Geoff Wilson, founder of Wilson Asset Management, stepped up his attack on the Albanese government’s proposed tax on unrealised superannuation capital gains, which he labelled “unfair” and “un-Australian”.

The proposed policy would increase the earnings tax on superannuation balances of $3 million or more from the current 15% to 30% without indexation. It would also apply the 30% tax rate to unrealised ‘paper profits’.

Speaking to Radio 2GB’s Ben Fordham, Wilson argued that without indexation, a typical full-time Australian worker commencing their working life today would be taxed on unrealised gains by the time they retire.

Wilson’s criticism is supported by AMP Deputy Chief Economist Diana Mousina, who told Sky News:

“An average 22-year-old today, who’s earning average full-time earnings, will hit the cap when they get to about 62 years old on my analysis”.

“So that’s before they actually reach retirement”.

“My estimates were actually, I think, understating the amount of people that will hit the cap because I used quite low return assumptions”.

Mousina also warned that “if people know that their super is going to be hit”, then “more people will probably go to purchase a home, which has implications for home prices in the future”.

“So people will find a way around this system to try and reduce their taxable income as much as possible”, she said.

Geoff Wilson also warned that taxing unrealised gains could also stifle investment in start-ups, given some investors use their SMSFs as a low-tax investment vehicle for startup businesses.

This echoed Wilson Asset Management’s recent note to shareholders, which stated the following:

“Under taxing of unrealised gains every funding round would require tax to be paid on a hypothetical valuation”.

“Most startups operate with negative cashflow and when capital is raised it is to fund growth, not to provide liquidity to investors”.

“Therefore, there is no liquidity to pay tax on an unrealised gain”.

The taxing of unrealised gains is opposed by the Coalition and most teal independents, business leaders, the superannuation industry, eminent economists such as former Treasury Secretary Ken Henry (lead author of the 2010 Henry Tax Review) and former Reserve Bank of Australia governor Phil Lowe, and even former ACTU secretary Bill Kelty, who was one of the architects of Australia’s compulsory super system.

Below are three superior choices to taxing unrealised capital gains.

Option 1: Lower the threshold to $2 million and apply a 30% tax to realised gains only.

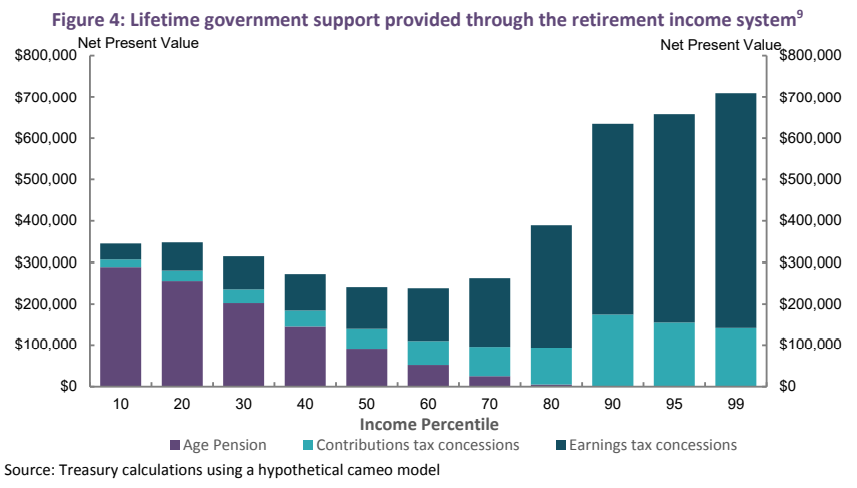

The Australian Treasury valued concessions on superannuation earnings at $24.2 billion in FY25, rising to $28.25 billion in FY28.

As illustrated in the following chart, these concessions on earnings overwhelmingly benefit high-income earners.

The government should reduce the threshold for large superannuation accounts to $2 million, index it to wage growth, and raise the tax rate on actual (realised) earnings from 15% to 30%.

The second 15% of tax would be calculated the same way as the first, making this reform easy to implement. It would also make superannuation concessions more equitable and raise billions of dollars for the federal budget.

Option 2: Tax earnings in the retirement phase at 15%:

Currently, people over 60 with less than $2 million in a retirement account pay no tax on their earnings, while Australian workers pay full marginal tax rates on theirs.

“This is arguably more scandalous than the 15% rate faced by super savers with more than $3 million, who are at least contributing some tax and Chalmers wants to tax more, including on unrealised capital gains”, noted The AFR’s John Kehoe last week.

The standard 15% tax on superannuation should, therefore, be extended to realised earnings on superannuation accounts in their retirement phase.

Doing so would raise significant funds for the federal budget and make superannuation concessions fairer and more consistent.

Option 3: Replace the 15% flat tax on superannuation contributions with a flat 15% deduction:

The Australian Treasury estimated concessions on superannuation contributions to be $30.95 billion in FY25, rising to $36.75 billion in FY28.

To reduce the cost of these concessions and improve their equity, the government could replace the 15% flat tax with a 15% deduction from one’s marginal tax rate.

This simple adjustment would make superannuation concessions on contributions progressive by matching one’s marginal tax rate minus 15%.

If a superannuant’s income were $220,000, they would be taxed at their marginal tax rate (47%) less 15%, resulting in a 32% superannuation contributions tax.

If a superannuant earning $30,000 contributed, they would be taxed at their marginal tax rate (18%) minus 15%, resulting in a superannuation contributions tax of only 3%.

The above three reform proposals would enhance the equity and sustainability of the superannuation system, raising billions of dollars in additional revenue for the federal budget.

They would also eliminate the complexities and pitfalls associated with taxing unrealised ‘paper’ gains.