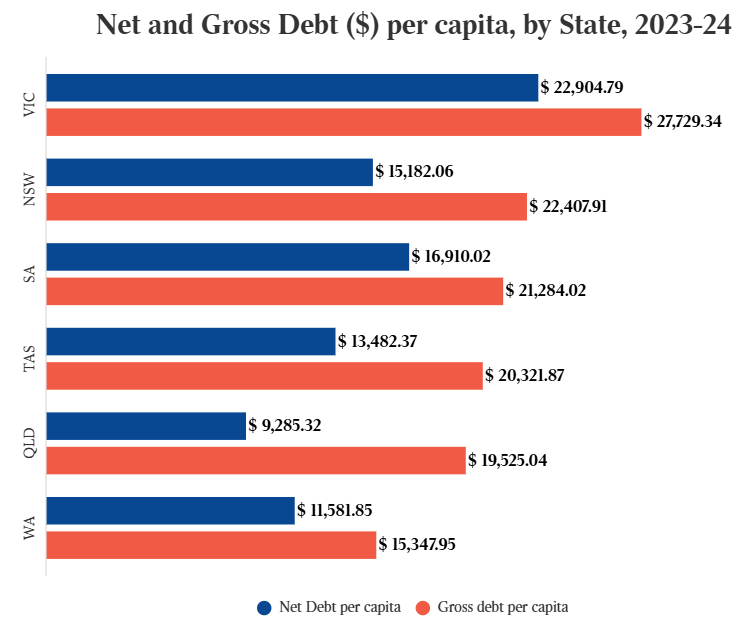

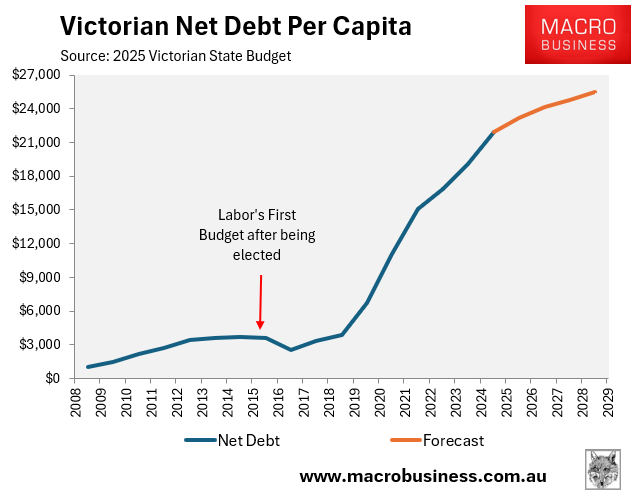

Victoria also has the highest per capita debt and the lowest credit rating out of Australia’s states and territories in 2023-24.

New state data published by the CBA shows that Victoria’s economy continues to lag the nation.

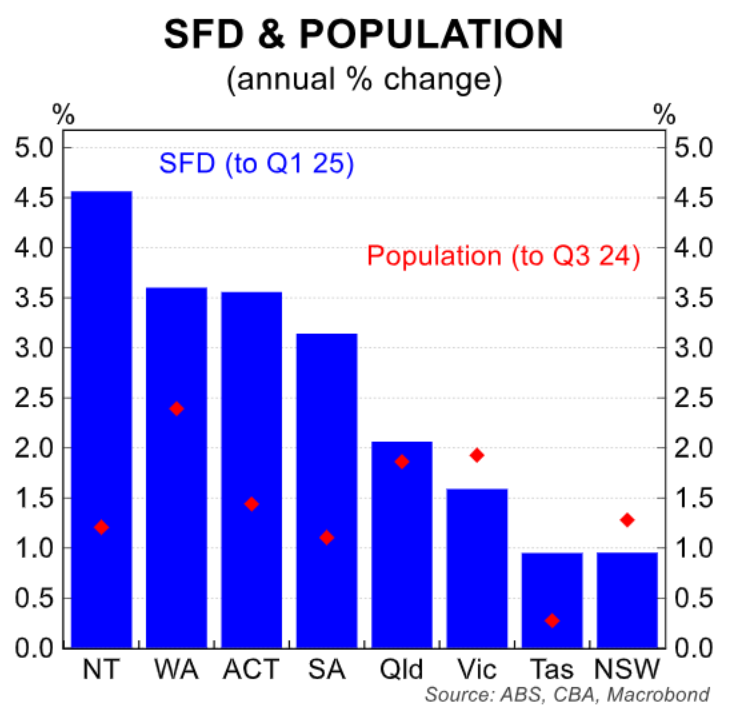

Victoria’s state final demand lagged well behind its population growth in the year to Q1 2025:

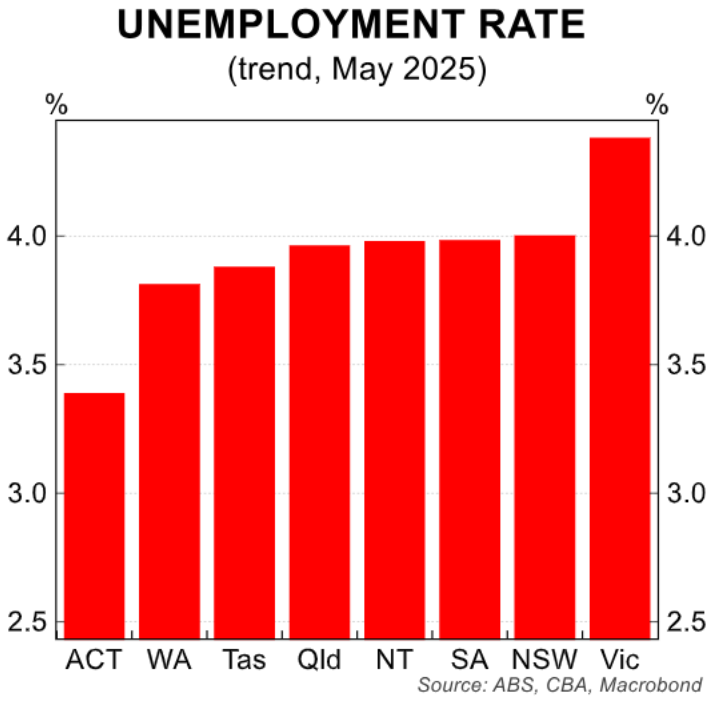

Victoria’s trend unemployment rate in May (4.4%) was also the highest in the nation, tracking well above the national average (4.1%).

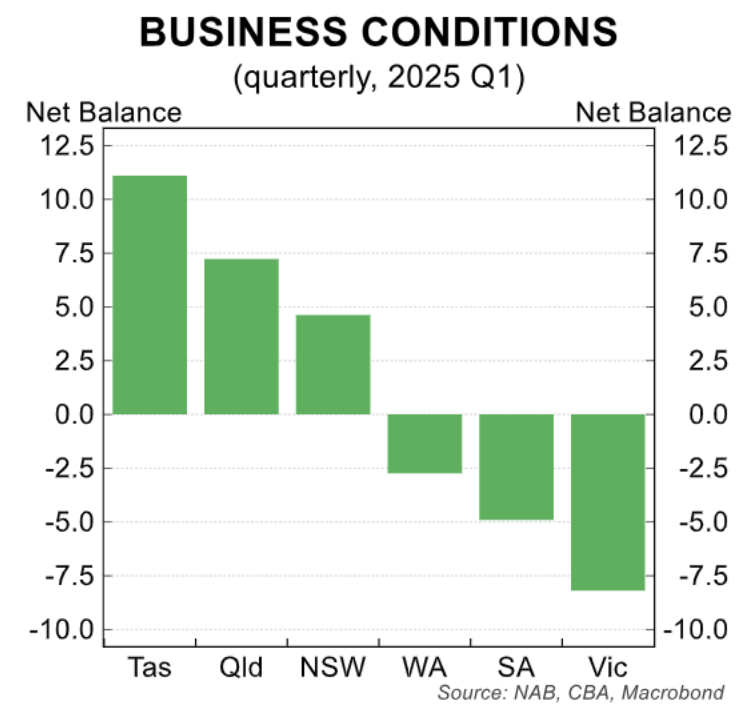

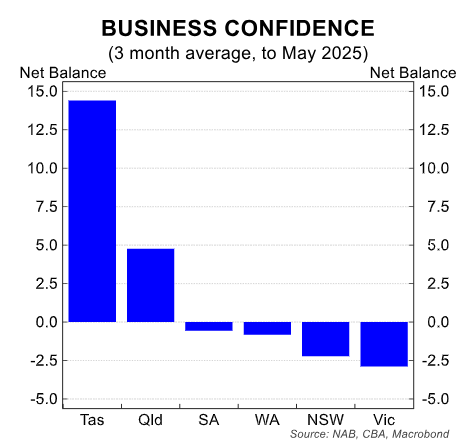

Meanwhile, the NAB business survey showed that business conditions were easily the worst in Victoria in Q1 2025:

Victoria also had the poorest business confidence in Q1 2025.

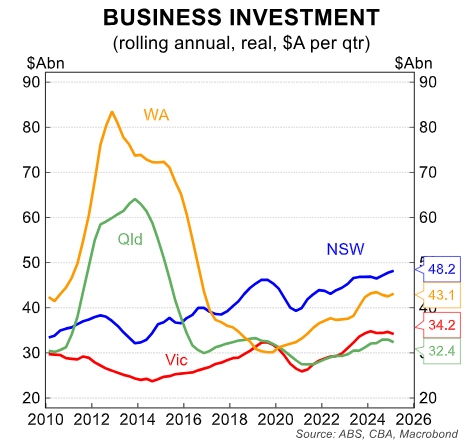

Victoria’s business investment is also poor, tracking well below NSW and Western Australia and only marginally ahead of Queensland (which has a far smaller economy and population).

Victoria’s economic growth strategy is predicated on importing a huge number of people to construct homes and infrastructure and offer services.

The state’s population has expanded by around 2.5 million people this century and is officially predicted to grow by an additional 4.2 million people during the next 31 years.

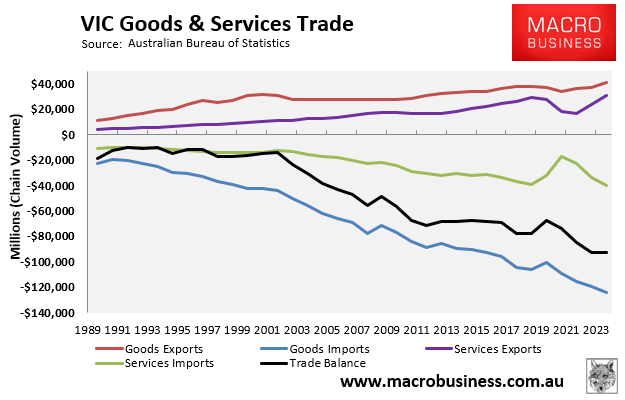

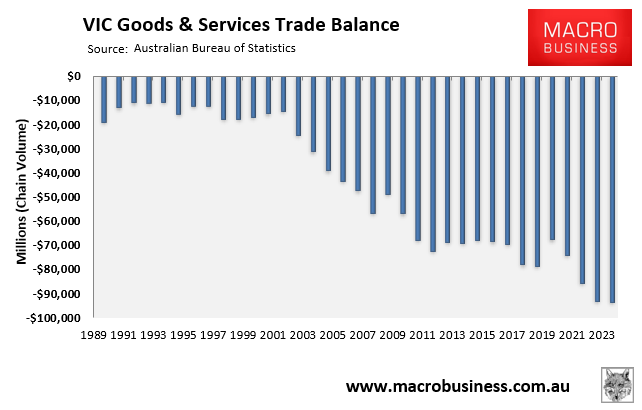

Victoria’s trading performance is indicative of its ‘Ponzi’ economy.

Exports have expanded at a slow rate over the last two decades, while imports have surged.

As a result, the state’s trade deficit soared to $92.9 billion in the financial year ending Q2 2024:

Victoria (via Melbourne) is essentially draining financial resources from mining states to fund its population ‘Ponzi’ plan, growing for the sake of growth via mass immigration and debt accumulation.

This ‘Ponzi’ growth model has resulted in perpetual infrastructure bottlenecks and lower living standards for incumbent residents due to rising congestion, reduced amenity, and deteriorating housing affordability.

It has also pushed the state deep into debt as it struggles to build its way out of the never-ending population crisis.

The Victorian government needs to develop an economy based on real and sustainable growth that raises the existing population’s living standards.

The first step is to push the federal government to reduce immigration to a manageable and sustainable level.

Endless mass immigration will bankrupt the state and erode living standards.