By Harry Ottley, Economist at CBA

- TheAustralian unemployment rate remained steady at 4.1% in May.

- Population growth in Australia continues to ease, with the annual rate down to 1.7% in Q4 24.

- News offshore was dominated by geopolitical events as Israel and Iran continued hostilities following initial Israeli strikes a week ago.

- The FOMC left the Fed Funds rate steady but flagged an incoming stagflationary impulse to the economy from tariffs.

- Next week, the focus locally will be on the May CPI indicator, which we expect will show inflation easing to 2.3%/yr.

- Offshore, the focus will remain on geopolitics as President Trump mulls direct US involvement in the conflict. The overseas dataflow is light on, but the PCE deflator in the US will garner attention, albeit we forecast it to remain benign for now.

The attention of financial markets was squarely on the Middle East this week. The conflict between Israel and Iran has intensified, creating market jitters and pushing oil prices higher.

US President Trump is actively considering directly involving US forces in the war, which could materially increase volatility in coming weeks.

As our Head of International Economics Joseph Capurso noted, the conflict only increases the stagflationary impulse facing the global economy. It has also proved a distraction from the other major downside risk to the global economy –US trade policy.

The first pause on tariffs is due to expire on July 9 with the risk of the US ratcheting up tariffs again not currently priced in by markets in our view.

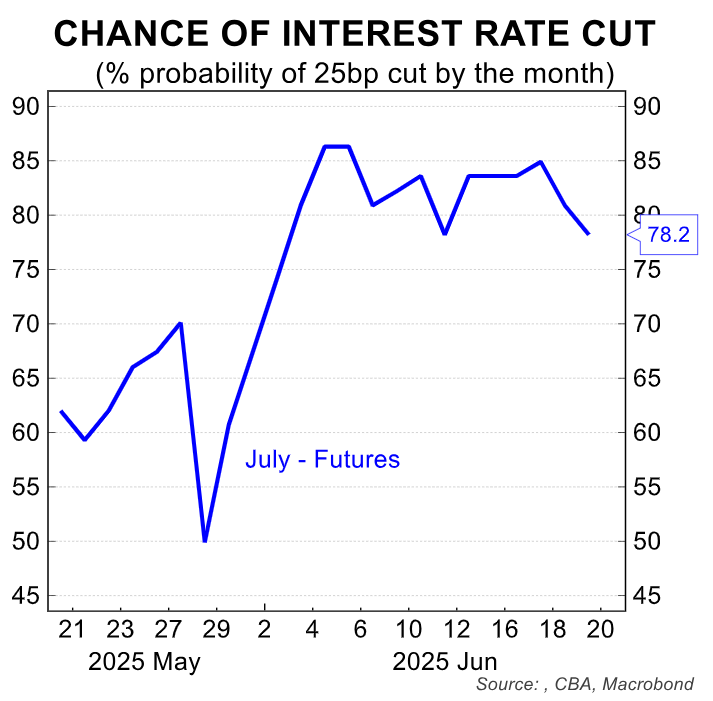

Closer to home, the Australian May labour force survey was the focus. With the July RBA meeting coming into view, the dataflow is key to assessing the likelihood of an interest rate cut next month. Money markets are currently ~80% priced.

Despite a drop in employment, the most policy relevant metric, the unemployment rate was steady at 4.1% for the fifth month in a row. The consistency of the unemployment rate means the labour force report does not shift the dial either way for the RBA.

The final piece of the data puzzle is due next week with the May monthly CPI indicator released.

Aside from geopolitics, offshore economic news was centred on three central bank decisions. The US FOMC, Bank of England and Bank of Japan all left policy on hold as widely expected.

The FOMC is firmly in wait and see mode as it relates to US tariff impact on economic activity and inflation. Fed Chair Powell said he expects the US consumer to bear some of the cost of the tariffs (i.e. higher inflation) but they could afford to wait and see how large the impacts will be.

The Bank of England kept rates on hold as expected as they continue to reduce rates once per quarter. There were divergent views with three members voting to reduce the Bank rate.

The Bank of Japan also kept rates steady as progress on the US-Japan trade agreement remains slow going. We expect the BoJ to wait until December 2025 to next increase the policy rate.

Next week, local analysts will be focused on the May monthly CPI indicator. This is the final piece of key data that will form the basis for the RBA’s July decision. We expect annual headline inflation to ease to 2.3%/yr and for the annual trimmed mean measure to fall to 2.5%/yr.

If the data prints as we expect though, there are some details under the hood that suggest that there are upside risks to both our and the RBA’s Q2 25 CPI forecasts. If these risks crystalise and given the potential impact on energy costs stemming from a further escalation in the Middle East –discussions about inflation may be a little more cautious around the RBA Board table in July.

We also get data on job vacancies and the preliminary June S&P Global PMIs. On job vacancies, the level remains elevated across a wide variety of industries. This signals significant demand remains for labour in the Australian economy, but this demand has been cooling. We expect a broadly flat outcome in the three months to May 2025.

The PMI’s will be closely watched given the subdued signals coming from the business sector recently (NAB Business Survey is a case in point).

Offshore, focus will remain on geopolitics and news on US trade policy. The May PCE deflator in the US will garner most attention in terms of the dataflow. We expect a benign outcome in May but anticipate the inflationary impact of the tariffs is certainly coming.